Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

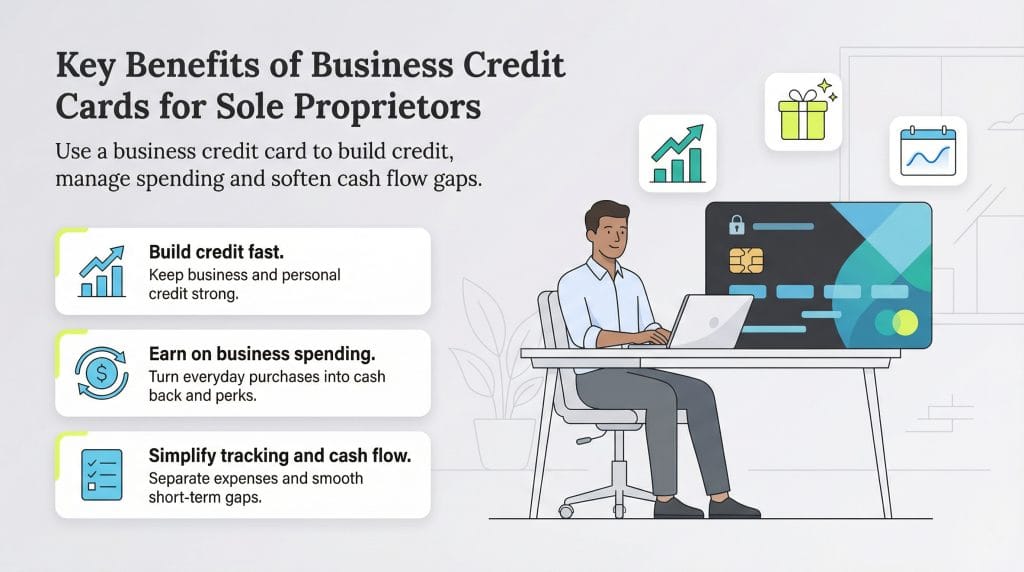

Build business credit while simplifying your accounting processes and earning rewards.

At some point after starting your business, you’ll likely apply for a business credit card. A business credit card simplifies your accounting process while helping you build business credit to obtain business loans and secure better interest rates.

However, you may hesitate to apply for a business credit card if you’re a sole proprietor. What are the benefits and will you even get approved? We’ll explain more about business credit cards for sole proprietors and share five tips to improve your chances.

If you have a sole proprietorship, your chances of being approved for a business credit card (and the interest rates you’ll pay if you carry a balance) are tied directly to your personal credit history. Your personal credit will affect the credit card’s initial limit and interest rate. Different credit card companies will have varying eligibility requirements, so while your sole proprietorship may not qualify for one card, you may be eligible for another.

After being approved for a business credit card, sole proprietors must be vigilant about using the card responsibly. If not carefully managed, a credit card can lead to financial hardship and cash flow problems for a business.

Notably, according to the Small Business Administration, there is no separation between you and the sole proprietorship you own and operate from a legal standpoint. In other words, you are responsible for the debts your business incurs.

“A credit card is a tool that can be used correctly or incorrectly,” said LJ Suzuki, founder of CFOshare. “Yes, you should get a business credit card because it is a good tool to have in your toolbox. But it is up to you to use that tool wisely.”

Suzuki noted that many rules governing personal credit card approval apply to getting a business credit card. “Generally speaking, it is still one of the easiest forms of credit to get — you can apply online for any variety of cards with different perks,” Suzuki explained. “But don’t be surprised if they ask for your Social Security number and run a credit check on you personally.”

Consider the following steps and best practices that will improve your chances of being approved for a business credit card as a sole proprietor.

Before applying for a business credit card, ensure your business finances are organized clearly and separate from your personal accounts. In particular, establishing a dedicated business checking account to manage your income and expenses is crucial. Mixing funds can complicate tax filing and hinder accurate financial recordkeeping. A separate business account also shows credit card issuers that your business is legitimate and professionally managed.

Jim Pendergast, general manager at altLINE, emphasized that showcasing your sole proprietorship’s clear financial structure is essential when applying for a business credit card. “A huge part of this process is opening a business bank account that is separate from their personal finances,” Pendergast stressed. “This shows credit card issuers that they are serious about running their businesses professionally and have accurate financial records, such as cash flow documentation.”

Countless business credit card providers exist. When assessing the best option for your sole proprietorship, consider that these cards are backed by financial institutions, banks and credit unions — and these entities are more inclined to approve businesses with which they already have a relationship.

To get started, check with the banks where you already have personal and business accounts and ask if they issue business credit cards. You can also turn to a bank where you were approved for a small business loan. These financial institutions are more likely to approve you because they already know your creditworthiness.

Additionally, consider the perks and rewards a business credit card offers. For example, a cash-back card may make sense or you may prefer a travel rewards card.

As a sole proprietor, your personal financial situation matters more than it would for business owners in other business structures, such as a limited liability company or S corporation. Card issuers will scrutinize your personal credit score.

Before applying for a business credit card, check your personal credit score. According to Experian, a good credit score is in the 700s. However, there is some flexibility here. For example, FICO considers scores between 670 and 739 good while VantageScore considers scores between 661 and 780 good.

However, there is some flexibility here.

Ryan Duitch, CEO and founder of Arro Finance, said sole proprietors should focus on improving their credit score before applying for a business credit card. “Sole proprietors should treat applying for a business card just like a personal one,” Duitch explained. “Be sure to have strong credit by keeping your utilization low and show a clear business purpose for the card by submitting activities and revenue.”

When applying for a business credit card as a sole proprietor, you’ll be asked to provide your Social Security number, recent financials to show monthly revenue and expenditures and potentially your company’s tax identification number (TIN).

While most other small businesses will be required to provide an employer identification number (EIN) as their TIN to apply for a business credit card, your status as a sole proprietor means you’ll generally use your Social Security number instead. If you hire employees, you’ll be required to have an EIN assigned to your business by the IRS. However, even as a sole proprietor without employees, obtaining an EIN can be beneficial as some financial institutions may prefer it for business credit card applications.

The card issuer will also want to know how long you’ve been in business. Banks and other financial institutions want to minimize their risk. Card issuers are more willing to work with a more established sole proprietorship than a new one.

Since credit card issuers want to manage their risk with the borrowers they take on, sole proprietorships that offer a personal guarantee have a better chance of being approved. A personal guarantee means you agree to use your personal assets to repay the debt if your business cannot.

If your credit history is limited, consider applying for a secured business credit card, which may require a cash deposit as collateral. While business credit cards typically do not require specific physical collateral like company equipment or real estate, offering a secured option can help establish your creditworthiness.

Using a business credit card responsibly can improve your credit score and offer additional perks. “Credit cards are an excellent form of debt to float temporary cash shortfalls or finance large online purchases such as furniture or software,” Suzuki explained. “[But] credit cards are a terrible form of long-term financing. You would be better to get a working capital line of credit or term loan if you need debt for more than a few months.”

The following are some of the benefits a business credit card can offer your sole proprietorship:

While it’s impossible to list every potential credit card available to sole proprietors, the following are well-regarded options. Benefits vary by the card issuer, so consider rewards, interest rates and fees:

Jennifer Dublino contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.