Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

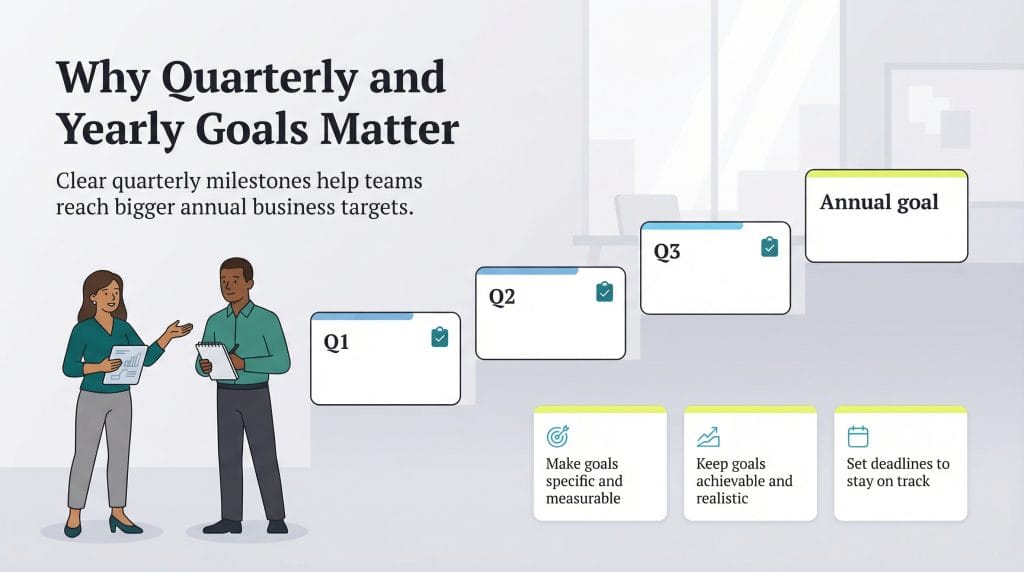

All businesses need to set goals and evaluate them throughout the year, but the first quarter has a significant impact on your company's success.

April marks the beginning of the second quarter of the year and the conclusion of tax season. Once your business’s accountant has finalized your tax returns, it’s a great opportunity to analyze how the year is going for your company, including the progress you’ve made on your goals for the first quarter. Below, discover how you can effectively analyze your Q1 performance to set your organization up for success in Q2 and beyond. Plus, find out how the first quarter can affect your whole year and why goal setting is the backbone of business growth.

When Jan. 1 hits, businesses typically resolve to reach ambitious goals, some of which may be quarterly objectives or yearlong initiatives. Even though it may feel like there is so much time ahead of you, the first three months of the year go by quickly. Reflecting on what your company did and didn’t accomplish during this time is crucial for moving forward.

“Evaluating business performance after the first quarter can help companies maintain discipline and focus on where they want to go in the coming fiscal year,” said Swapnil Shinde, CEO of the bookkeeping software company Zeni. “It’s important to use first-quarter data to help identify what is successful and what is failing, something you’ll want to make sure you’re doing before making any major investment.”

Here are four ways to take stock of how your business fared during Q1 so you can continue working toward your company’s goals in Q2.

Set aside time in April to review the company goals you set in January. Looking at the right key performance indicators (KPIs) can give you valuable insight into whether these goals were met. Although the exact KPIs to focus on will vary depending on your business model, some critical metrics you should keep an eye on are sales revenue, gross and profit margins, overhead costs, and monthly profits or losses.

“Revenue growth and profit margins help determine if sales are trending in the right direction and whether pricing strategies need adjustment,” said Amy Friedrich, president of benefits and protection for Principal Financial Group.

Friedrich also recommended incorporating broader economic trends and customer sentiment into your analysis to give you a better understanding of the macroeconomic environment and its financial impact on your business.

In addition to financial goals, you may have set objectives related to consumers’ experiences with your company and their perception of your brand. For example, you may have aimed to improve your company’s reputation or boost customer retention. You also may have established goals centered around your team, like implementing a successful hiring process, increasing productivity or building internal leadership.

For every goal you set, you should have a metric that tells you whether you and your staff are making progress toward that objective. However, when you’re choosing which KPIs to assess, remember that more isn’t always better.

“There is such a thing as overanalyzing, and this can be counterproductive if there isn’t a clear focus on the ultimate business objectives,” said Joseph Gonzalez, founder and CEO of Level Up Insurance and host of The BluePrint Podcast. “The key is knowing what drives success and not getting lost in data for data’s sake.”

Once you’ve identified your KPIs, evaluate the goals you set and determine which ones have been reached in Q1. Commend your team members for their excellent work on meeting these goals. It may be time to grow any goals that were met too easily.

Most small businesses start the year excited and determined to kick off new projects and embark on challenging goals, but it’s perfectly normal to fall short of the high expectations presented in the first quarter. Just don’t let that discourage you or keep you from taking a realistic look at where business is now and how it needs to improve.

Based on your KPIs, identify the Q1 goals that were not reached. Then, determine why your company didn’t meet them.

“[You] must decide if the problems stem from execution flaws or faulty strategies while considering external influences,” Gonzalez told us.

For example, maybe the goals were unrealistically high, the implementation plans weren’t communicated clearly, or an unexpected incident caused a loss of business. Whatever the reason for not reaching the goals, it’s essential to make corrections and move forward.

If your business results from Q1 don’t align with your projections, consider taking a different approach to achieve better results in Q2. You might have to get a little uncomfortable by trying new technology, new approaches or new ideas to get on the right course.

According to John Little, founder and CEO of The Winner’s Edge Coaching, taking stock of Q1 requires more than an understanding of financial data and marketing campaign results. It also requires a careful eye to identify trends within your team and organization. These can signal what is and what is not going well from a people standpoint, which can directly affect your bottom line.

“Smart leaders recognize that Q1 isn’t just about results; it’s about patterns,” Little explained. “Q1 can be extremely informative when we take time to observe and reflect to understand where to lean in and double down, or where to pause and recalibrate.”

To do this, Little suggested asking yourself the following questions:

“When companies fail to assess their Q1 performance holistically, they risk making tactical adjustments while ignoring the systemic leadership gaps that drive long-term success,” he said.

Part of reflecting on Q1 means looking forward to Q2. Beyond uncovering areas for improvement and course correction, your Q1 assessment should highlight what went well and where to invest your time and energy in Q2.

“Identifying areas of strong performance provides an opportunity to concentrate available resources on these successful initiatives to enhance overall growth rates,” Gonzalez said. “It’s important to avoid simply reacting to circumstances because the real objective involves establishing strategic foundations to support the remaining year’s success.”

These strategic foundations include establishing positive, proactive habits, like dedicating regular time to monitoring your cash flow.

“This way, you can plan for shortages, understand when surpluses might occur, and protect both customer and vendor relationships,” said Mark Valentino, president of business banking at Citizens. “Setting aside regular time to review your financial reports can provide the opportunity to study and understand these documents thoroughly.”

Another element of this strategic foundation is protecting your organization and its people, regardless of changes to your business’s performance or the broader economic environment.

“Business owners should use this time to revisit their long-term plans to make sure they have strategies in place to protect themselves, their employees and the value of their business,” Friedrich said. “For example, talent remains a core tenant of any business’s success, and investing in employees through benefits that protect their health and financial well-being drives greater retention.”

>> Related: How Employees Make or Break Business Success

For the areas where the company fell short, your Q1 analysis should lead to the development of specific tactics that can get the business back on track in Q2. Once you identify those strategies, get all of the company’s stakeholders to commit to adhering to the updated plans. These leaders should then communicate the plans to the rest of the staff.

Set deadlines for the new and continuing objectives, and plan to meet weekly with the key players to update everyone on progress and notify them about any potential issues. Discuss how new developments will be implemented, and emphasize the importance of committing to your company’s revised goals.

It’s essential for all team members to be aware of the Q1 assessment and the company’s updated goals so they know where marks were missed and they’re motivated to do better. It’s especially important to loop in employees whose performance may have contributed to missed targets. Management and staffers should be encouraged to offer suggestions for improvement and new methods for reaching individual and team goals. Including the whole staff in the journey to make Q2 better can benefit employee engagement.

The first quarter of the year can either be the driving force behind your business’s success or lead to a slow downfall over the rest of the year. It’s vital to assess progress in Q1 to see how your company can improve weak spots and continue successful tactics in the next quarter.

Here are two big reasons Q1 affects your whole year:

As the saying goes, “Fail to plan, plan to fail.” Businesses that don’t set goals in the first quarter of the year aren’t setting themselves up for success. It’s much harder to embark on and accomplish time-sensitive initiatives when you’ve already wasted the first three months of the year. But if you set quarterly and annual goals for your company, it’s just as important to evaluate them over time to ensure you’re on the path to success.

Keep in mind, however, that your Q1 performance isn’t the be-all and end-all for the year, and it’s never too late to adjust.

“A strong Q1 doesn’t guarantee a strong year, just as a weak Q1 doesn’t mean failure,” Little said. “What matters is how leaders evaluate, interpret, strategize and communicate.”

Setting goals for each quarter and the year is a crucial part of building and maintaining a successful business. When you set business goals, you and your team have clear targets to work toward. Goals keep everyone on the same page and can boost morale.

You may wonder which types of goals you should set for maximum success. One accessible goal-setting framework is the SMART method. This means that, regardless of the team or department, a goal should be:

The more specific your goals are, the easier it is for you and your team to strategize how to accomplish them. Organize quarterly goals so they build upon each other and can lead you to accomplish larger annual goals. Then, take stock of the first quarter and each one thereafter.

Sean Peek and Adam Toren contributed to this article.