Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is a Certified Financial Statement? (And How to Get One)

Understand the requirements, process and costs of obtaining audited financial statements for your business.

Written by: Skye Schooley, Senior Lead AnalystUpdated Jan 27, 2026

Editor Verified:

Editor Verified

A business.com editor verified this analysis to ensure it meets our standards for accuracy, expertise and integrity.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

When your business reaches certain milestones (e.g., securing significant funding, pursuing government contracts, preparing for acquisition), you’ll likely encounter a request for certified financial statements. This requirement often catches business owners off guard, especially when they discover it’s more involved than simply having their bookkeeper sign off on the numbers.

We’ll walk you through exactly what certified financial statements are, when you need them and the step-by-step process to obtain them. Whether you’re preparing for a major loan application or responding to investor requirements, understanding this process can save you time, money and unnecessary stress.

Certified financial statement — the short definition

A certified financial statement is a set of audited financial reports that an independent certified public accountant (CPA) has examined and signed, providing reasonable assurance that the numbers are free from material misstatement.

The package typically includes four core statements:

Statement of cash flows (operating, investing and financing activities)

Statement of equity (changes in ownership accounts).

Together, these documents give a complete snapshot of your company’s financial position and performance. Primary users include commercial lenders (who need assurance before extending credit), equity investors and private equity firms (during due diligence), government agencies (for regulatory filings or grant compliance) and partners or buyers in merger and acquisition transactions.

Tip

If someone requests "certified" financials, always confirm whether they mean a full audit or will accept a review. The difference in cost and timeline is substantial.

Certified vs. reviewed vs. compiled (what you actually need)

Not every financial statement engagement carries the same weight. The table below breaks down the three common levels of assurance you’ll encounter when working with a CPA.

Category

Audit

Review

Compilation

“Certified”?

Yes, typically what “certified” refers to

No

No

Assurance level

High / reasonable assurance

Limited assurance (analytics and inquiries)

None (no assurance)

Who performs

Independent CPA (external)

Independent CPA (SSARS review)

CPA (SSARS compilation)

Typical procedures

Tests of details & controls, confirmations, inventory observation, analytics, inquiries

Analytics, develop expectations, investigate variances; no substantive testing

Assemble financials from management data; no testing

Deliverable & common uses

Auditor’s report plus audited (“certified”) financials; often required by lenders and regulators

Review report; sometimes accepted when a full audit isn’t mandated

Compilation report; usually insufficient where assurance is required

When choosing between these options, consider your specific requirements. If your bank loan covenant explicitly requires “audited” or “certified” statements, a review won’t suffice. However, if you’re seeking preliminary investor interest or applying for smaller credit facilities, a review engagement might meet your needs at roughly half the cost of a full audit. Always confirm the required level of assurance with the requesting party before engaging a CPA firm.

Bottom Line

An audit gives reasonable assurance, a review offers limited assurance and a compilation provides no assurance at all. Match the engagement type to your stakeholder's actual requirement before signing an engagement letter.

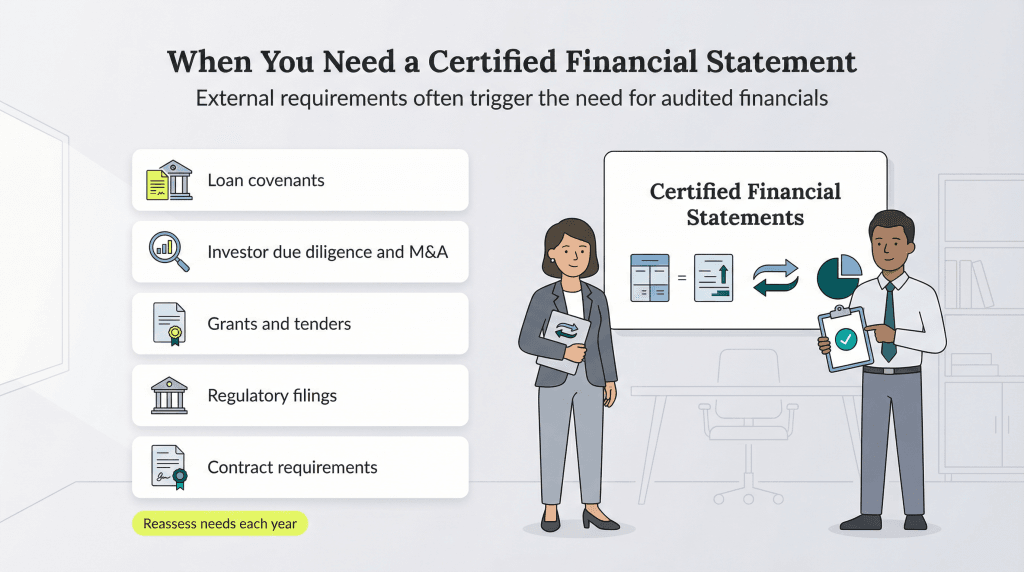

When you need a certified financial statement

Most small businesses operate for years without an audit. Certified statements become necessary only when an external party demands independent verification of your numbers. Here are the most common triggers:

Loan covenants: Many commercial credit agreements require annual audited financials to monitor debt-to-equity ratios, working capital floors or other financial covenants.

Investor due diligence and M&A: Private equity firms, venture capital funds and strategic buyers almost always request audited statements before closing. Quality of earnings reports often build on audited figures.

Grants and tenders: Government contracts and grant programs frequently mandate audited financials to ensure compliance with spending restrictions and reporting rules.

Regulatory filings: Certain industries (e.g., insurance, finance, healthcare) face statutory audit requirements from state or federal regulators.

Contract requirements: Franchise agreements, partnership buyout clauses or supplier contracts may specify annual audits as a condition of doing business.

If none of these apply to you today, revisit the question annually. Growth, new credit facilities and ownership changes all create audit triggers that catch business owners by surprise.

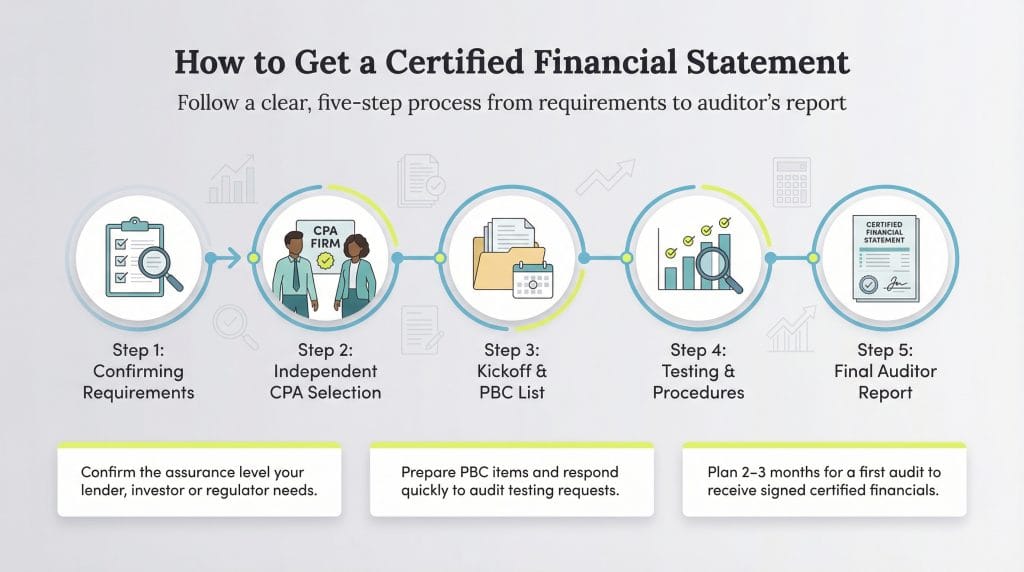

How to get a certified financial statement (step-by-step)

Obtaining audited financials isn’t as simple as handing your books to an accountant. The process is methodical, collaborative and heavily documented. Here’s how it unfolds:

Step 1: Confirm the required assurance level with the counterparty.

Before you engage an auditor, ask your lender, investor or regulator whether they will accept a review or truly require a full audit. Request any specific scope items in writing, such as single-audit compliance for federal grants or agreed-upon procedures for certain loan covenants. This saves you from paying for more assurance than necessary or discovering mid-engagement that your CPA’s standard scope won’t satisfy the requirement.

Step 2: Select an independent CPA or audit firm.

Independence matters. The CPA firm cannot have bookkeeping, payroll or controller-level responsibilities for your company during the audit period. Look for firms with experience in your industry; a CPA who audits manufacturing companies will move faster and catch risks a generalist might miss. Check that the firm undergoes peer review every three years, a quality-control requirement for all audit practices.

Step 3: Complete the kickoff meeting and PBC list.

Once you sign the engagement letter, the audit team will send a provided-by-client (PBC) list – a detailed request for documents, schedules and supporting evidence. We’ve included a comprehensive checklist later in this guide. Schedule fieldwork windows around your calendar; auditors often need two to four weeks of access to records, systems and key personnel. Blocking those dates early prevents delays.

Step 4: Navigate the audit procedures.

The auditors will test account balances, send confirmations to banks and customers, observe inventory counts (if applicable) and review contracts, board minutes and legal correspondence. They’ll document control weaknesses, propose adjusting entries for errors and request management explanations for unusual transactions. Your job is to respond promptly and provide clear support. The faster you close open items, the faster the audit wraps.

Step 5: Receive the auditor’s report.

At the conclusion, the CPA issues an opinion letter – typically “unqualified” (clean), “qualified” (clean except for specific issues), “adverse” (material misstatements) or a “disclaimer” (insufficient evidence). An unqualified opinion is what lenders and investors expect. The final package includes the signed opinion, footnoted financial statements and any required supplemental schedules.

Tip

Budget two to three months from kickoff to final report for a first-time audit. Subsequent years often run faster because systems, controls and documentation improve.

Cost and timeline — what drives both

Audit fees vary widely, and firms rarely publish rate cards. A microbusiness with clean books might pay $8,000 to $15,000 for a straightforward audit, while a $20 million revenue company with multiple entities, significant inventory and complex revenue recognition can easily spend $40,000 to $100,000 or more.

Several factors push costs up or down:

Size and complexity: More revenue, more locations and more product lines mean more testing and more hours.

Industry risk: Construction, healthcare and financial services face tighter scrutiny (and higher fees) than service-based businesses with simple revenue models.

Data quality and ERP maturity: Companies running on spreadsheets or patched-together software take longer to audit than those on integrated accounting platforms like NetSuite or QuickBooks Online.

Number of entities: Consolidated groups require intercompany elimination schedules and separate legal-entity work.

Prior audit history: First-year audits cost more because the team must understand your systems from scratch and often restate opening balances.

The timeline depends on responsiveness. If you deliver a complete PBC package at kickoff and answer follow-up questions within 48 hours, fieldwork can wrap in two to three weeks. Delays in providing bank statements, contracts or reconciliations stretch the calendar and often trigger hourly overruns.

Bottom Line

Expect to invest both cash and management time. The true cost of an audit includes your controller's hours pulling reports, your operations team facilitating inventory counts and your legal counsel drafting representation letters.

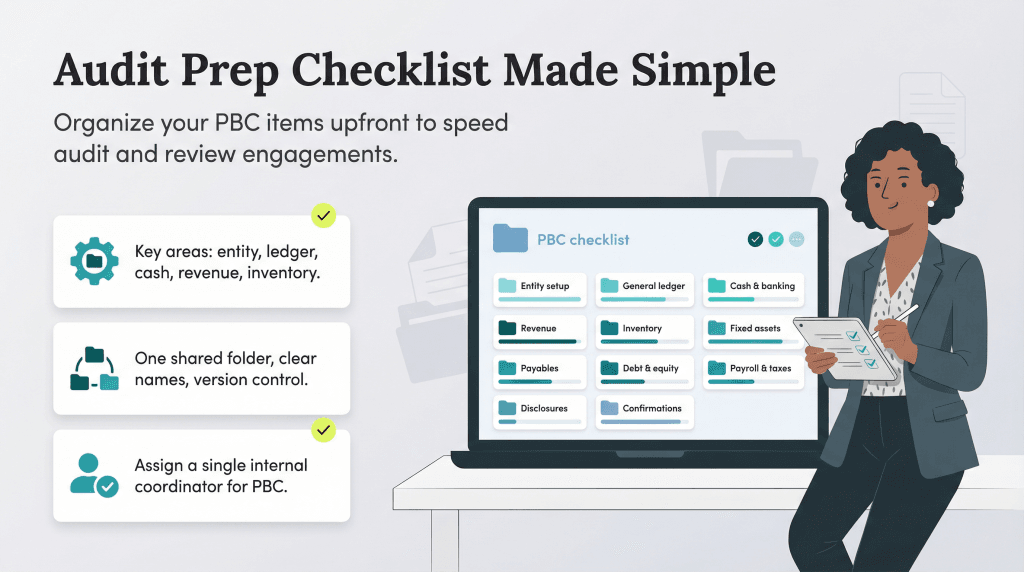

Document and prep checklist

Auditors will send their own PBC request, but assembling these items in advance demonstrates readiness and accelerates the engagement. Actual requests vary by engagement type (audit versus review), entity structure and industry.

Entity and engagement setup

Legal name(s), employer identification number (EIN), addresses, ownership structure and capitalization table

Organizational documents (articles of incorporation, bylaws, operating agreement)

Board or management meeting minutes and resolutions

Prior year financial statements and auditor or reviewer reports

Trial balance (current year) and prior-year comparative trial balance

Draft management representation letter (to be finalized at conclusion)

Organize these items in a shared folder (e.g., Google Drive, Dropbox, SharePoint) with logical subfolders. Label files clearly and version-control anything updated during fieldwork. This structure not only speeds the current audit but also builds a reusable framework for future years.

Tip

Assign a single internal point person, such as your controller or CFO, to coordinate PBC requests. Auditors appreciate one email thread and one contact instead of chasing multiple departments.

Who can certify your statements?

Only an independent CPA licensed to practice in your state can issue an audit opinion and certify your financial statements. Independence is non-negotiable: the firm cannot perform bookkeeping, prepare your tax returns or hold any financial interest in your company during the audit period.

When selecting an auditor, prioritize these criteria:

Industry experience: A CPA who has audited dozens of software-as-a-service (SaaS) companies will navigate ASC 606 revenue recognition far faster than a generalist.

Peer review status: Every CPA firm that performs audits must undergo a peer review every three years. Ask to see the most recent report and confirm it was a pass with no deficiencies.

Client references: Request contact information for two or three audit clients in similar industries and revenue bands. Ask about responsiveness, value-added insights and billing transparency.

Technology compatibility: If your company uses specialized ERP or data analytics platforms, confirm the auditor has experience extracting and testing data from those systems.

We recommend interviewing at least two firms before signing an engagement letter. Compare scope, fee structures (fixed versus hourly) and cultural fit. The right auditor becomes a long-term advisor, not just a once-a-year compliance vendor.

Did You Know?

The Public Company Accounting Oversight Board oversees auditors of public companies, but private-company audits fall under state boards of accountancy and professional standards set by the American Institute of CPAs.

Frequently asked questions

Yes, in most business contexts. When someone requests certified financial statements, they typically mean audited statements accompanied by an independent CPA's opinion letter. The term "certified" is informal shorthand for the assurance an audit provides.

Not automatically. Most small businesses operate successfully with compiled or reviewed statements (or no third-party assurance at all). You need an audit only when a lender, investor, regulator or contract specifically requires one. If you're self-funded and not seeking outside capital, an audit is optional.

Sometimes. Community banks and credit unions often accept reviewed statements for loans under $1 million or when the borrower has strong collateral and a solid credit history. Larger institutions and syndicated loan groups almost always require audits. Always confirm the requirement in writing before scheduling an engagement.

Plan for eight to twelve weeks from engagement kickoff to final report for a first-time audit. Subsequent years compress to six to eight weeks as your team becomes familiar with the process and documentation improves. Delays in providing requested documents extend the timeline.

A complete set includes the balance sheet, income statement (or statement of operations), statement of cash flows and statement of equity (or statement of changes in stockholders' equity). Footnotes accompany each statement, disclosing accounting policies, significant estimates and other required information.

Skye Schooley is a dedicated business professional who is especially passionate about human resources and digital marketing. For more than a decade, she has helped clients navigate the employee recruitment and customer acquisition processes, ensuring small business owners have the knowledge they need to succeed and grow their companies.

At business.com, Schooley covers the ins and outs of hiring and onboarding, employee monitoring, PEOs and HROs, employee benefits and more.

In recent years, Schooley has enjoyed evaluating and comparing HR software and other human resources solutions to help businesses find the tools and services that best suit their needs. With a degree in business communications, she excels at simplifying complicated subjects and interviewing business vendors and entrepreneurs to gain new insights. Her guidance spans various formats, including newsletters, long-form videos and YouTube Shorts, reflecting her commitment to providing valuable expertise in accessible ways.