Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Security incidents are costly and can damage your reputation.

When a small business accepts credit card payments and other digital payment forms online, cybersecurity is of the utmost importance. Seemingly innocuous actions, like clicking a link in an email, can expose your customers’ personal information to hackers and leave your company vulnerable to legal action, lost business and brand distrust.

Securing your online payment process is crucial for your business’s survival. We’ll share 11 online payment security tips to protect your business and customers.

Searching for a credit card processor and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Consider the following online payment security best practices to protect your customers and business.

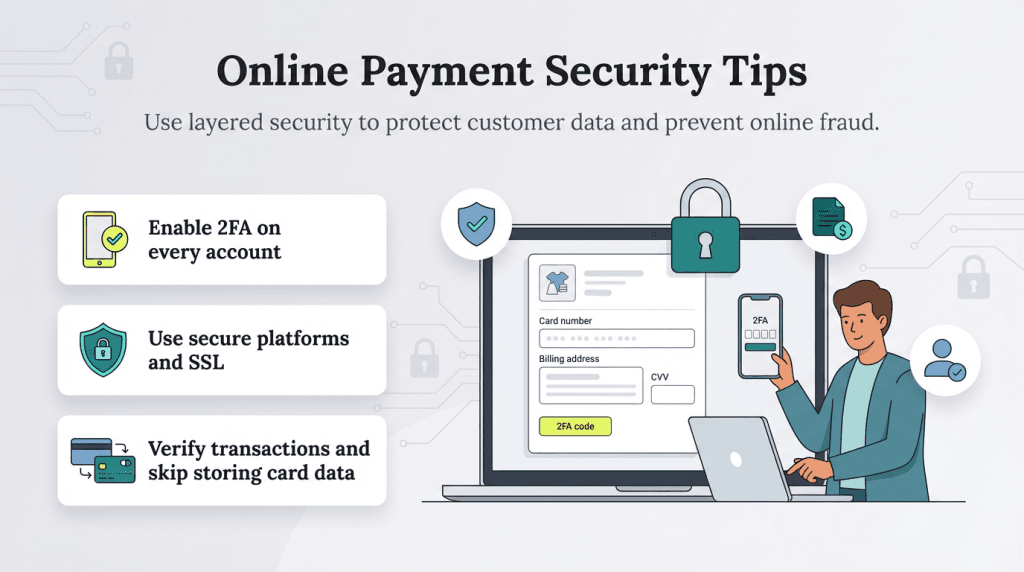

Two-factor authentication (2FA) is an essential element of any company’s cybersecurity plan. 2FA, also called multifactor authentication (MFA), is essential when you deal with vendors, social media, financial institutions or any platform where your business has an account. If a cybercriminal can access your accounts, your customers’ sensitive information and your company’s private data are at stake. If you deal with a vendor that doesn’t offer 2FA or MFA, request it or find a more secure vendor.

With 2FA, you know immediately if someone is trying to access your account and can take steps to secure it by changing the password. According to John Price, a cybersecurity expert and CEO of SubRosa, MFA is also crucial for securing your business’s internal information.

“Businesses should consider using [MFA] for any internal access to payment systems, ensuring only authorized personnel can handle sensitive transactions,” Price advised. “Implementing strong access controls and limiting data retention can also go a long way in reducing vulnerabilities.”

Online businesses can improve security by verifying transactions, which are less secure because they are of the card-not-present variety, in the following ways:

One of the best ways to protect your online store is to base it on a secure e-commerce platform. The best e-commerce platforms — such as BigCommerce, Adobe Commerce, Shopify and WooCommerce — are established companies that have excellent reputations and implement innovative security measures, such as:

Platforms with strong security are rarely the cheapest, but this cost is a crucial part of your cybersecurity budget. Secure e-commerce platforms can ultimately save you money by protecting your reputation and your customers.

You may still be vulnerable to savvy hackers or dishonest employees even when you do your best to secure your operations. Cyber insurance will help cover your bases. Cyber liability insurance typically covers the costs associated with a data breach, such as those for:

Requiring customers to set up an account before they make a purchase lets you verify them with login credentials. Alternatively, you can ask customers to confirm their identity by providing a photo of their driver’s license or other government-issued identification for big-ticket items.

It’s best not to store any customer payment data, which could otherwise become a target for cybercriminals. Don’t store electronic data or paper files, such as when you take credit card payments over the phone. However, if you must store payment data to enable easy repeat purchases, work with a third-party company that uses encryption to protect the data.

Brent Johnson, chief information security officer at Bluefin, recommended using tokenization services to secure customer payment data.

“Merchants can choose to take advantage of tokenization services to remove cardholder data from their environment, rendering stored sensitive data useless to hackers in the event of a breach,” Johnson said. “Tokenization also fosters consumer confidence by keeping their payment and personal data secure while using that data to create a more personalized online shopping experience.”

A Secure Sockets Layer (SSL) certificate provides security by encrypting communication between the customer and your business. SSL certificates give customers added confidence about doing business with you because they see the certificate displayed in the browser.

For extra security, install a firewall and implement an intrusion detection and prevention system.

Any business that accepts credit cards is required to comply with the Payment Card Industry Data Security Standard (PCI DSS). This set of standards covers proactive steps that businesses must take to:

In addition to credit cards, which you can verify with additional information, consider accepting payment forms with built-in security. These include electronic checks verified through the Automated Clearing House (ACH) network and digital wallets such as Apple Pay, Google Pay and Samsung Pay, which are secured through blockchain technology.

Human error leads to many data breaches, so it’s vital to invest in employee training. Train team members to identify and properly handle suspicious emails or calls that might be phishing attempts to gain login credentials.

Warn them against clicking unexpected email attachments that might contain malware or sharing sensitive information with unauthorized people. Ensure they log out of their workstation when leaving their desks and never leave work-related USB drives or devices unattended.

When you see something out of the ordinary, like an unusually large order from an existing customer, call them to verify its legitimacy.

Protect your customers and business by accepting secure forms of payment. These are some of the most secure payment methods: