Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Boost customer satisfaction with another convenient payment option.

Since many businesses, from restaurants to retailers, take orders over the phone, you need to be able to accept credit card payments over the phone, in addition to in person via a credit card reader or point of sale (POS) system. Fortunately, many of the best credit card processors support this option, allowing merchants to offer an added service that boosts customer satisfaction in an increasingly card-centric society.

We’ll explain methods for collecting credit card payments over the phone and share information to help you get started.

Searching for a credit card processor and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

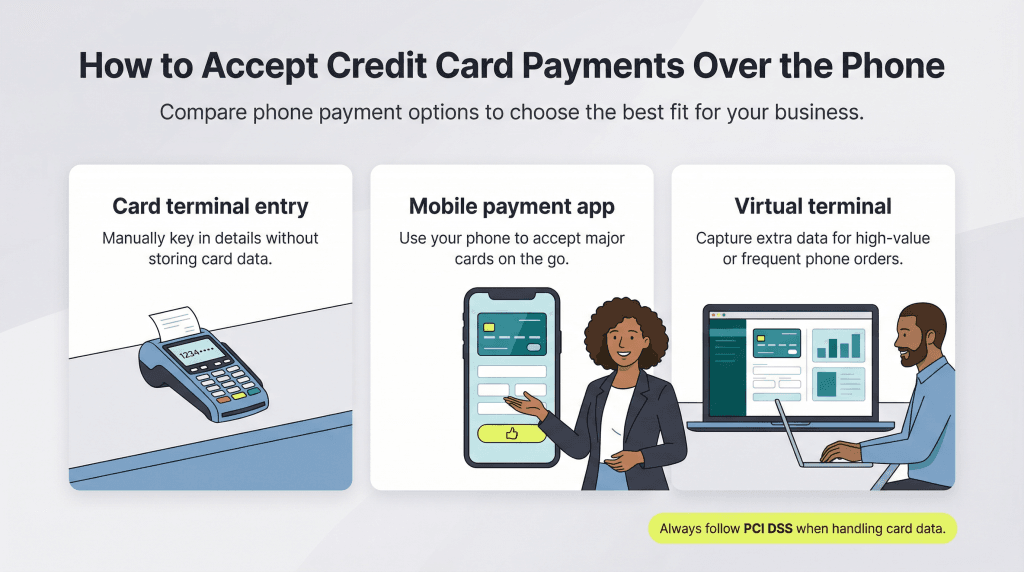

You can accept card payments over the phone in several ways:

Ask your customer to read off the card number, expiration date and card verification value (CVV) code while you type the information into your POS system’s credit card terminal.

Importantly, instruct employees never to write down cardholder information ― a practice that can put your business at risk of violating credit card processing rules and laws, including Payment Card Industry Data Security Standards (PCI DSS).

To accept credit card payments with your mobile phone, enter your customer’s credit card information into the mobile app your credit card processor provides.

The best mobile credit card processors allow you to accept all major credit cards, provide free payment apps, sell reasonably priced EMV card readers and provide generous customer support.

Virtual terminals are web-based credit card processing applications. They sometimes offer Level 2 or Level 3 processing ― methods that capture additional data to verify a transaction’s authenticity. This functionality typically incurs an additional monthly charge, making it a better fit for businesses that accept high-dollar transactions or experience a high volume of phone transactions.

Here are several business types that frequently accept credit card payments over the phone:

Restaurants that accept phone orders need a robust phone system to accommodate high call volumes. Check out our reviews of the best business phone systems for restaurants to get started.

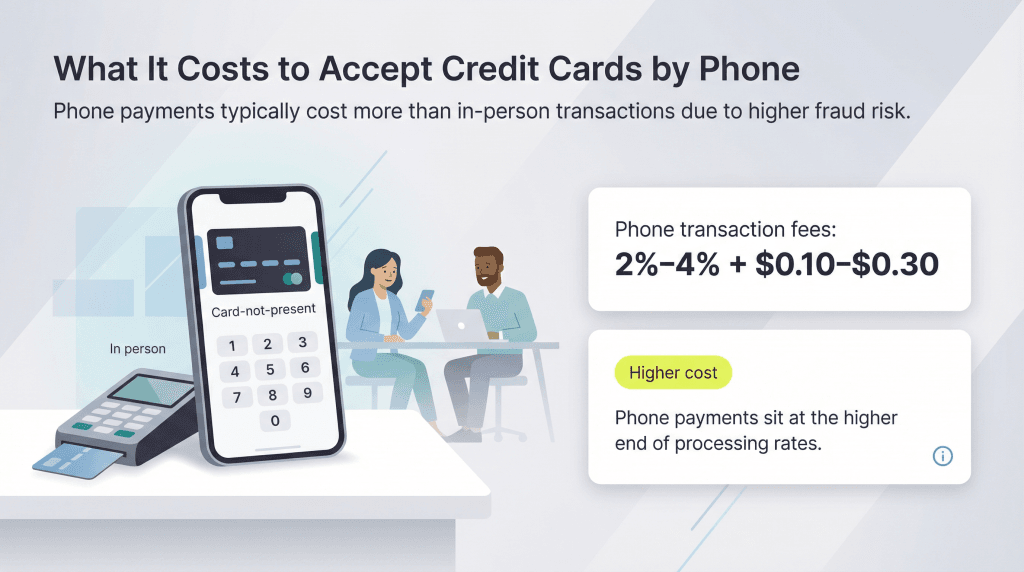

When a customer pays with a credit or debit card over the phone, there’s always a risk that the customer isn’t the authorized cardholder. In addition to incurring higher processing rates, these transactions leave merchants vulnerable to fraudulent charges.

Scott Waters, senior vice president of business development at Merchly, emphasized that PCI compliance is the top security concern when accepting credit card payments over the phone.

“It is always recommended to use a third-party interactive voice response or payment system that will accept payments through touch-tone keypad to ensure compliance with PCI standards,” Waters advised.

Waters also noted that employee dishonesty is a considerable risk.

“It’s always recommended if employees are able to take payments over the phone to restrict their access to phones, notes and other methods of storing customer personal information,” Waters cautioned.

To avoid fraudulent charges, merchants should take the following security measures:

Accepting credit cards over the phone can bring many benefits to your business, including:

“Another pro of using a processor with a direct bank relationship is an underwritten merchant account,” Waters added. “These accounts have been looked at by a representative at the processor and bank and generally come with higher daily and monthly limits as well as lower processing fees.”

The primary drawbacks of accepting credit cards over the phone are security risks, employee fraud and higher payment processing fees.

Frank Pagano, managing partner of VizyPay, noted that fraud and security issues are the biggest risks associated with accepting credit cards by phone.

“Without the right encryption (or lack thereof), card information can be compromised by interception or through simple human error by manually inputting the information,” Pagnano cautioned.

Additionally, phone transactions are especially vulnerable to fraud.

“This also opens the door for card-not-present fraud, where criminals can use compromised credit card information for unauthorized purchases over the phone,” Pagnano explained.

Additionally, a customer may be defrauded while thinking they’re processing a transaction with a legitimate business.

Merchants mitigate these risks by implementing robust security practices when taking phone payments:

Employee fraud is another risk merchants must consider. An untrustworthy employee might misuse or sell the credit card information they collect. To maintain PCI compliance and reduce this risk, ensure there’s no written record of customer card data. Instead, associates should enter the information directly into the POS system, where it’s encrypted and secured.

When a card isn’t physically swiped, dipped or tapped, there’s a greater chance the transaction is unauthorized, so processors offset that risk with higher processing fees.

Credit card processing costs vary depending on the service provider and pricing model. However, you’ll likely pay more to accept credit cards over the phone than for in-person, card-present transactions.

Most credit card processors charge merchants between 2 percent and 4 percent of each transaction. Card-not-present transactions — including phone orders — typically fall on the higher end of that range due to the greater risk of fraud and chargebacks. In addition to the percentage fee, most processors also charge a fixed per-transaction fee (often around 10 to 30 cents) for card-not-present payments.

Danielle Bauter contributed to this article.