Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

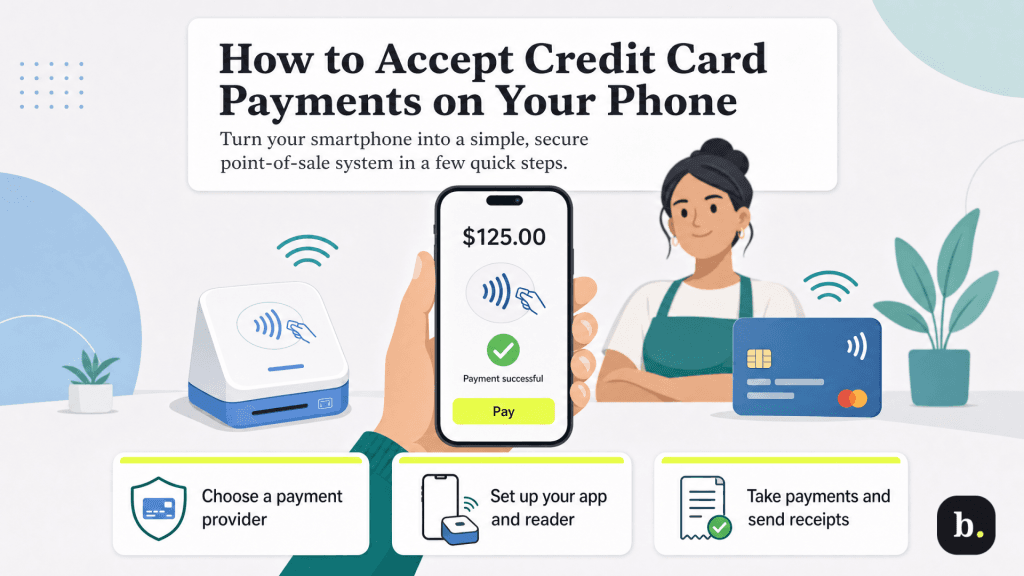

Accepting credit card payments has never been easier for small businesses. Here's how to take payments with your phone, along with the tools, costs and setup tips to keep in mind.

Many businesses need to take payments while they’re on the go, whether they’re working trade shows, making deliveries or meeting customers in the field. That makes accepting credit cards with your phone an appealing option. In this guide, we’ll walk through how mobile payment processing works, what it costs and what to look for before you get started.

Yes. With the right payment processor, your phone can double as a mobile checkout tool, letting you accept credit cards, digital wallets and other contactless payments wherever you do business. Providers like Square and PayPal offer mobile apps, card readers and flexible pay-as-you-go pricing that make it easy to get started.

“Mobile card processing is especially valuable for small and medium-sized businesses that provide services on-site, such as home repair, personal training or delivery services,” said Bob Legters, chief product officer at Paysafe. “It allows businesses to go cashless, enabling customers’ payment choice and allowing businesses to collect payments in real time.”

Getting started is usually faster than many business owners expect, especially if you’re already accepting credit cards online or in person. While the exact setup process may vary by provider, the steps below will help you get your phone ready to accept payments in the field, at events or anywhere you do business.

Before you can start taking payments with your phone, you’ll need to open a merchant account with a credit card processor or set up an account with a payment facilitator, if you don’t already accept credit cards.

Most credit card processors and payment facilitators have their own mobile app, and this is where your setup really starts to come together. After downloading the app, you’ll typically enter some basic business details, link your bank account and finish activating your account.

Most apps work on both iPhone and Android devices and walk you through setup step by step, so you usually won’t need much technical experience to get started.

Along the way, you may also be able to set tax rates, build a simple inventory list, turn on tipping or customize digital receipts — features that can be especially helpful for retailers, contractors and other service-based businesses.

Many payment providers now support Tap to Pay, which lets you accept contactless payments directly on a compatible smartphone. Others offer mobile card readers — sometimes at no upfront cost for new merchants — that connect to your phone through Bluetooth or, in some cases, a physical dongle.

“Since [mobile credit card processors] utilize existing smartphones or tablets, they are cost-effective by reducing hardware expenses,” said Peter Galvin, chief marketing officer at payment solutions provider NMI. “Additionally, they are simple to set up, usually only requiring the download of an app, and features are easy to update through the app store.”

Not every customer will have a card ready to tap or insert. In those situations, a virtual terminal gives you another way to take payment by manually entering card details through a secure webpage or app provided by your payment processor.

To key in a payment, you’ll typically need:

Once your app, reader and account are fully set up, you’re ready to start taking payments. The process looks a little different depending on whether you’re using a mobile reader or keying in a transaction manually.

Once the payment goes through, provide the customer with a digital or printed receipt. Most payment apps and virtual terminals make it easy to email or text receipts directly from your phone.

If you’re regularly taking payments in person, a mobile receipt printer can add a more polished touch, especially for businesses that work events, pop-ups or on-site service calls.

After the transaction settles, your payment processor will deposit the funds into your bank account, minus any applicable processing fees.

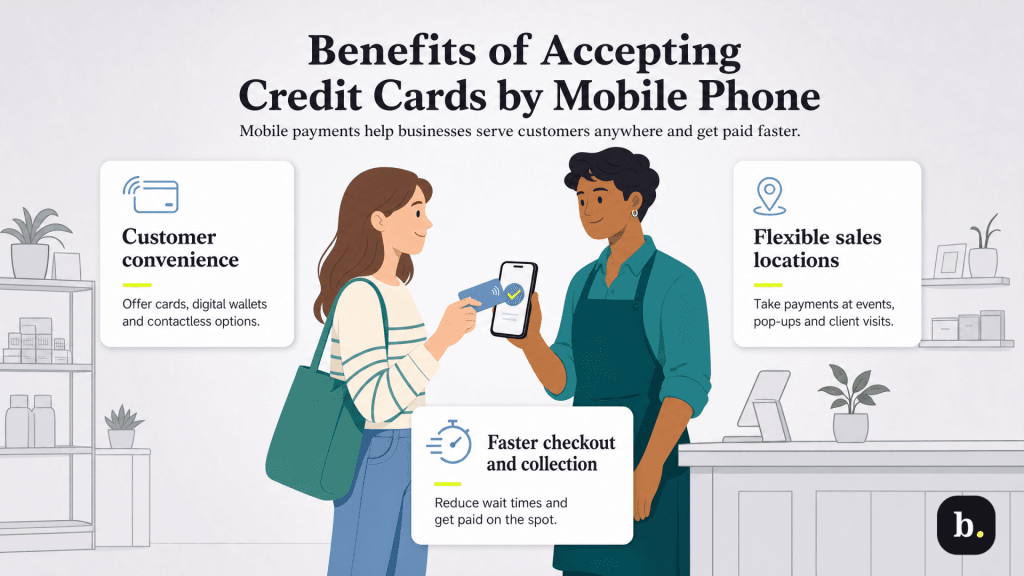

Accepting credit card payments with your phone can do more than help you make sales on the go. For many businesses, mobile payment processing makes it easier to meet customers where they are, work more flexibly, speed up checkout and collect payments faster.

Here’s a look at the benefits of accepting payments via your phone.

Cash is becoming less common in everyday transactions, so accepting cards, digital wallets and other contactless payments gives customers more ways to pay and helps create a great customer experience.

“[Mobile phone payments] don’t just provide the best customer experience — they [help businesses] build stronger, lasting relationships with their clientele, improving their operational model and creating flexibility in how they do business,” said Matt Downs, president of Integrated & Platforms at Global Payments.

One of the biggest advantages of mobile payment processing is how easily it lets you take your business beyond your usual setup. Even if you normally work from a storefront, office or restaurant, accepting payments on your phone can open the door to new sales channels, events and off-site opportunities.

A restaurant owner might use an iPhone to take payments or an Android payment app to process sales at food festivals, catering events or community pop-ups. Retailers selling clothing, jewelry or handmade goods can test new markets through trunk shows and temporary shops. Independent sales consultants can collect payment on-site during client visits — no countertop hardware or fixed checkout station required.

Mobile payment devices aren’t just useful for businesses on the move. Stores, restaurants and other brick-and-mortar businesses can also use them to speed up checkout lines, especially during busy seasons, product launches or major promotions.

Long lines can test a customer’s patience, and in some cases, cost you the sale altogether. Giving employees mobile payment devices lets them check out customers wherever they are in line, helping transactions move faster when traffic picks up.

Getting paid on the spot can solve one of the biggest headaches for service-based businesses. Instead of tracking down overdue invoices, waiting for a check to arrive in the mail or dealing with the debt collection process, you can collect payment as soon as the job is done.

That means less time spent following up on unpaid balances and fewer write-offs tied to late or missed payments.

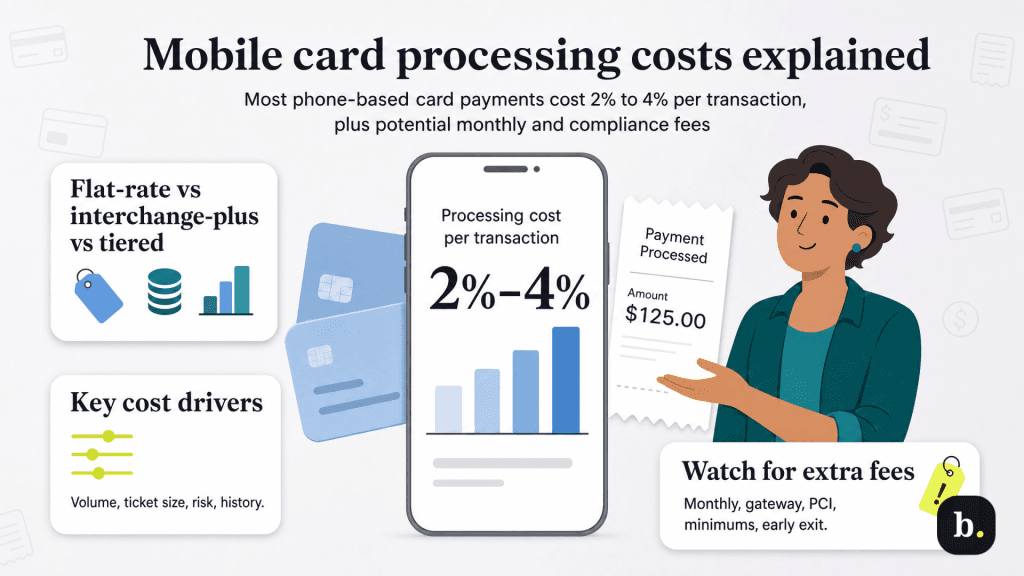

For most businesses, mobile payment processing costs fall somewhere between 2 percent and 4 percent per transaction, though your actual rates can vary quite a bit depending on your provider, pricing model and how your business processes payments.

The numbers your business sees on paper may depend on things like:

Not every provider prices mobile payment processing the same way. Payment facilitators often keep things simple with flat-rate pricing, while traditional credit card processors may use interchange-plus or tiered pricing instead.

Here’s what those pricing models typically look like:

Transaction rates are only part of the picture. Depending on your provider, especially if you work with a full-service payment processor, you may run into additional fees like these:

“Beyond the basic pricing models, businesses should evaluate processors based on their transparency, contract flexibility and ability to scale with business growth,” Downs explained. “Payment processors that offer customized fee structures or volume-based discounts can provide significant savings as your business expands.”

Mark Fairlie contributed to this article. Source interviews were conducted for a previous version of this article.