Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Mobile businesses can save time and money by accepting payments with their iPhones.

Entrepreneurs with mobile businesses like pop-up shops, home service companies or food trucks must be able to accept payment on the go. Rather than using a wired credit card reader that needs to be plugged in, you can use your iPhone.

Searching for a credit card processor and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Many credit card processing companies allow you to accept credit card payments with your iPhone. We’ll explain everything you need to know about accepting payments via iPhone.

An iPhone can help mobile business owners access a powerful and versatile payment terminal that can save customers time and reduce hassles.

Follow these steps to accept payment with an iPhone:

“Using an iPhone to accept credit card and mobile wallet payments has never been easier,” noted Lou Alfieri, merchant services consultant at Shift4. “Doing so enhances mobility, allowing merchants to accept payments anywhere, whether at a counter, tableside or offsite.”

There are many options when mobile credit card processors that allow you accept payments with an iPhone. When searching for the best option, evaluate their card reader pricing, processing costs and card reader features.

Here are a few of the best mobile credit card processing solutions to consider:

Processor | iPhone card reader | Features | Reader cost | Processing cost |

|---|---|---|---|---|

Clover | Clover Go | Swipe, tap, chip and contactless payments | $199 | $0-$14.95 monthly fee; 2.6% plus 10 cents transaction fee |

Square | Square Reader (for contactless and chip) | Chip, tap and contactless payments | Free for new merchants, otherwise $59 | No monthly fee: 2.6% plus 10 cents transaction fee |

PayPal | PayPal Zettle | Swipe, chip, tap, contactless payments and PIN pad | First one $29, then $79 | No monthly fee; 2.29% plus 9 cents transaction fee |

Helcim | Helcim card reader | Swipe, tap, chip, contactless payments and PIN pad | $99 | No monthly fee; Interchange plus pricing averaging 1.83% plus 8 cents |

Payanywhere | Payanywhere 3-in-1 | Swipe, tap, chip and contactless payments | $59.95 | No monthly fee; 2.69% transaction fee |

SumUp | SumUp Plus card reader | Swipe, tap chip, contactless payments and PIN pad | $54 | No monthly fee; 2.6% plus 10 cents transaction fee |

Here is some additional information on each option.

The Clover Go mobile credit card reader can accept magnetic stripe (swiped), chip (inserted) and near-field communication (NFC or tapped) cards. It also supports mobile wallets like Apple Pay, Google Pay and Samsung Pay. This compact $199 device connects to your iPhone via Bluetooth and interfaces with the Clover Go mobile payment app.

Clover offers various pricing plans tailored to industry and business needs, so monthly payments vary. For example, under the Home Services category’s Standard plan, you’ll pay $199 plus $14.95 monthly for the Clover Go device and a software plan that allows you to accept payments and manage your business. You’ll also pay 2.6 percent plus 10 cents per transaction for card-present transactions via the reader.

Our complete review of Clover credit card processing explains more about Clover’s pricing plans and options.

Square is a credit card facilitator that offers the Square Reader for contactless and chip payments. This compact reader utilizes Bluetooth and supports NFC mobile payments like Apple Pay and Google Pay. However, it doesn’t support cards with magnetic stripes or chipless cards.

The Square Reader costs $59 and interfaces with Square’s POS software, allowing you to view sales transactions, manage inventory, issue digital receipts and manage your customers. There are no monthly fees. You’ll pay 2.6 percent plus 10 cents per transaction for card-present transactions via the reader.

Our in-depth review of Square explains how the vendor’s robust free service plan provides businesses with everything they need to accept various payments.

Like Square, PayPal is a credit card facilitator. With these platforms, you don’t have your own merchant account. When you accept card payments with PayPal, you’re a submerchant under PayPal’s umbrella merchant account.

Unlike the Clover Go and Square Reader, the PayPal Zettle iPhone credit card reader has a numeric pad where customers can enter their debit PIN. It accepts chip, tap and swipe transactions; customers can also pay via PayPal, Venmo, Apple Pay, Samsung Pay and Google Pay. PayPal Zettle is one of the only credit card processors that supports Venmo for business.

The Zettle reader utilizes Bluetooth and works with PayPal’s Zettle app, which integrates with PayPal’s free Zettle POS software. This combination creates an efficient solution for businesses with e-commerce and brick-and-mortar stores.

Your first PayPal Zettle mobile card reader for iPhone costs $29; additional units cost $79. There are no monthly fees; you’ll pay 2.29 percent plus 9 cents per transaction for card-present transactions via the reader.

Helcim’s iPhone card reader allows you to accept swiped, chip and NFC card transactions and mobile wallets. It also features a numeric pad for PIN input. The reader connects via Bluetooth and can interface with Helcim’s POS software on iPhones, iPads and laptop computers.

Helcim POS software also includes automatic tax calculations, inventory management and customer data. Helcim card readers cost $99 each. There are no monthly fees; on average, you’ll pay 1.83 percent plus 8 cents via the reader.

Our review of Helcim credit card processing explains more about this all-in-one platform that provides merchants with essential tools beyond credit card processing.

The Payanywhere 3-in-1 reader doesn’t have a numeric pad and looks similar to the Clover Go and Square readers. It accepts magnetic stripe, EMV and chip cards and mobile wallets.

This $59.95 device connects to your iPhone, tablet or laptop via Bluetooth. The Payanywhere app supports adding tips or percentages and accepts signatures for additional security. It can also send digital receipts or kitchen tickets for food service businesses.

There are no monthly fees; you’ll pay 2.69 percent per transaction for card-present transactions via the reader.

The SumUp Plus reader accepts swipe, tap, chip, Apple Pay and Google Pay. It features a debit card PIN pad on the back. The reader connects via Bluetooth, boasts excellent battery life (up to 500 transactions per charge) and is affordable at only $54.

The accompanying app allows you to manage products in your catalog, assign tax rates and send digital receipts. If you have multiple employees, you can see everyone’s sales.

There are no monthly fees; you’ll pay 2.6 percent plus 10 cents per transaction for card-present transactions via the reader.

If your business is inherently mobile, you must accept payments on the go. And since most people don’t carry checks or much cash, accepting credit cards and digital payment methods is essential.

Additional benefits of accepting mobile payments via your iPhone include the following:

“The number one benefit to being able to accept payments from your phone is being able to get paid anywhere,” said Branden Korf, marketing associate at EBizCharge. “You can collect payments from your farmers market booth, from your food truck or after completing a job fixing a sink as a plumber. There are so many scenarios where collecting payments from your phone is a huge help for daily business operations.”

Alfieri emphasized that accepting payments with iPhones is a win-win for businesses and customers.

“[iPhone payment processing] improves the customer experience with quick, secure and convenient payment options and is a professional, modern checkout process that supports growing payment trends,” Alfieri said.

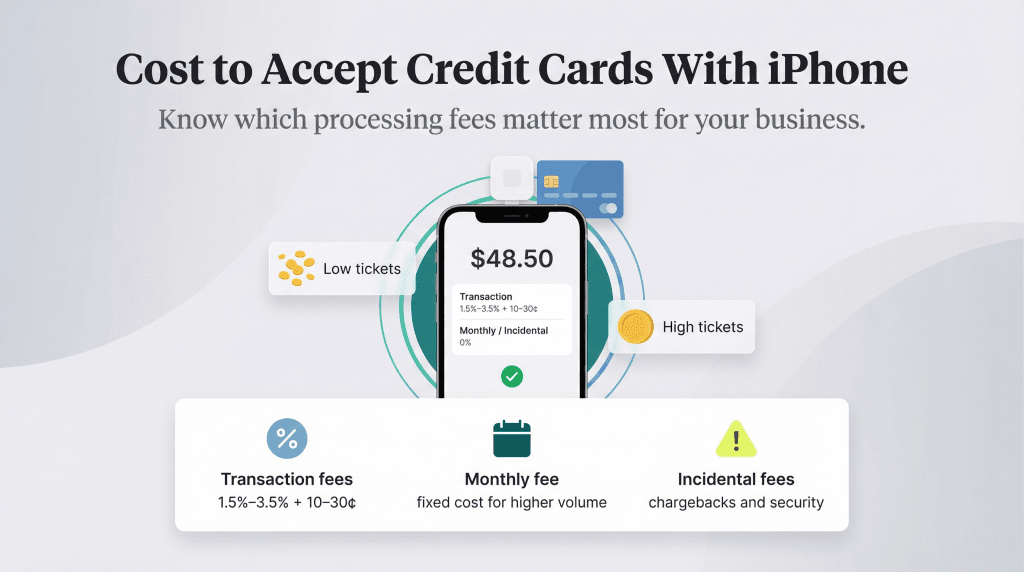

Here’s a quick primer to help you understand your costs.

All payment processors charge a transaction fee ― a percentage of the total purchase amount. Some processors also charge a flat amount per transaction. Transaction rates range between 1.5 percent and 3.5 percent plus 10 to 30 cents per transaction. Here’s what you should know:

Some credit card processors charge a monthly fee that covers, at a minimum, customer service and monthly statements. This fee may include other services, including PCI security compliance and payment gateway charges. Processors that charge monthly fees usually have lower transaction rates and may be a good choice for businesses with higher sales volumes.

Most payment processors charge incidental fees when specified events (outlined in the contract) occur. For example, you’ll typically be assessed a chargeback fee if a customer disputes a transaction and you may be charged if you don’t meet security requirements.

“The financial barrier to entry for mobile payments is remarkably low,” Kyle Hall, CEO of PayKings, explained. “Most providers offer free basic equipment and charge only per-transaction fees, making it accessible for even the smallest merchants.”