Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

If you manufacture, sell or distribute products, your insurance policy portfolio should include product liability insurance.

Your business is responsible for the products you make, sell or distribute, as well as the completed services you provide. You can be held liable and accountable for any losses or damage if one of your products is faulty and injures or kills a third party or leads to property damage. To provide some financial protection in these circumstances, product liability insurance can help cover the legal costs of any claims filed against your business.

Current industry data shows that defective product incidents account for more than 40 percent of the value of all liability claims, making product liability insurance a critical protection for businesses of all sizes. Allianz Commercial analysis reveals this trend has persisted over the past five years, highlighting the ongoing financial risks businesses face.

This comprehensive guide will help you understand everything you need to know about product liability insurance, including who needs coverage, what it protects against, how much it costs and how to choose the right policy for your business.

>> Read Next: The Insurance Claims Process and How to File

Product liability insurance provides your business with coverage against expenses that arise when a person claims a product your business sold, made or distributed caused bodily injury, unlawful death or property damage.

This type of insurance policy can provide financial assistance to cover legal fees, judgments against you, settlements, compensatory damages, punitive damages and economic or business damages that result from a lawsuit. It will also cover the injured party’s medical costs that arose from the use of your product. [For a full list of the different types of business insurance you might need, check out our Business Insurance Guide.]

Product liability insurance and general liability insurance are typically purchased together, but these policies are not the same. Product liability insurance provides coverage against damages related to the products you make, distribute or sell, as well as completed services.

General liability insurance, in contrast, provides coverage against a wide range of claims that arise when a third party is injured or property is accidentally damaged on your premises, such as a customer trips on the carpet in your store and drops their smartphone or breaks their ankle. Additionally, such policies cover damages an employee causes on third-party premises. General liability insurance also provides coverage against lawsuits over claims you copied a competitor’s logo or damaged their reputation.

Businesses that make, sell or distribute products need product liability insurance. Companies and individuals involved in construction also require product liability insurance.

Here’s a closer look at some of the businesses and business professionals who should have product liability insurance.

Product liability insurance protects manufacturers against claims that one or more of their products caused property damage or personal injury. The insurance provides coverage against lawsuits resulting from design defects, manufacturing defects and related issues.

Product liability insurance protects retailers, suppliers, distributors and other members of the distribution chain against lawsuits over damages caused by the products they sell. Retailers can be sued even if they’re not responsible for the products’ defects or issues related to their use. This kind of insurance can also provide coverage for lawsuits related to marketing defects, such as a lack of warnings about product use or misuse and improperly applied labels.

It’s important to note that retailers can be held liable even if they weren’t aware they sold a defective product. A person who is injured by a defective product or incurs financial losses due to the product’s use or misuse can sue anyone involved in the product’s supply chain. The injured person can also sue a retailer that didn’t provide sufficient warning or accurate instructions for using the product.

Construction professionals, general contractors and installers require product liability insurance to protect them against lawsuits over personal injury or property damage that occurred after they completed their work. For example, a homeowner could sue a heating, ventilation and air conditioning professional who installed a furnace that later malfunctioned and led to a natural gas leak that injured or killed someone. In this case, the installer’s product liability insurance policy could cover their legal costs.

Product liability insurance provides coverage if your product or completed service does one or more of the following:

Product liability insurance doesn’t cover services but does cover the results of services provided — for example, damages that resulted from a contractor’s work on a claimant’s property.

Below, learn more about what product liability insurance covers and what is excluded.

Product liability insurance can provide coverage against lawsuits over damages caused by defective products. A defective product refers to an item not fit for its intended purpose. A defect may also make the product unsafe for use.

There are different types of defects:

In a lawsuit over a wrongful death, a claimant could sue for three types of damage:

A product liability insurance policy typically includes reasons why the insurance provider may deny your claim, not provide coverage or choose not to renew your policy. These are known as exclusions.

Product liability insurance might include these common types of exclusions.

Product liability insurance is typically part of your general liability insurance premiums, so the cost will often be included in that amount. The price of the insurance depends on factors related to the risks associated with your profession and your policy limits. Manufacturers typically pay higher rates for product liability insurance because there are higher risks involved in their businesses.

Generally speaking, though, product liability insurance costs about 25 cents per $100 in sales revenue. For example, if your business sells $5 million worth of goods per year, your product liability insurance costs would be calculated like this: 0.25 x $5 million ÷ $100 = $12,500. [Learn how to save money on business insurance.]

These additional factors may affect the cost of your product liability insurance:

Each industry carries its own level of risk, which affects how much product liability coverage is needed.

For manufacturers:

For retailers and distributors:

For small businesses and artisans:

When choosing insurance coverage, select the limits for property damage and bodily injury separately:

These high limits will increase your costs but offer your business more protection.

Additional factors you should consider when choosing a product liability insurance policy include the following:

Your premiums are typically determined by the types of products you manufacture or sell, your expected sales volume and the role of your business. It’s essential to accurately assess your products (as well as your total expected sales) to ensure you pay for and receive the correct level of insurance coverage. Always review any existing business insurance policies to avoid overlapping or unnecessary coverage.

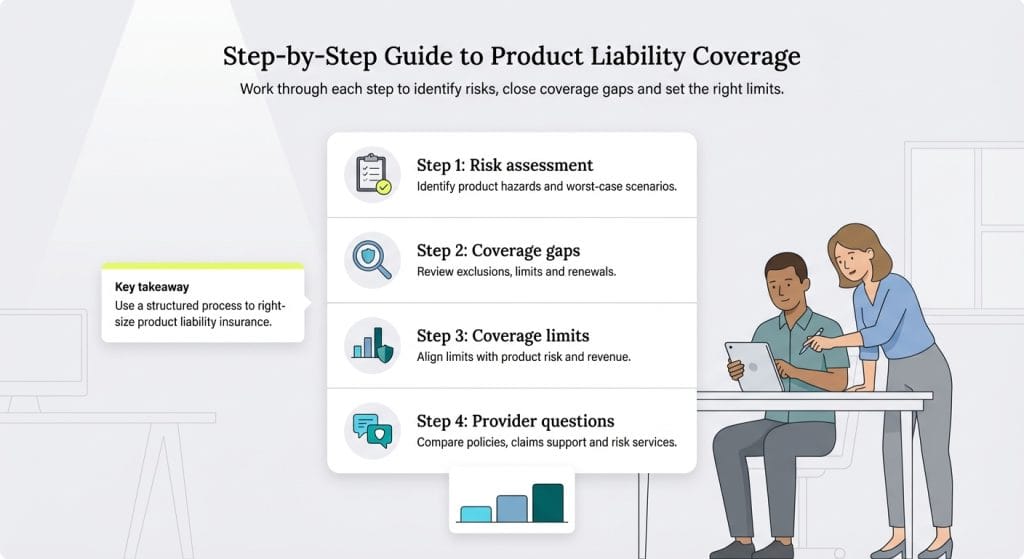

Choosing the right product liability insurance starts with understanding your specific risks and coverage gaps. Use this step-by-step framework to assess your needs, determine appropriate limits and make informed decisions when selecting a provider.

Evaluate your products systematically by listing everything you manufacture, sell or distribute. For each product category, identify potential hazards and assess the severity of possible injuries or damages. Don’t forget to factor in your role in the supply chain, as your liability can vary depending on whether you’re the manufacturer, distributor or retailer.

Key questions to ask:

Review your existing policies to ensure your coverage limits are adequate for potential claims. Check for exclusions that could leave you vulnerable, and consider any geographic limitations if you operate across state or national borders. It’s also important to take note of your policy’s renewal terms and the risk of non-renewal.

Use your product’s risk level and business model to guide how much liability coverage you need. The following benchmarks are widely used by insurers but should be tailored to your unique risk exposure and contractual obligations.

Your annual aggregate limit should typically be two to three times your per-occurrence limit to protect against multiple claims within the same policy year.

Coverage questions:

Claims handling questions:

Risk management questions:

By working through these steps, you’ll gain a clearer picture of your product liability exposure and how to protect your business. Taking a proactive, informed approach helps ensure adequate coverage, strengthen your risk management practices, build credibility with partners and reduce the long-term cost of claims.