Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

SBA Loan Forgiveness for PPP, EIDL and 7(a) Loans

What are the main features of PPP and EIDL loans and how does the forgiveness process vary for each type?

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

The United States Small Business Administration (SBA) offers several loan programs to support small businesses, including emergency relief loans and traditional financing options. If you’re looking for loan forgiveness, it’s essential to know which programs still offer it and which do not.

As of 2025, loan forgiveness is only available for the SBA’s Paycheck Protection Program (PPP) loans. Other SBA loans, including Economic Injury Disaster Loans (EIDL) and 7(a) loans, do not qualify for forgiveness. We’ll explain how PPP loan forgiveness works and outline options if you’re facing default on an SBA loan.

What is SBA loan forgiveness – and which loans qualify?

SBA loan forgiveness is the process by which the SBA cancels all or part of a borrower’s debt obligation under specific loan programs. Only certain SBA loan programs offer forgiveness options.

PPP loan eligibility

PPP loans are fully forgivable if businesses met employee retention requirements and used the funds for eligible expenses. Sally Graham, a former public affairs specialist with the SBA, confirmed that PPP loans are the only SBA loan eligible for forgiveness. “Current law only authorizes SBA to offer loan forgiveness on Paycheck Protection Program loans,” Graham explained. “COVID-19 EIDLs must be repaid.”

EIDL advance eligibility

Under the EIDL program, eligible businesses could receive up to $15,000 in funding from SBA that did not need to be repaid through three separate advance programs: the original EIDL Advance (up to $10,000), the Targeted EIDL Advance (up to $10,000) and the Supplemental Targeted Advance (up to $5,000).

Loans that do not qualify

Standard EIDL loans, 7(a) loans, Express loans and 504 loans do not qualify for forgiveness and must be repaid in full according to their terms. However, borrowers facing financial hardship may pursue alternative relief options such as hardship accommodation plans or Offers in Compromise (OIC).

Understanding PPP loan forgiveness

The PPP was an SBA loan program offered during the pandemic. PPP loans were disbursed through nearly 5,500 lenders across the country to help small businesses keep workers on their payroll and avoid layoffs. These loans were designed to be forgivable from the beginning, with specific requirements borrowers must meet to qualify for full forgiveness. However, this program ended on May 31, 2021.

Key forgiveness requirements

To qualify for PPP loan forgiveness, borrowers must meet several critical requirements:

Covered period compliance: The covered period was initially eight weeks but was later extended to 24 weeks, giving borrowers more flexibility in meeting forgiveness requirements.

60 percent payroll requirement: At least 60 percent of the forgiven loan amount must have been spent on payroll costs.

FTE employee retention: Borrowers must maintain their full-time equivalent (FTE) employee count during the covered period compared to pre-pandemic levels.

How PPP loans worked

PPP loans were available for up to $10 million, with eligibility based on total payroll liabilities, including wages, salaries and employee benefits. For instance, sole proprietors could receive 2.5 months’ worth of their net income, capped at an annualized $100,000 income limit. This meant that regardless of how much a business owner earned, PPP funds could only cover 2.5 months of income as if their annual salary were $100,000.

PPP loans had a low 1 percent fixed interest rate, making them effectively interest-free for many borrowers. Initially, these were two-year loans, but those approved after June 5, 2020, had a five-year repayment term.

How to apply: forms and deadlines

The SBA offers multiple application forms and methods for PPP loan forgiveness, with specific deadlines borrowers must meet.

Available application forms

Borrowers can use SBA Form 3508, 3508EZ or 3508S depending on their loan size and circumstances:

Form 3508: Standard application for all borrowers

Form 3508EZ: Simplified version for borrowers who maintained employee and compensation levels or had certain reductions in business operations

Form 3508S: Designed for loans of $50,000 or less with additional simplifications

SBA direct forgiveness portal

The SBA direct forgiveness portal is available for all borrowers regardless of loan size. Effective March 13, 2024, all borrowers can use SBA’s direct forgiveness portal, and applying through the portal can take as little as 15 minutes.

Critical deadlines

Understanding PPP forgiveness deadlines is essential for successful loan forgiveness:

Five-year application window: Borrowers have up to five years from the SBA loan number issuance date to apply for forgiveness.

10-month payment deferral: If borrowers don’t apply within 10 months after the covered period ends, they must begin making loan payments while awaiting forgiveness approval.

Tip

In addition to government-backed loans, business owners can pursue one of the best business loans or alternative lending options if they need financing help.

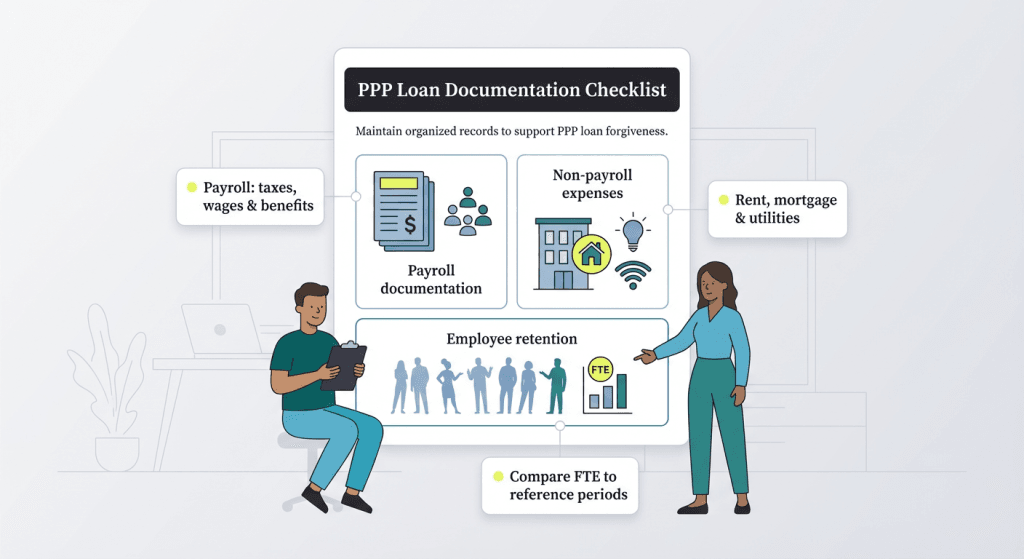

Documentation you’ll need

Proper documentation is essential for PPP loan forgiveness approval, and borrowers should maintain detailed records of how loan funds were used.

Payroll documentation

Payroll records are the most critical documentation for forgiveness. Required documents include:

Payroll tax filings

State quarterly wage reports

Payroll processor records

Evidence of payments for employee health insurance, retirement and state/local taxes

Non-payroll expense documentation

For rent and mortgage payments:

Lease agreements and receipts or canceled checks for rent payments

Lender amortization schedules and payment receipts for mortgage interest

For utility expenses:

Utility bills and receipts

Canceled checks or bank statements showing payments for electricity, gas, water, transportation, telephone or internet services

Employee retention records

FTE employee records help verify compliance with employee retention requirements. Borrowers should maintain documentation showing average FTE employees during the covered period compared to the reference periods:

February 15, 2019 to June 30, 2019

January 1, 2020 to February 29, 2020

For seasonal employers: March 1, 2019 to June 30, 2019

EIDL forgiveness: what’s eligible?

EIDL forgiveness is limited to the advance portion of the program, while the actual loans must be repaid.

EIDLs help small businesses affected by a disaster cover overhead costs and operating expenses. The SBA created two types of EIDL programs: COVID-19 EIDLs to help businesses survive pandemic-related financial hardships, and traditional EIDLs to assist businesses recovering from natural disasters like hurricanes, wildfires or floods.

EIDL advance programs

EIDL advances were forgivable grants available through three separate programs with a combined maximum of $15,000. The SBA provided up to $15,000 in funding that did not need to be repaid through three different advance programs:

Original EIDL Advance: Up to $10,000 (calculated at $1,000 per employee up to 10 employees)

Targeted EIDL Advance: Up to $10,000 for businesses in low-income communities with more than 30 percent revenue reduction and 300 or fewer employees

Supplemental Targeted Advance: Up to $5,000 for businesses with 10 or fewer employees in low-income communities with more than 50 percent revenue reduction

The combined amount from all three advance programs could not exceed $15,000. For example, if a business received the full $10,000 original EIDL advance, they could still receive up to $5,000 from the Supplemental Targeted Advance if eligible.

EIDL loan repayment requirements

Whether COVID-related or traditional, EIDL loans are not forgivable. Borrowers must repay them over 30 years, but there are no prepayment penalties for paying them off early. Graham cautioned borrowers to beware of scams promising forgiveness for SBA EIDL loans.

“Borrowers should be cautious of scams and phishing attempts that request money for SBA’s free assistance or purport to offer forgiveness for other SBA products, grants or loans,” Graham warned.

Although EIDL loans cannot be forgiven, the SBA offers a hardship assistance option for borrowers struggling with repayment.

Hardship assistance options

The SBA offers hardship assistance options for EIDL borrowers struggling with repayment. The SBA’s Hardship Accommodation Plan (HAP) provides temporary relief for EIDL borrowers facing financial difficulties.

“[In February of 2024], the SBA expanded eligibility for the Hardship Accommodation Plan,” explained Mark Valentino, president of business banking at Citizens Bank. “This is one option for those with outstanding [EIDL] loans who are unable to meet their loan payments.”

HAP benefits include:

Payments reduced to 10 percent of the usual amount for six months

No requirement to catch up on missed payments first

Plan can be renewed once after expiration

Interest continues to accrue during the accommodation period

Valentino urges borrowers to proactively work with their lenders if they run into repayment challenges.

“Work with your lender before defaulting to avoid the seizure of assets and collateral,” Valentino advised. “Seek support from your financial advisor, banking institution, and/or a lawyer with experience in this space.”

Did You Know?

Declaring bankruptcy may discharge certain SBA business loans, but it depends on the type of loan, the type of bankruptcy filed and whether the borrower personally guaranteed the debt.

Forgiveness timelines & what happens if it’s denied

Understanding PPP forgiveness timelines and the appeals process is crucial for borrowers seeking loan forgiveness. As of 2025, borrowers still have time to apply for PPP forgiveness, with the majority of PPP loans already forgiven. Roughly 10.5 million PPP loans have been forgiven, demonstrating the program’s success in providing relief to small businesses during the pandemic.

Borrowers with loans above $150,000 remain subject to six years of review and audit post-forgiveness. The SBA has expanded its audit and compliance efforts in 2025, focusing on larger loans exceeding $2 million and businesses flagged for potential misuse of funds.

If forgiveness is denied, borrowers must begin repaying their PPP loans according to the original terms. Denied borrowers can appeal the decision through their lender or the SBA, depending on how the application was submitted. The appeals process requires additional documentation to support the borrower’s case for forgiveness.

SBA Offer in Compromise (OIC) basics

Other SBA loans, including 7(a), Express and 504 loans, do not offer forgiveness. However, if you’re facing financial hardship, you may be able to work out an OIC with the SBA.

Pursuing an OIC should be a last resort, as it has stringent requirements far more punitive than PPP forgiveness. To qualify, you must meet the following criteria:

Financial hardship: You must prove you cannot repay your loan fully and can only afford to pay a portion of the debt.

Collateral liquidation: You can only submit an OIC request after all collateral has been liquidated.

Closed business: Your business must have ceased operations — you can no longer accept clients or produce products. However, you may collect final receivables or complete outstanding projects before submitting an OIC request, as long as the business is not actively operating.

The OIC typically applies only to the guarantor (unless a separate offer is made for the business entity). If your OIC is accepted, the legal business entity remains liable for the debt, meaning the debt is not fully forgiven. Instead, the guarantor is released from liability in exchange for a lump-sum cash payment.

PPP forgiveness vs. an OIC

Obtaining an OIC for an SBA loan is very different from pursuing PPP loan forgiveness. Here’s how:

Extensive paperwork: Submitting an OIC requires significantly more documentation than applying for PPP loan forgiveness. You must provide a personal financial statement, tax returns, pay stubs and bank statements to prove you cannot afford to pay the debt in full.

Review process: Unlike PPP forgiveness, which only requires submitting a short application to the lender, an OIC must first be reviewed and recommended by the original lender before being sent to the SBA. If the lender does not agree to the borrower’s proposed terms, the OIC will not be forwarded to the SBA for approval.

Stringent criteria: Lenders treat PPP forgiveness and SBA OIC requests very differently. PPP loans are 100 percent reimbursed by the SBA, whereas SBA 7(a) loans are typically 75 percent reimbursed. This means the bank will take a 25 percent loss on any amount forgiven through the OIC program. As a result, the bank has a financial stake in making the decision and will evaluate the loan much more critically than the PPP loan.

Comparison table: SBA loan forgiveness at a glance

Varied by program (original, targeted, supplemental)

Already forgiven automatically

EIDL Loans

No

Must be repaid over 30 years

HAP available for hardship cases

7(a), Express, 504 Loans

No

Must be repaid per loan terms

OIC may be available in extreme hardship

FAQs: SBA loan forgiveness

Borrowers have up to five years from the date the SBA issued the loan number to apply for PPP forgiveness. However, if borrowers don't apply within 10 months after the covered period ends, they must begin making loan payments while awaiting forgiveness approval.

No, forgiven PPP loans are not considered taxable income. The loan forgiveness amount does not need to be reported as income on tax returns, and expenses paid with PPP funds remain deductible.

Reductions in FTE employee counts can reduce your forgiveness amount proportionally. However, safe harbors exist if you restore FTE levels by December 31, 2020, or if you can document that qualified employees were unavailable or that business operations declined due to COVID-19.

If denied, you must repay the loan according to the original terms with one percent interest over two or five years depending on when your loan was approved. You can appeal the decision through your lender or directly with the SBA, depending on where you submitted your application.

No, EIDL loans are not eligible for forgiveness and must be repaid over 30 years. Only EIDL advances (up to $15,000 combined from all three advance programs) were forgivable grants. However, the SBA offers hardship accommodation plans for borrowers experiencing financial difficulties.

Matt Sexton contributed to this article. Source interviews were conducted for a previous version.

Jamie Johnson has spent more than five years providing invaluable financial guidance to business owners, leading them through the financial intricacies of entrepreneurship. From offering investment lessons to recommending funding options, business loans and insurance, Johnson distills complex financial matters into easily understandable and actionable advice, empowering entrepreneurs to make informed decisions for their companies. As a business owner herself, she continually tests and refines her business strategies and services.

At business.com, Johnson covers accounting practices, budgeting, loan forgiveness and more.

Johnson's expertise is also evident in her contributions to various finance publications, including Rocket Mortgage, InvestorPlace, Insurify and Credit Karma. Moreover, she has showcased her command of other B2B topics, ranging from sales and payroll to marketing and social media, with insights featured in esteemed outlets such as the U.S. Chamber of Commerce, CNN, USA Today, U.S. News & World Report and Business Insider.