Forming an S corporation can help create a clearer separation between you and your business. An S corp isn’t a separate type of business entity but rather a tax election available to eligible LLCs and corporations. That distinction doesn’t just matter at tax time. It also affects how you handle everyday expenses, track spending and build your company’s financial profile. A business credit card can play an important role in maintaining that separation, but only if it’s used correctly.

This guide covers how card issuers evaluate S corporations, the benefits a dedicated business credit card can provide and what to consider when choosing and applying for one.

How do card issuers treat S corporations?

Many S corp owners assume their tax status will affect how they qualify for a business credit card. In reality, card issuers are usually more interested in the underlying business than the S corporation election itself.

When you apply for a business credit card, you’ll generally be treated like any other incorporated business. Issuers will look at the business’s revenue, business credit profile and financial history, along with the personal credit of any owner required to provide a guarantee. The S election itself doesn’t unlock special card terms or approval standards.

In practical terms, that means having your EIN, legal business name and basic business information ready before you apply. Some issuers may also ask for formation documents or financial information, especially if you’re seeking a higher credit limit.

S corp owners may be surprised if a card application asks for both an

EIN and an SSN. However, even with an established business, a personal guarantee often means the issuer wants information tied to both the company and the owner.

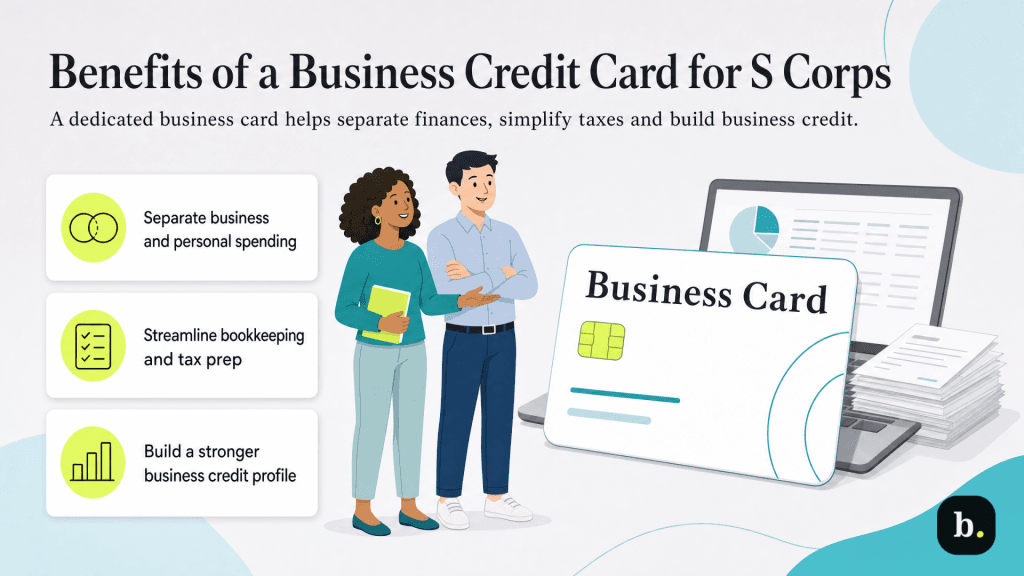

Benefits of a dedicated business credit card for S corps

A dedicated business credit card can do more for an S corporation than provide a convenient way to pay expenses. It can help reinforce the separation between personal and business finances, simplify accounting and bookkeeping and help establish a business credit history. Here are some of the biggest benefits.

1. It keeps business and personal finances separate.

One of the biggest advantages of operating as an S corporation is the separation it creates between you and your business. That separation helps protect personal assets from business liabilities, but only if you consistently treat the company as a separate entity. Mixing personal and business finances can create problems, and in extreme cases may give creditors grounds to argue that the business and owner weren’t truly operating separately.

A dedicated business credit card can help reinforce that separation by keeping business purchases in one place. It’s worth keeping expectations realistic, however. A business credit card isn’t a liability shield on its own. Most business credit cards require a personal guarantee, which means you’re still personally responsible for the debt if the business can’t pay it. The real benefit is helping maintain a clear separation between personal and business finances.

2. It simplifies accounting, bookkeeping and tax preparation.

When business purchases flow through a single account, it’s much easier to track expenses throughout the year. Instead of sorting through multiple accounts to identify company purchases, a dedicated business credit card gives you one centralized record of company spending. Every purchase appears on the same statement, making it easier to review transactions, categorize expenses and spot discrepancies before they become bigger problems.

That can save time when reconciling business bank accounts, preparing financial statements and working with your accountant. It’s especially helpful for S corporations, which file Form 1120-S and issue a Schedule K-1 to each shareholder. Keeping expenses organized throughout the year can make tax preparation smoother and reduce the risk of mistakes when reporting business income and deductions. It can also help create clearer documentation showing that operating expenses are separate from shareholder distributions and payroll expenses.

3. It can help build business credit.

Used responsibly, a business credit card can help an S corporation establish a business credit profile under its own name. Some issuers report account activity to commercial credit bureaus such as Dun & Bradstreet, Experian Business and Equifax Business, allowing the company to begin building a business credit score and a track record of responsible repayment.

Making payments on time can help strengthen the company’s credit history over time, which may prove useful if you seek financing or business loans in the future. It’s also worth paying attention to where the issuer reports account activity. Some report only to commercial credit bureaus, while others may also report to personal credit bureaus, especially when a personal guarantee is involved.

Beyond helping keep finances organized, many business credit cards offer perks such as cash-back rewards, employee cards with spending controls and tools designed to help businesses detect and respond to

credit card fraud.

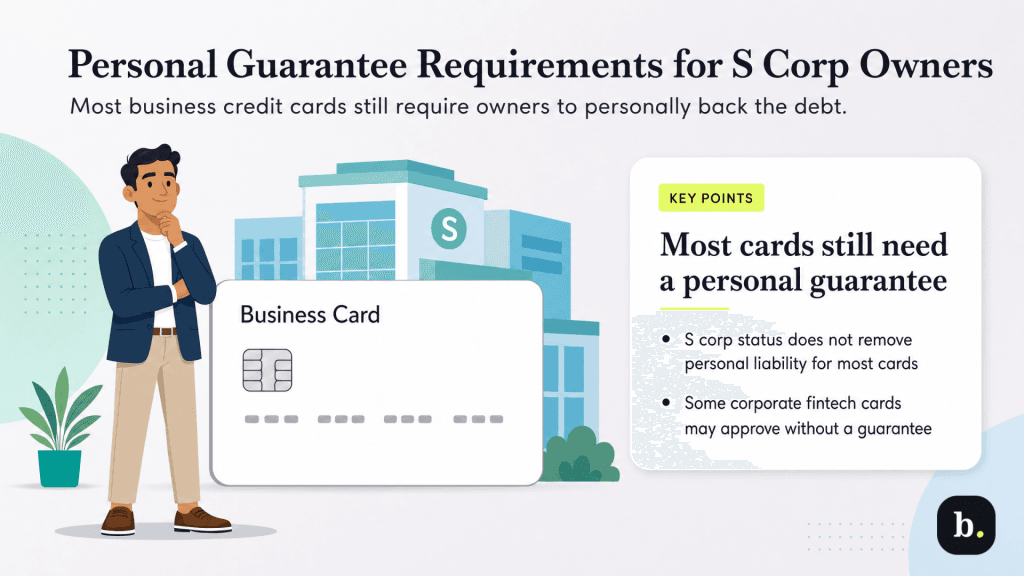

Personal guarantee requirements for S corp owners

One of the most common misconceptions among S corp owners is that corporate status automatically eliminates personal liability when applying for credit. In reality, that’s usually not the case with business credit cards.

Most business credit card issuers require a personal guarantee, even when the business is an established corporation or LLC. That means you’re personally agreeing to repay the debt if the company can’t. The requirement is common across the business credit card industry because most cards are unsecured, giving issuers little recourse if the account goes into default.

In practical terms, forming an S corp helps create legal separation between you and the business, but it doesn’t automatically shield you from liability tied to a personally guaranteed credit card.

When you may be able to avoid a personal guarantee

There are exceptions, but they’re generally found in the corporate card arena. Several fintech companies, including Brex and Ramp, focus more heavily on the business’s finances than the owner’s personal credit, which can make approval without a personal guarantee possible.

To qualify, you’ll typically need an established U.S. business entity, a business bank account and strong financials. Many providers look at factors such as cash reserves, revenue and spending activity when evaluating applicants. For established S corps with healthy finances, these cards can provide a way to separate business borrowing from personal credit. Just keep in mind that many are structured as charge cards, meaning balances generally must be paid in full each billing cycle.

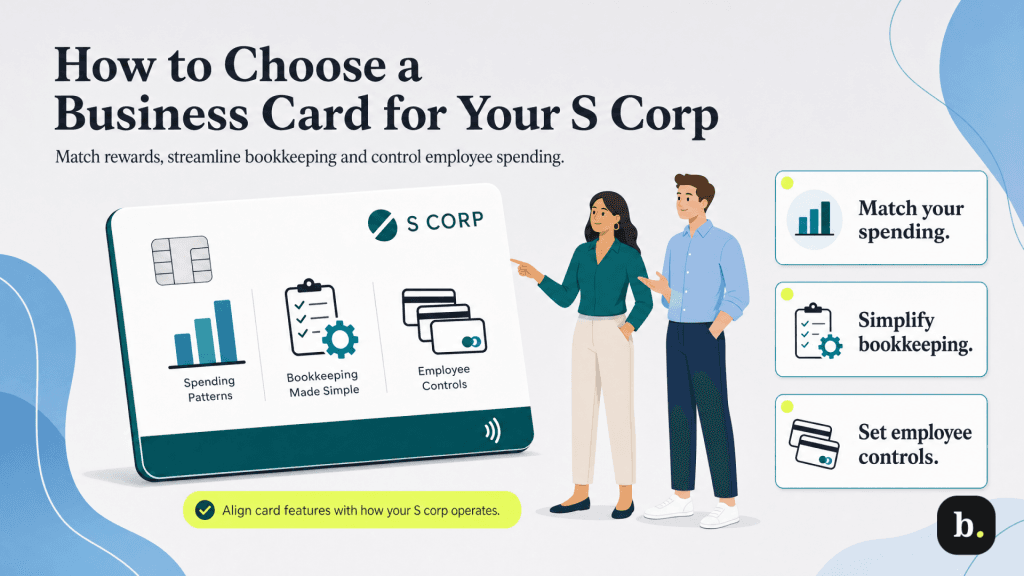

Top considerations when choosing a card for your S corp

Not every business credit card is a good fit for every S corp. The right choice depends on how the business spends money, how you manage your finances and whether you’ll be sharing the card with employees. Here are some of the most important factors to consider.

1. It should match your spending patterns.

The best rewards program is the one that aligns with where your business actually spends money. Review your largest expense categories — such as travel, advertising, software subscriptions, shipping or office supplies — and look for a card that offers elevated rewards in those areas. If your spending is spread across multiple categories, a flat-rate cash-back card may provide more consistent value.

2. It should make bookkeeping easier.

For many S corps, bookkeeping and expense tracking are just as important as rewards. Features such as automated expense categorization, receipt capture, integrations with the best accounting software and exportable reports can save time throughout the year and make tax preparation more manageable.

3. It should give you control over employee spending.

If employees need access to company funds, look for a card that allows you to issue employee cards with customizable spending limits and controls. These features can help prevent overspending, improve visibility into company expenses and make it easier to keep transactions properly documented.

Application tips for S corps

Applying for a business credit card as an S corp isn’t dramatically different from applying as any other type of business structure. Still, gathering a few key documents ahead of time can help the process move more quickly.

What documents should you have ready?

Most applications will ask for basic information about the business, including your EIN, legal business name, formation details and recent revenue figures. Some issuers may request additional documents if they need to verify the company’s information.

If you’re applying for a corporate card that evaluates business financials rather than relying primarily on a personal guarantee, be prepared to provide additional information such as recent financial statements (such as a cash flow statement and profit-and-loss statement), cash balances or details about how the business is funded.

How can you improve your approval odds?

The type of card you’re applying for matters. Traditional business credit cards usually place a lot of emphasis on the owner’s personal credit because a personal guarantee is often required. Corporate card issuers tend to spend more time evaluating the business itself, looking at factors such as revenue, cash reserves and overall financial stability. Either way, having accurate information readily available can help the application process go more smoothly.

Use the card to support your S corp structure

By itself, a business credit card isn’t anything magical for an S corporation. The real value comes from how you use it. Keeping business purchases on a dedicated card can make bookkeeping easier, create a clearer record of company expenses and help the business establish its own credit history.

Most cards still require a personal guarantee, so the card doesn’t replace the protections that come with operating as a separate business entity. Instead, it works best as one more tool for keeping the business and owner financially distinct.

When choosing a card, focus on the features that fit how your business actually operates, whether that’s rewards in your biggest spending categories, stronger expense-management tools or employee spending controls. And if your S corp has established financials and avoiding a personal guarantee is a priority, a corporate card that underwrites the business rather than the owner may be worth exploring.