Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Employer Health Insurance: Average Employee Health Insurance Cost in 2025

Discover how employer-sponsored health insurance works, including current rates and what prices in 2024 mean for employers.

Table of Contents

Employee health insurance benefits are a must-have for many workers. While health benefits are available through health insurance marketplaces or federal programs, the cost of private health insurance has gone up, leaving many Americans without viable options outside of employer-sponsored coverage. This means that the insurance benefits an employer offers as part of a compensation management program — as well as how the costs of that insurance are shared with the employee — can directly impact a business’s ability to hire and retain the right people.

Below, we break down the current state of employer health insurance costs in the U.S., including how to keep expenditures down and what health insurance prices in 2025 mean for employers.

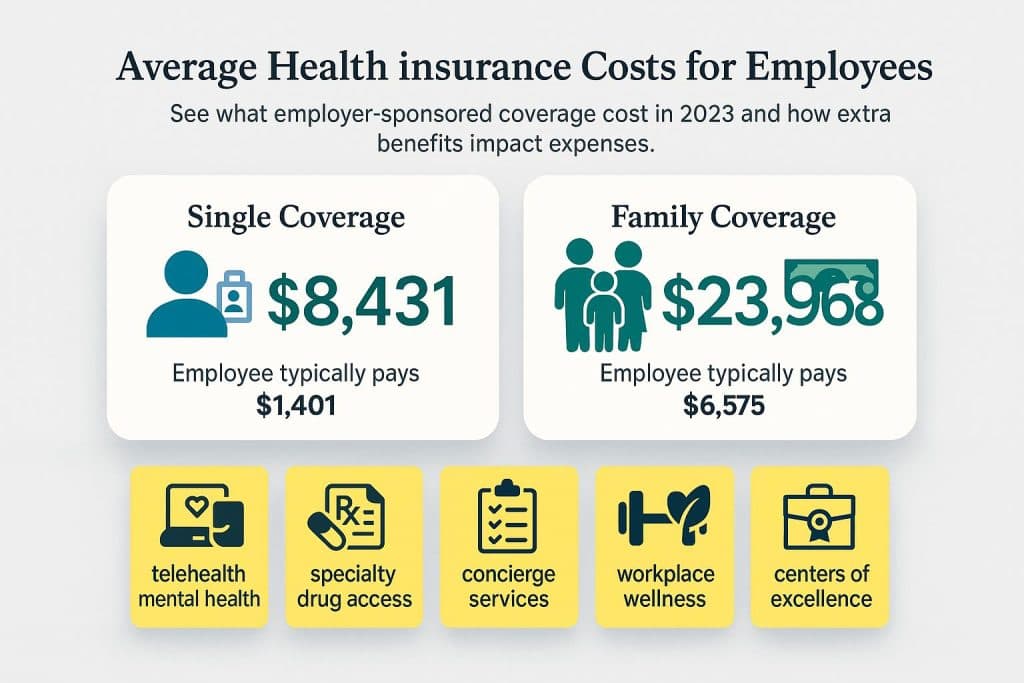

How much does health insurance cost for employees?

According to the Kaiser Family Foundation (KFF)’s 26th Employer Health Benefits Survey, the average annual premium cost for an employee in 2024 for employer-sponsored health coverage increased by 6 percent to $8,951 for single coverage and $25,572 for family coverage, up another 7 percent from the previous year. On average, employees covered $1,368 (16 percent) of the premium for single coverage and $6,296 (25 percent) for family coverage, slightly less than they did in 2023.

At the same time, some employers are looking to decrease their employees’ healthcare expenses by covering treatments or expanding what they offer. These services could be considered fringe benefits:

- Telehealth behavioral mental health services

- Specialty drug access, including GLP-1 drugs for weight loss

- IVF and other family planning services

- Concierge services

- Health and wellness promotions within the workplace

- Access to centers of excellence

- Working spouses surcharges

How much does health insurance cost for employers?

Assuming employers shoulder price increases without increasing the burden on employees or adopting other cost-saving measures, the average health insurance cost for employers is expected to surpass $16,000 per employee in 2025, according to Aon. This represents a 9 percent jump from the year prior and is even greater than the 6.4 percent increase in employer healthcare budgets between 2023 and 2024.

Exact costs depend on a variety of factors, such as the state where the business is located or whether the insurance plan is an HMO or PPO. However, medical claims and prescription drug costs are projected to continue to rise overall due to several factors, including sustained economic inflation and the increased use of specialty medications, such as GLP-1 medications for weight loss and diabetes.

How can employers keep health insurance costs down?

Business owners can follow these steps to lower health insurance costs for themselves as an employer and for their employees.

1. Shop around with an insurance agent or broker.

Understanding and choosing the right health insurance plan from the many available options can be confusing, said Michael Stahl, former chief marketing officer at UnitedHealthcare. “The key is to work with an agent who is unbiased and can show you all the options.”

These options may include group health-sharing plans, traditional group plans, ACA marketplace plans or even level-funded plans, which provide rebates at the end of the year if employees have made few health insurance claims.

“By having the opportunity to learn and compare from multiple carriers, you can be sure you are getting the best benefits structure with the best rates available,” Stahl said.

2. Encourage proactive healthcare.

According to Rudolf Berzins, founder and principal of Apex Benefit Group, it costs less to insure people who are proactive about their health. Many insurance companies offer incentives for businesses that encourage their employees to participate in workplace exercise programs or schedule regular visits with their primary care providers. Before selecting an insurance provider, check if any of them will provide discounts or rebates for proactive health initiatives in the workplace.

3. Shift cost-sharing to employees.

To reduce small business insurance costs, employers can choose health plans that shift more of the costs onto employees. While these contributions can be tax-advantaged, this type of plan means a smaller paycheck for the employee. Furthermore, although this strategy can save money for business owners, it may hurt their ability to recruit and retain employees. [Related article: How Much Workers’ Comp Insurance Do You Need?]

4. Encourage employees to look for prescription drug discounts.

“Pharmacy and prescription coverage [have] a tremendous impact on overall insurance premiums,” Berzins said.

In addition to saving money on insurance costs by seeking generic drug alternatives within an insurance plan, Berzins recommended investigating whether the insured can get direct discounts. “Contact the pharmaceutical company directly for possible coupons or discounts.”

How does employer health insurance work?

Through employer health insurance, employees can receive substantial discounts on their health insurance premiums. Employers often subsidize the cost of the insurance plans they offer, making them significantly more affordable to their employees, who can usually sign up for the insurance plan through the company’s HR department.

Typically, employees have a limited range of employer health insurance plans, depending on the health insurance program chosen by the business owner. Companies can opt to provide health maintenance organization (HMO) plans, preferred provider organization (PPO) plans or both.

How are employer-sponsored health insurance costs shared?

Employees are attracted to companies that provide health insurance benefits, but they may be turned off if the financial burden on the worker is too high. “Employer health benefits are such a crucial part of attracting and retaining talent,” Stahl said. “It is essential to get it right.”

Employer-sponsored health insurance costs are generally shared in two ways: premiums and out-of-pocket fees.

Shared employer and employee costs

- Premiums are the amount a person (either the employer, employee or a combination) pays for coverage. They are due at regular intervals, often monthly or quarterly. Some business owners choose to fully cover premiums for their employees, while others subsidize a portion. This means it is almost always cheaper to get health insurance through an employer

- Health savings accounts, or HSAs, are tax-free savings accounts that can be used for future medical expenses. An HSA can be paired with certain high-deductible insurance plans. Employees do not need to spend all of the money in their HSA every year, as the funds can be rolled over. Employees may contribute to an HSA on their own, or an employer may also contribute.

- Flexible spending accounts, or FSAs, are pretax accounts designated for healthcare costs not covered by insurance, including copays and deductibles. FSA funds are set aside by the employer, and the employee must use them by the end of the year. Funds that are not used are sent back to the employer.

Out-of-pocket employee costs

Whether a business owner requires their employees to share responsibility for the insurance’s monthly premiums, employees will almost always still have out-of-pocket expenses for their healthcare.

- The deductible is the amount paid for healthcare services before the insurer begins paying. Most deductibles are yearly amounts. For example, an employee may have a $2,000 annual deductible, which means they must pay out of pocket for $2,000 of medical services before the insurer covers any amount.

- A copayment, or copay, is the amount employees pay directly to a healthcare provider at the time of service. Not all services or plans require copays.

- Coinsurance is the percentage of costs that employees are still responsible for after their deductible, and it applies only to services covered by insurance. For example, if a plan has 20 percent coinsurance, the insurance company will pay 80 percent of each covered medical bill. The employee is responsible for the other 20 percent.

When must an employer offer health insurance?

Technically, an employer is never required to offer PPO or HMO health insurance, and employees are not granted the explicit legal right to demand insurance from employers. However, according to the Affordable Care Act (ACA), any employer with 50 or more full-time employees (those who work 30 or more hours per week), or an equivalent number of part-time employees, must offer health insurance to 95 percent of their full-time employees.

Should an employer fail to meet this stipulation, they must pay a fee per employee per year to the IRS. Additionally, an employer of 50 or more full-time employees who provides health insurance to one employee is legally obligated to do so for all “similarly situated” employees, meaning employees with similar titles, salaries and job duties.

Under the ACA, employer-sponsored health coverage must also be available to the employee’s dependents. Biological and adopted children under the age of 26 qualify as dependents, but spouses, stepchildren and foster children generally do not.

Can an employee opt out of an employer’s health insurance?

In almost all situations, an employee can opt out of an employer’s health insurance. Exceptions may occur if an employment or union agreement requires an employee to use the employer’s insurance. In rare cases where the employer entirely covers employees’ health insurance premiums, opting out may be subject to specific waiver procedures.

Two common reasons why workers opt out of an employer’s health insurance offering are that they are already covered by a spouse or family member’s insurance, or there is a limited range of medical services covered. For workers who decline employer-sponsored insurance in favor of marketplace insurance, the premiums and plan options are determined in part by the individual’s income.

What health insurance changes are there in 2025?

Employer-sponsored health insurance rates have increased steadily in recent years, a trend expected to continue and amplify in 2025. These rate increases are likely to impact employers and employees alike, so adopting cost-saving measures can be particularly beneficial for small business owners and their teams.

According to Mercer’s National Survey of Employer-Sponsored Health Plans, employers can expect a third year of high healthcare costs. The total cost per employee is expected to increase an average of 5.8 percent (or, if they take no cost-saving actions, by about 7 percent). Experts predict that small-to-medium-sized businesses with 50-499 employees will be hit the hardest, averaging about a 9 percent increase in healthcare costs.

One contributing factor to this rise is the residual impact of inflation. Because contracts between insurers and medical providers tend to be locked in for multi-year spans, economic changes tend to have a delayed effect on the healthcare industry.

Other factors driving the cost of healthcare (and subsequently, insurance rates) include:

- The healthcare pay transparency requirements of 2021, which may have unintentionally spurred price-gouging tactics between providers and insurers. Healthcare providers can now see the higher prices other provider groups negotiated from an insurer and may decide to follow suit.

- More Americans are returning to pre-pandemic levels of accessing care, thereby increasing services rendered.

- The increased incidence of chronic and more expensive conditions, along with delays in medical services, necessitate longer, more frequent and more complex care.

- A spike in the use of specialty drugs, including those for diabetes and weight loss, drives up the costs of these medications.

- The nationwide healthcare worker labor shortages and hospital consolidations. Analyses from the Peterson-KFF Health System Tracker found that these shortages have led healthcare providers to increase contractual costs for hospital services.

On the other hand, several factors may help mitigate continually rising healthcare costs, including:

- The increased availability and usage of biosimilar drugs in place of biologic medications to help treat MS, Crohn’s disease, IBS, ulcerative colitis and other diseases. Similar to a generic medication, biosimilar drugs are almost identical to FDA-approved biologics, but are faster and generally less expensive to develop.

- Exploring a holistic approach to reduce the cost of care. Rather than implementing short-term fixes to low-hanging fruit problems, such as cutting administrative costs, research from PwC found that health plans are increasingly establishing dedicated roles to examine overall medical costs and seek ways to improve operational efficiencies and medical management processes.

Although deductibles are continuing to increase, there are also more cost-sharing options between employers and employees, Berzins explained. This increase in options means business owners can make more plans available to their employees than in prior years. In many cases, this has lowered the costs for employers.

Meanwhile, employees can reduce their expenses by choosing different tiers of insurance within their group health plan, said Berzins.

There is a definite upside for employees who don’t have many medical expenses: “These changes will help stabilize premiums,” said Berzins.

What is the minimum employer contribution for health insurance?

The ideal contribution percentage for your business will depend on your industry, the size of your company and the types of health insurance benefits you offer. Consider researching contribution rates in your geographic region and for your type of business, and comparing those with what you can provide while remaining profitable.

Julianna Lopez and Sean Peek contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.

- HR Compliance Challenges Small Businesses Face Today

- How to Hire and Staff for Your Business

- Drinking on the Job: Small Business Guide to Creating an Office Alcohol Policy

- What to Do if ICE Serves Your Business With a Form I-9 Audit

- How Offering Professional Development Opportunities to Employees Helps Your Small Business