Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

A strategically developed business growth plan can set your business on a path toward long-term profitability.

When you run a business, it’s easy to get caught up in daily operations and focus only on what’s in front of you. But sustainable success requires looking ahead and planning for growth. That’s where a business growth plan comes in. It should map out a defined period and pinpoint how you’ll expand your company and increase revenue.

Business.com’s business growth plan guide details exactly what to include in your growth plan, along with actionable advice from business strategy experts.

A business growth plan is a written strategy that outlines where a company wants to go and how it will get there, including its goals and growth tactics. Business owners and leadership teams need to think beyond day-to-day operations and plan intentionally for growth if they want their company to thrive long term. Creating a useful business growth plan takes time, but it helps keep expansion efforts on track and can pay off significantly.

“A business growth plan is a clear, step-by-step guide for how a company will grow,” explained Sachin Puri, CEO of Bluehost Group and Network Solutions. “It shows where the business wants to go, how to get there and what’s needed to make it happen. Think of it as a map to success.”

Puri noted such plans are especially important when a business is trying to grow fast, expand into a new market or deal with substantial changes.

Though similarly named, a business growth plan is not the same as a traditional business plan. In short, a traditional business plan focuses on launching or stabilizing a business, while a growth plan focuses on scaling your business as it matures.

“A business growth plan vs. a generic business plan reflects an organization that is trying to grow faster than its market space or do something strategically interesting, different or important in that year, not just growing a little bit,” said Mariann McDonagh, president of McDonagh Growth Associates and operating partner at Edison Partners, a growth equity firm.

McDonagh explained that a growth plan is used when a company wants to expand its customer profile, enter adjacent markets or pursue initiatives that require new strategies and resources. In contrast, entrepreneurs typically create standard business plans when launching a new venture to define their core business model or secure initial funding.

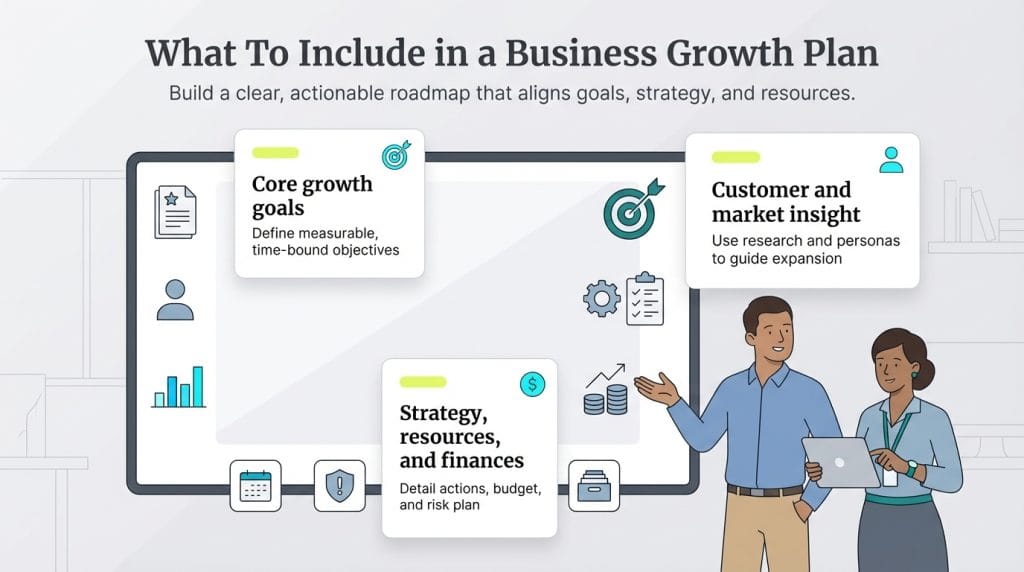

We spoke with chief growth officers (CGOs), chief strategy officers (CSOs) and other business professionals about developing and writing business growth plans. Based on their expertise, we recommend including the following elements in your growth plan.

The executive summary sets the direction for your entire business growth plan, outlining why the plan exists, what you want to achieve and how you’ll get there.

Johannes Heinlein, CGO at Project Management Institute (PMI), says a successful business growth plan should be clear and actionable so it can lead to a positive impact. “It typically begins with an executive summary that explains why the plan was created, identifies key growth opportunities and outlines the desired outcomes,” Heinlein said.

Soren Godbersen, CGO at Lightstone, said you should aim to give a high-level overview of goals and strategies in your executive summary. “There will be plenty of opportunities to go into detail in subsequent sections,” Godbersen explained.

No business can succeed — much less grow — without a clear understanding of its customers. Growth experts we spoke with recommend developing ideal customer profiles (ICPs) and including that information in the customer analysis section of your growth plan.

When you understand your target audience‘s needs, wants and preferences, you can make smarter decisions about how to expand and drive revenue. Your customer analysis section should outline your customer personas and explain how they relate to your growth plans. For example, if your research shows there’s no demand for a new product, that’s a sign to rethink the expansion before you invest time and money in it.

Is the time right for your business to expand its revenue sources? What are your competitors doing, and can your team potentially do it better? Or what aren’t rivals doing that your company could capitalize on? To answer these questions, you’ll need to conduct both a market analysis and a competitor analysis.

In this section, Heinlein recommends examining market trends, highlighting competitive positioning and outlining opportunities for future growth. “This analysis will provide a strong foundation for setting clear, measurable goals that align with the organization’s mission,” Heinlein said.

This section defines the specific milestones your company aims to hit based on what you uncovered in your analyses. This is where you translate your customer, market and competitor insights into clear, measurable goals.

Companies often use the SMART goals framework in their business plan, and that approach is also ideal for business growth plans. That way, you’ll be setting objectives that focus on the specific growth you want to achieve and when you want to achieve it.

Your growth objectives are the whole point of your business growth plan. You should be able to clearly explain what the objective is, why you’re targeting it and how you’ll measure success. You’ll also want to highlight the key performance indicators (KPIs) you’ll use to track progress, such as revenue growth, customer acquisition or retention.

In this section, you’ll detail how you’ll reach your objectives, from the macro to the micro. Think of this part as a project management plan where you break down every strategy, process and deliverable. Defining the specific tactics your team must execute is vital to moving from ideation to completion. For example, you might outline how you’ll launch a new product, expand into a new market or improve customer retention, along with who owns each initiative and when it will happen. These tactics should tie directly to the KPIs you defined earlier.

Heinlein cautioned that organizations often spend too much time identifying opportunities and not enough time executing on them. “By including key principles of project management, a growth plan can be both structured and adaptive, ensuring opportunities are successfully realized,” he said.

McDonagh advocates specifying what each department in your business will be responsible for. “With any really good growth plan, the organization will be involved across all of the functional areas,” she said.

Achieving your growth objectives may require a range of tangible and intangible resources. Use this section to outline the specific resources each department will need, such as new software, additional team members or a defined number of staff hours. Other necessary resources may include raw materials or physical equipment. You’ll use these inputs to estimate costs in the next section of your growth plan.

Godbersen recommends grounding your growth plan in clear, realistic financial assumptions. That detail matters, especially as the Federal Reserve Banks’ 2025 Report on Employer Firms (based on the 2024 Small Business Credit Survey) found that 94 percent of employer firms reported at least one financial challenge in the prior year.

At a minimum, your financial projection section should cover:

Every growth plan should flag the biggest risks and explain how you would manage them. This section shows investors, lenders and internal stakeholders that you have thought through potential obstacles, such as the following:

For each risk, include a brief mitigation plan, so readers understand how you would respond if challenges arise.

Set a clear timeframe for when you want to achieve your growth objectives, then map out the steps needed to get there. Develop a timeline that divides the initiative into phases with specific milestones and deadlines. This approach helps you turn big-picture goals into manageable steps and track progress along the way. Be realistic about how long each step will take so your plan feels doable, not overly ambitious.

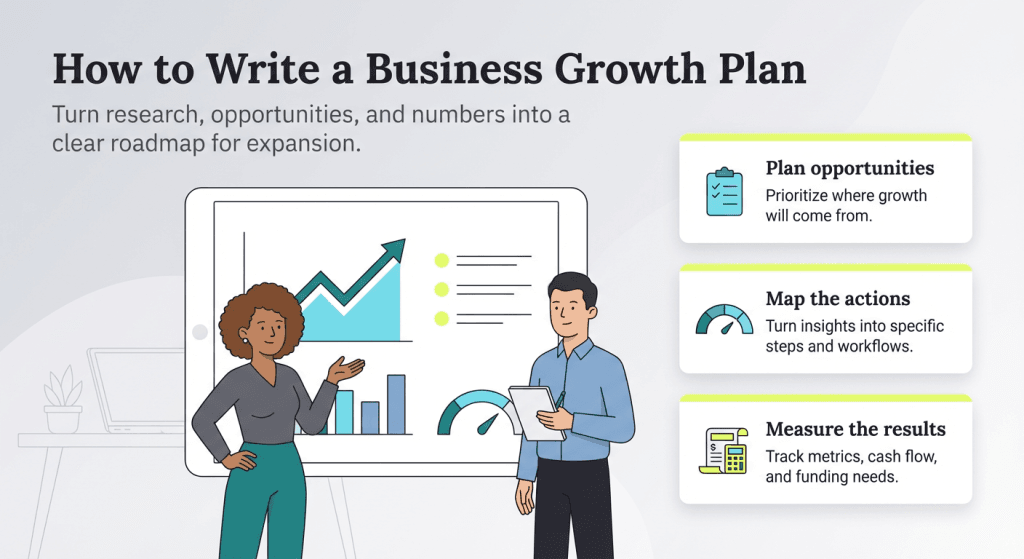

Now that you know what elements to include in your growth plan, it’s time to put it all together. Here are the steps to follow when writing a business growth plan.

Before you start writing, gather the data you’ll need to support your plan, including:

You should also understand what changes your business will need to make to support those goals, such as hiring, technology upgrades or operational capacity.

Break your growth strategy into clear, actionable steps, so you know what needs to happen and who will do it. For example, outline:

Mark Talens, executive vice president and chief strategy and solutions officer at ParkourSC, recommends moving beyond high-level plans to define exactly how execution will happen.

“Don’t just identify what needs to be done — define specific, automated actions and decision-making processes that will drive results,” Talens advised. “Your plan should specify how you’ll turn insights into concrete actions.”

Decide how you’ll measure success before you start executing the plan. Focus on tracking progress throughout the expansion, not just the final outcome, so you can see what’s working and where adjustments are needed.

Choose a small set of metrics that reflect both growth and operational health, such as:

Reviewing these metrics regularly helps you spot wins early, catch problems before they escalate and adjust timelines, spending or processes as needed.

A strong growth plan is practical, focused and grounded in how your business actually operates. Keep these tips in mind as you write.

Growth often means entering new markets or expanding your offerings, but it shouldn’t come at the expense of your core identity. Your plan should clearly connect back to what your business does best and why it exists in the first place.

For example, it would feel off-brand if The Coca-Cola Company tried to grow by launching a video game. That kind of move would likely confuse employees and customers alike.

As Heinlein puts it, a growth plan should be clearly linked to your organization’s mission and vision, with those elements guiding how the plan is carried out. That alignment helps employees, leadership and stakeholders understand not just what the company is doing, but why.

It’s hard to map out how you’ll grow if you haven’t defined what success looks like. Before filling in the details, get clear on the end goal, whether that’s revenue targets, market share or expansion into a new segment.

McDonagh recommends starting with the end in mind and working backward, especially when entering a new market. For example, if a company wants 25 percent of its revenue to come from that new segment, the plan should spell out what needs to happen to reach that number, step by step.

A growth plan only works if your business is set up to support it. Before moving forward, take a realistic look at whether you have the people, tools and systems needed to carry out the plan. This is where the earlier sections we explained, like resources required and strategies and processes, come into play. If roles aren’t clearly defined, workloads are already stretched or key tools are missing, even a strong growth plan can stall quickly.

Use this step to identify gaps early and decide what needs to be in place before you begin, whether that’s hiring, upgrading technology or adjusting internal processes.

Your growth plan shouldn’t be static. Treat it as a working document that you revisit as you hit milestones, miss targets or uncover new information. Set specific review dates so you can look at results and decide whether to stay the course or adjust.

As markets shift and new challenges emerge, your plan should be flexible enough to adjust without losing sight of your core goals. Small course corrections, such as reallocating resources, revising timelines or adjusting priorities, can help you stay resilient and keep momentum without starting from scratch.

For many companies, a growth plan is essential for securing capital. Investors want to see how the business plans to scale sales and generate revenue over defined periods. But even without outside funding, a growth plan helps clarify where the business is headed and how it plans to get there. Companies are more likely to succeed when expansion decisions are documented and intentional, not reactive.

The numbers back that up. According to 2024 data from the U.S. Bureau of Labor Statistics, about 20 percent of new businesses fail within their first year, and roughly half fail within five years. Poor planning is a common factor. Writing a growth plan helps business owners catch problems early and make clearer decisions.

Heinlein emphasized the importance of defining and measuring success early. “Setting goals, putting a performance measurement system in place and tracking progress almost doubles the chances of success,” Heinlein said.

Max Freedman contributed to this article. Source interviews were conducted for a previous version of this article.