Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

From credit scores and income requirements to secured cards and corporate cards, here's what you need to know before applying.

Getting approved for a business credit card isn’t always as straightforward as meeting a single credit score requirement. Issuers look at a combination of factors, including your personal credit history, business revenue, time in business and overall financial profile. The good news is that approval standards vary widely, which means there are options for startups, newer businesses and owners who are still building credit.

This guide breaks down the requirements most issuers consider, what credit scores and financial qualifications they typically look for, and what you can do if you’re not quite there yet.

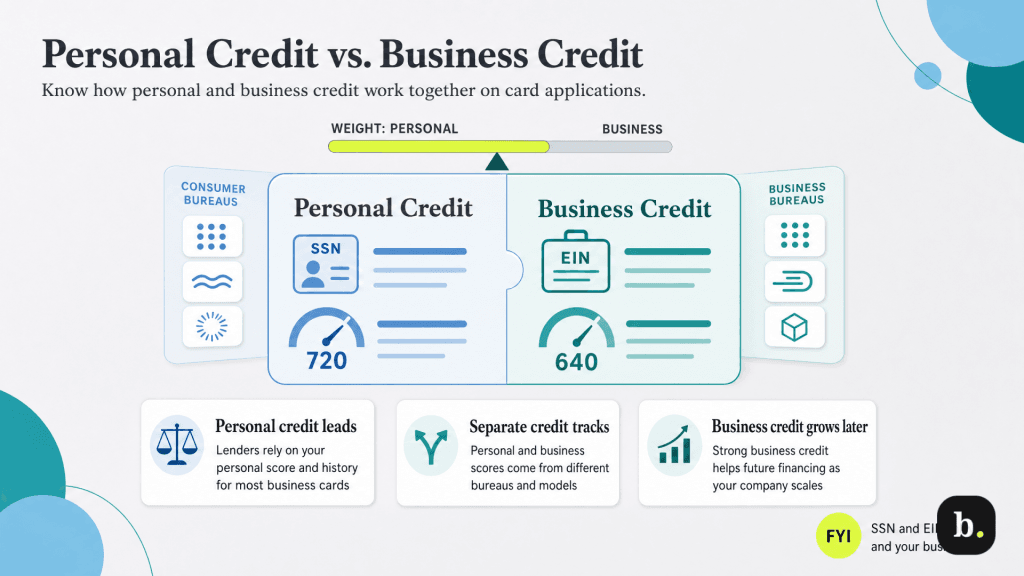

For most business credit card applications, your personal credit score matters more than your business credit score. While issuers may look at some details about your business, your personal credit history is often the first thing they look at.

That surprises a lot of applicants, especially business owners who have spent time building business credit. The reality is that many small businesses simply don’t have much borrowing history for an issuer to evaluate. A personal credit report, on the other hand, often provides years of payment and borrowing data, giving lenders a clearer picture of how an account is likely to be managed.

Most small business credit cards also require a personal guarantee. That means you’re personally responsible for repaying the balance if the business can’t. Because of that added risk, issuers typically place significant weight on your personal credit history and credit score.

Personal and business credit serve different purposes, are tracked by different bureaus and use different scoring models. Understanding how they differ can help explain why most issuers focus on personal credit during the application process. Here’s what to know:

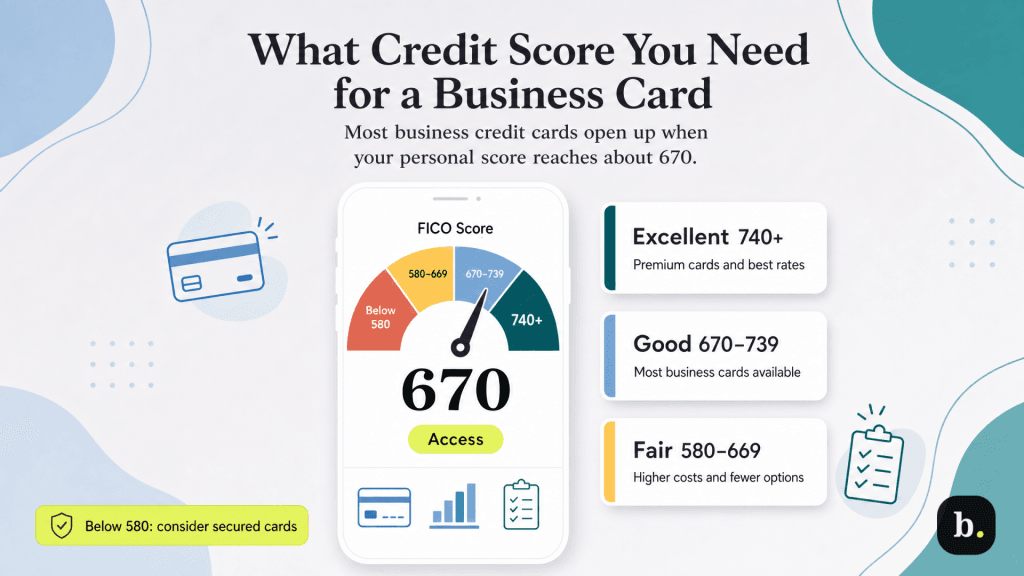

There’s no single credit score requirement that applies to every issuer or every card. However, most business credit cards fall into fairly predictable credit-score ranges. As a general guide:

These ranges should be viewed as guidelines rather than hard rules. Note that some issuers may impose a slightly higher benchmark of around 690 for business credit cards, while others place more emphasis on factors such as income, existing debt and overall credit history. In practice, a personal credit score of about 670 or higher will generally give you access to the largest selection of business credit cards.

One of the biggest misconceptions about business credit cards is that you need substantial business revenue to qualify. In reality, many issuers don’t publish minimum revenue requirements for traditional small-business credit cards. For most applicants, personal credit is far more important than revenue.

That means startups, side hustles and newer businesses can often qualify even if revenue is modest or inconsistent. Revenue may still influence your credit limit, but it isn’t always the deciding factor in whether you’re approved.

Most business credit card applications ask for annual income or business revenue. What you report depends on your business structure and circumstances:

Whatever income figure you provide, make sure it’s accurate. Issuers may verify application information, and intentionally overstating income on a credit application can create legal problems.

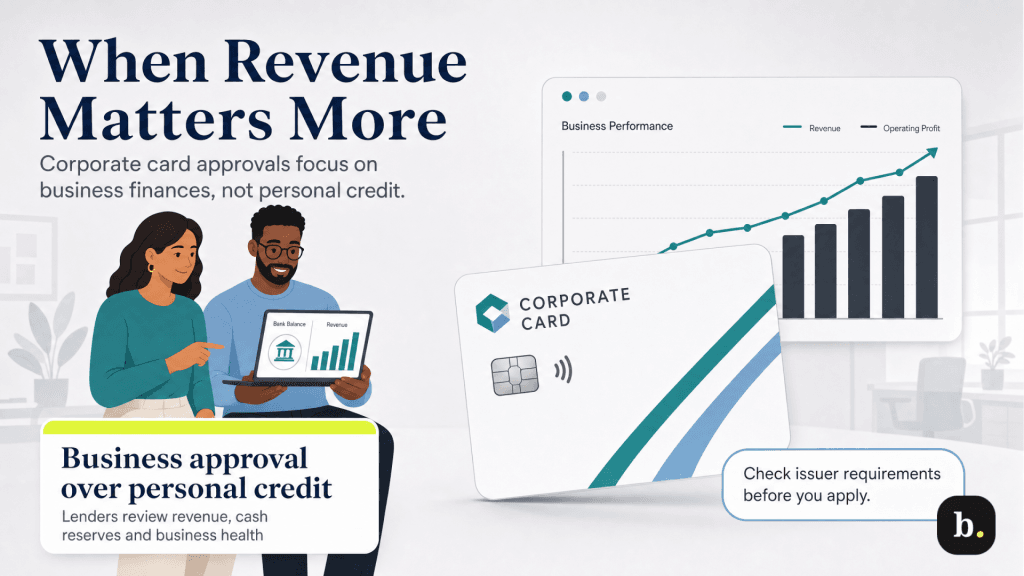

Revenue and cash reserves become much more important when applying for corporate cards that are underwritten based on the business rather than the owner.

Unlike traditional business credit cards, corporate cards from providers such as Brex and Ramp generally don’t rely on a personal credit check. Instead, they evaluate the financial strength of the business itself.

As a result, these products often require minimum revenue levels, cash balances or funding thresholds. Requirements vary by provider and can change over time. For example, Ramp has generally looked for a minimum balance of about $25,000 in a U.S. business bank account, while Brex has cited minimum cash requirements for startups and higher financial thresholds for more established companies. Always confirm current requirements directly with the issuer before applying.

Credit score and income tend to get the most attention, but they’re not the only factors issuers consider. Depending on the card and issuer, details such as how long you’ve been in business, your existing debt and even your relationship with the lender may influence the decision.

Here are a few things to keep in mind:

Not every business owner applies with excellent credit, years of business history or strong revenue. If your qualifications are borderline, there are several steps you can take to improve your approval odds before submitting an application.

Because personal credit is usually one of the most important factors in a business credit card approval decision, it’s worth reviewing your credit before you apply. Many banks, credit card issuers and free credit-monitoring services provide access to your score at no cost. Checking your own credit is considered a soft inquiry, so it won’t affect your score.

Some free services provide a VantageScore rather than a FICO score. The two scores are often similar, but don’t be surprised if the numbers aren’t an exact match. A free score can still give you a good sense of where you stand before applying.

You can also review your business credit reports with commercial bureaus such as Dun & Bradstreet, Experian Business and Equifax Business. Business credit typically plays a smaller role in most small-business credit card applications, but monitoring it can help you identify errors and track your progress over time.

If you’re close to qualifying but not quite there yet, a few changes can strengthen your application:

If traditional business credit cards are out of reach right now, a secured card may help you get your foot in the door. These cards typically require a refundable security deposit and can provide an opportunity to build a stronger credit history over time.

While secured cards generally offer fewer rewards and benefits than unsecured cards, they can provide a path forward. By making on-time payments and using the card responsibly, you may be able to strengthen your credit profile and eventually qualify for a traditional unsecured business credit card.

Many business owners assume they need years of business history or substantial revenue to qualify for a business credit card. In reality, personal credit is often the biggest factor. That’s good news for startups, side hustles and newer businesses that may not have an extensive financial track record yet.

Wherever you’re starting from, the goal isn’t to qualify for every card on the market. It’s to find the cards that fit your current profile, use them responsibly and build toward better options over time.