When you start a business, your personal credit is usually the only credit you have, so it’s natural to lean on it. But the longer your personal and business finances stay tangled together, the more risk you carry: to your personal credit, to your liability protection and to the accuracy of your books. Separating the two isn’t just good financial housekeeping. It’s one of the first steps toward establishing business credit that lenders, vendors and card issuers can evaluate independently of your personal finances.

This guide explains why separating personal and business credit matters and outlines the steps businesses can take to build business credit that becomes less dependent on the owner’s personal credit history over time.

Why does separating personal and business credit matter?

When you’re just starting a business, using personal credit for business expenses may seem easier than setting up separate accounts and financing. However, keeping personal and business finances intertwined can create problems that become more difficult to untangle as the business grows. Separating the two can help protect your personal finances, simplify recordkeeping and establish a stronger foundation for future growth.

Here’s why separating personal and business credit matters:

1. It protects your business from liability.

If your business is organized as an LLC or corporation, that structure can help protect your personal assets from business liabilities. However, that protection depends in part on treating the business as a separate legal entity.

Commingling funds — such as paying personal expenses from a business bank account or using personal accounts for routine business transactions — can blur that separation. While commingling alone doesn’t automatically eliminate liability protection, it’s one of the factors courts may consider when determining whether to “pierce the corporate veil” and hold owners personally responsible for business obligations. Keeping finances separate helps reinforce the distinction your business structure is intended to create.

2. It simplifies taxes.

Keeping business and personal finances separate can make tax preparation significantly easier. When business income and expenses flow through dedicated business accounts, it’s much simpler to identify deductible expenses, track revenue and maintain accurate records.

Otherwise, you may find yourself digging through personal bank and credit card statements months later trying to identify which charges belonged to the business. Separate accounts make those records much easier to track and document.

3. It helps create a more accurate financial picture.

It’s difficult to make informed business decisions when personal and business spending are mixed together. Separate accounts provide a clearer view of revenue, expenses and profitability, making it easier to evaluate how the business is performing.

That visibility becomes especially important when creating budget planning forecasts, setting prices, managing cash flow or deciding whether it’s time to hire employees, expand operations or invest in growth.

4. It helps you build independent business credit.

Business credit is a measure of your company’s creditworthiness that is tracked separately from your personal credit by commercial credit bureaus. Establishing that profile takes time, but it can create valuable financing opportunities as the business grows.

A strong business credit history may help your company qualify for higher credit limits, better financing terms and more favorable vendor relationships. Over time, lenders, suppliers and card issuers may place greater emphasis on the business’s financial track record rather than relying solely on the owner’s personal credit profile.

Many entrepreneurs start out relying on personal credit to

self-fund their businesses. But the longer personal and business finances remain intertwined, the harder it becomes to track profitability, prepare taxes and demonstrate the business's financial performance to lenders.

How to separate personal and business credit

Separating personal and business credit doesn’t happen overnight. Most businesses build that separation gradually by establishing a legal business identity, opening dedicated financial accounts and creating a track record of business credit activity.

The steps below build on one another, so it’s best to complete them in order whenever possible.

Step 1: Formalize your business and obtain an EIN.

The first step toward separating personal and business credit is creating a distinct legal identity for the business. Until that happens, lenders, vendors and credit bureaus have little way to distinguish the business from the owner behind it.

Simply operating under a business name isn’t enough to separate the business from the owner. A DBA (“doing business as”) name can help with branding, but businesses that want a separate legal entity generally form an LLC or corporation.

You’ll also need an Employer Identification Number (EIN), which serves as the business’s federal tax ID. An EIN is one of the primary identifiers used to track your business’s financial activity separately from your personal finances. You’ll need it to open business bank accounts and apply for many forms of financing, including business credit cards and vendor credit accounts. (Although you may need to consider using an SSN vs. an EIN when applying for a business credit card, depending on your needs and status.)

The IRS issues EINs at no cost, and businesses can typically obtain one immediately through the agency’s online application.

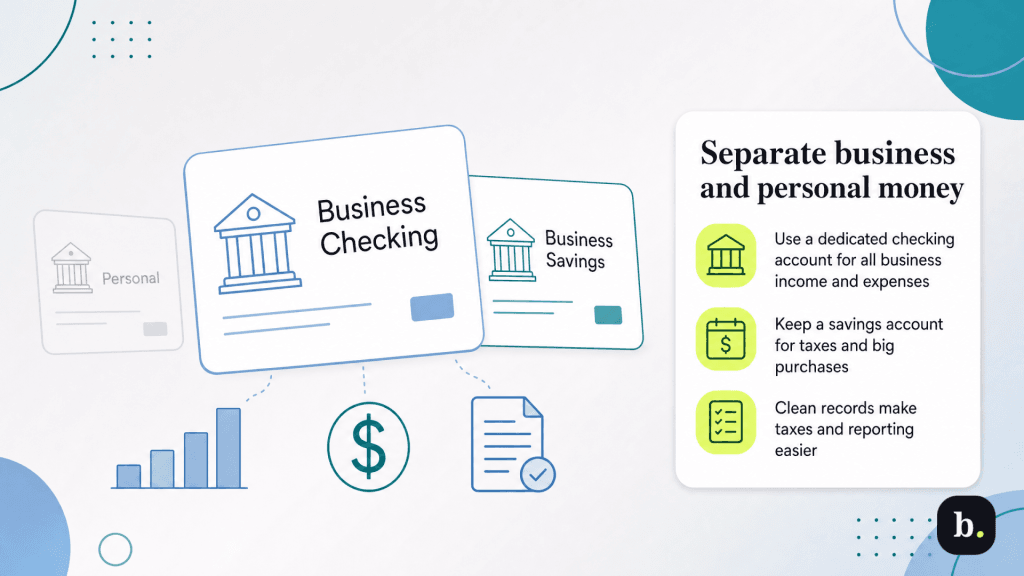

Step 2: Open dedicated business banking accounts.

A business checking account is one of the clearest ways to separate your personal and business finances. Once it’s open, business income should be deposited into that account and business expenses should be paid from it.

Using dedicated business banking accounts creates a clear record of the company’s financial activity and makes it easier to track revenue, expenses and profitability. It can also add credibility when working with vendors, lenders and other financial institutions.

From this point forward, avoid using personal accounts for routine business transactions whenever possible. The cleaner the separation between personal and business finances, the easier it becomes to maintain accurate records, prepare taxes and demonstrate that the business operates as a distinct entity.

Many businesses use a separate

business savings account to set aside money for taxes, large purchases or emergency expenses. Keeping those funds separate from operating cash can make cash flow management easier.

Step 3: Apply for a business credit card.

A business credit card helps extend the separation between your personal and business finances to everyday spending. Using a business credit card for routine expenses can help create a clearer financial record while also contributing to your company’s credit history.

Not all business credit cards work the same way, however. Some issuers report account activity only to consumer credit bureaus, while others report to commercial credit bureaus that track business credit. If building an independent business credit profile and a good business credit score are among your goals, it’s worth understanding how a card issuer reports account activity before you apply.

When possible, use the card only for business purchases and pay it from your business bank account. The more business spending and payments flow through business accounts, the easier it becomes to maintain a clear separation from your personal finances.

As your company grows, you may eventually add multiple business credit cards for different spending categories, departments or rewards programs. Regardless of how many accounts you have, the same principle applies: business spending should stay on business accounts.

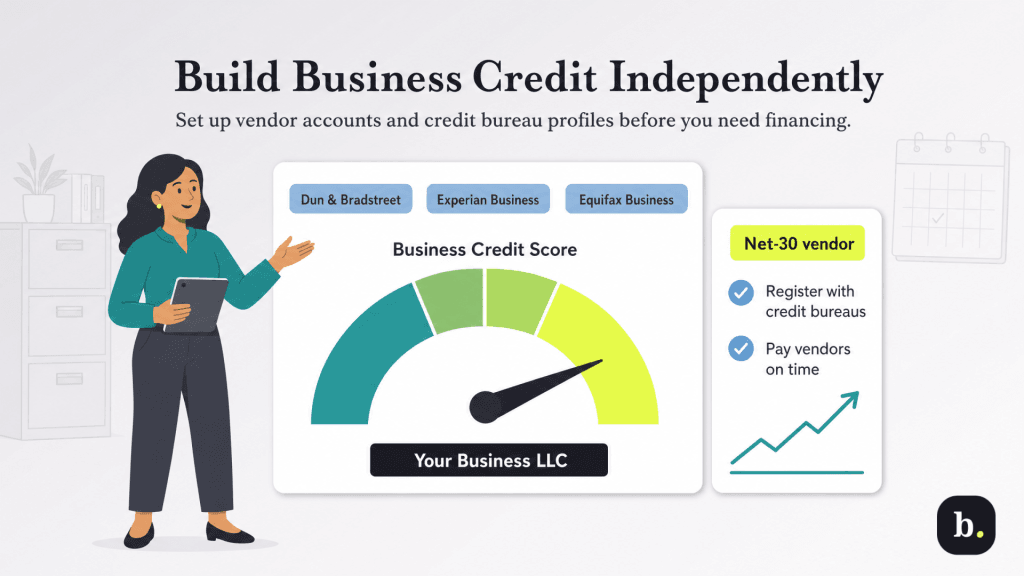

Step 4: Build business credit independently.

Once your business has dedicated banking and credit accounts in place, you can begin building a credit history under the company’s name. Establishing a track record of responsible borrowing and on-time payments takes time, but it can strengthen your standing with lenders, vendors and credit bureaus. Take the following steps:

1. Register with business credit bureaus.

Start by establishing a presence with the major business credit bureaus, which track business credit activity and generate commercial credit reports. Dun & Bradstreet, Experian Business and Equifax Business are among the most widely used.

These bureaus collect information about how businesses borrow and repay debt, then use that data to create business credit reports and scores. Dun & Bradstreet uses the PAYDEX score to evaluate business payment performance. The bureau relies on a D-U-N-S number, a unique business identification number, to identify companies within its system.

Because many vendors report payment activity to Dun & Bradstreet, establishing a profile with the bureau can help ensure those payments are reflected in your business credit file.

2. Establish net-30 vendor accounts.

Net-30 accounts are a form of trade credit that allows businesses to purchase goods or services and pay the balance within 30 days. They are often one of the first credit-building tools available to newer businesses.

A net-30 account is most useful when the vendor reports payment activity to a commercial credit bureau. Otherwise, you could make every payment on time and see little impact on your business credit history. Before opening an account, ask whether the vendor reports payment data and where it reports.

Over time, a history of prompt payments can help strengthen your business credit profile and improve access to business financing, including business loans.

Step 5: Establish policies to maintain separation.

Separating personal and business credit isn’t a one-time project. Once the right accounts and credit relationships are in place, maintaining that separation becomes an ongoing habit.

The most important rule is simple: don’t use business accounts or credit cards for personal expenses, and don’t use personal accounts for business expenses. Every transaction should flow through the account that matches its purpose.

Some expenses can fall into a gray area. A cellphone used for both work and personal calls is a good example. Rather than paying those types of expenses directly from a business account, you could create an expense reimbursement process that documents the business portion and reimburses it separately.

Whatever approach you choose, consistency and documentation help keep your records accurate and maintain a clear separation between personal and business finances.

What to do if your credit is already mixed

Many business owners start out using personal accounts and credit cards to cover business expenses. If that’s your situation, don’t assume you’ve missed your chance to separate the two. Here’s how to deal with the situation moving forward.

- Start fresh from a specific date: Follow the steps outlined above and begin moving business income, expenses and financing activity to dedicated business accounts. The goal isn’t to untangle every past transaction immediately. Instead, establish a clear separation from a specific point in time and maintain it consistently going forward.

- Seek professional help if finances are heavily commingled: If years of personal and business transactions have been mixed together, consider hiring an accountant. A tax professional can help identify business expenses, clean up your records and ensure everything is documented correctly. If liability protection or business-structure questions are involved, consulting a business lawyer may also be worthwhile.

- Expect personal guarantees at first: Many lenders require a personal guarantee from newer businesses, even after you’ve separated your finances. As the company grows and develops its own credit history, lenders may become more comfortable evaluating the business itself.

Give your business its own financial identity

Separating personal and business credit takes time, but every step helps establish the business as its own financial entity. Along the way, you’ll create cleaner records, strengthen liability protection and begin building a business credit profile that supports future financing opportunities.

The principle behind it all is simple: keep business income, expenses and credit activity separate from your personal finances. The more consistently you do that, the easier it becomes for your business to stand on its own.