Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Businesses often live from payroll to payroll, but smart business leaders understand the power of saving for future growth.

When you’re a business owner, you need to think differently about how to use your money and resources. Building and maintaining a business savings account is one way to protect your company and help yourself make better decisions.

A business savings account is an excellent place to store funds you don’t need to access on a daily basis. When you have a robust business savings account, you’ll be able to manage unplanned expenses or financial emergencies better.

You likely have at least one business checking account, but what about a savings account? Let’s look at some benefits of opening a business savings account.

Every business has seasons when sales are slow and you’re short on cash flow. A business savings account is a liquid asset, so you can tap it to pay any expenses if you need to. It’s a good way to help you plan and prepare for the unexpected.

Organizations that withstand the test of time understand there will be periods when they will be tested. Even if your business is thriving today, a sudden change in the market could cause you to lose customers and revenue quickly.

Consumer tastes change and new companies are constantly entering the marketplace. A robust savings account gives companies time to understand market changes and respond in a way that will help them in the long run.

New technology is changing the way business is conducted and companies need a way to pursue new solutions. Exploring new solutions allows your business to grow and expand while companies that can’t afford to do so will be left behind. When you have savings to fall back on, you’re in a position to focus on growth and take advantage of new opportunities as they present themselves.

Good business leaders think about how they need to pivot and change to stay competitive in the market. When you know where to expend your resources, you ensure the business will continue to function optimally. A healthy savings account makes investing in the resources your company needs possible.

Companies continue to grow amid challenging economies and many even thrive during hard times because they have financial resources set aside. The purchase or acquisition of a company going through money issues can provide an excellent platform for growth.

Robust savings also allow companies to obtain the best talent by matching or exceeding what other companies are offering for that position. When companies put money toward recruiting the best talent, they send the message that people matter.

Companies with robust savings can better acquire product knowledge and intellectual property. When a business focuses on gathering the right products or the right intellectual knowledge, that can push the company to stay a leader in its field.

Many businesses miss out on opportunities to give back because they need to use all of their resources to stay afloat. Good companies work diligently to develop their brand generosity. By saving, companies give themselves a wonderful gift in the form of a significant impact on the communities where they operate.

In his book “Start Something That Matters,” Blake Mycoskie, the founder and owner of TOMS, advises readers that the goal isn’t how much money you make, but how much you help people. Companies that develop the habit of saving money will find many beneficial reasons to give back a portion of their profits.

Every business owner should be setting aside a portion of their revenue each month for quarterly and annual tax payments. But if you solely rely on a business checking account, it’s easy to spend that money and go into tax season unprepared.

A business savings account gives you a dedicated place to save for taxes, so you’ll be less stressed when tax season rolls around. This account will also make it easier to track your tax payments and ensure you’re reporting everything accurately.

Every business savings account is Federal Deposit Insurance Corporation-insured up to $250,000, so your money is protected even if that bank fails. This can be a great place to store your emergency fund in case a financial emergency comes up and since you won’t see that money on a day-to-day basis, you won’t be as tempted to spend it.

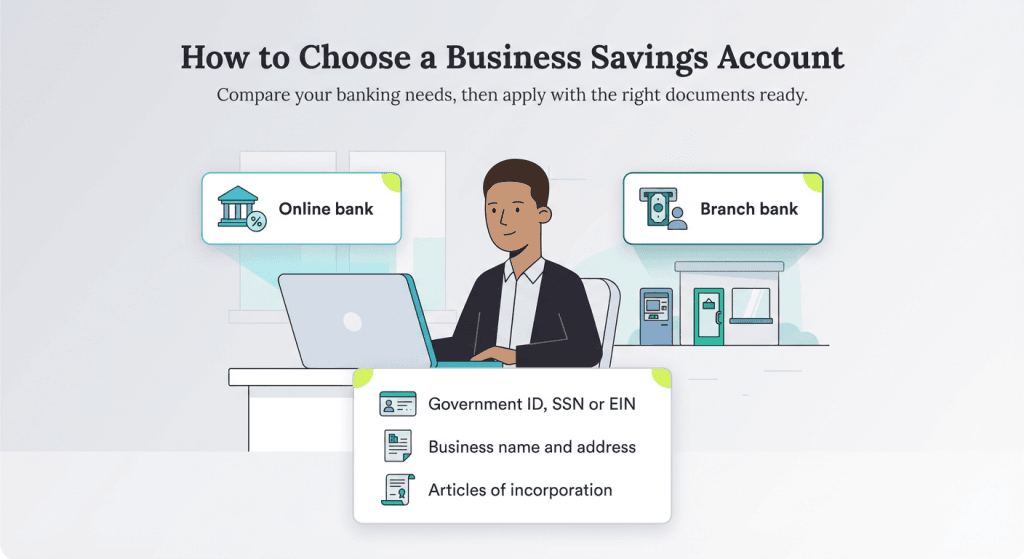

It’s a good idea to research several different banks before selecting where you’ll open your business savings account. The best bank will depend on your goals and personal preferences.

For example, if you value low fees and want to earn interest on your savings, an online bank account is probably the best option for you. If you want ATM access and want to visit the bank in person in case a problem arises, you should probably look for a brick-and-mortar option.

Once you’ve chosen the bank that’s best for you, applying is fairly simple and most banks will let you apply online or in person. Make sure you have the following documentation when you apply:

Here are the four business savings accounts to consider.

The nbkc business savings account earns a 2.75 percent annual percentage yield (APY) and there are no minimum balance requirements. There are no monthly fees and your account comes with checks and an ATM card. But nbkc’s customer service is more limited and it charges a fee of up to $45 for wire transfers.

Capital One offers a 4.11 percent APY promotional rate on its business savings and there’s no cost to open the account. You can make up to six free withdrawals per month and the company has a large network of over 70,000 fee-free ATMs. However, the bank charges up to a $40 fee for outgoing wire transfers.

Live Oak Bank (Member FDIC) offers a business savings account that comes with a 2.85 percent APY and no monthly maintenance fees. It’s easy to open the account and add new authorized signers, and you can manage your account by connecting it to popular accounting software like QuickBooks. However, it’s important to note that the savings account does not include ATM access. See full terms and conditions.

When you sign up for a business savings account with Axos Bank, you’ll be eligible for a $375 bonus. The account earns a 4.01 percent APY and your interest is compounded daily. However, you’ll need a minimum deposit of $1,000 to open the account and if your balance is less than $2,500, you’ll have to pay a monthly maintenance fee.

Once you open a business savings account and begin to set aside money, the next step is to find the right accounting software to manage those savings. The right accounting software lets you manage all of your money on one easy-to-access platform.

Here are four accounting software options to think about:

Ken Gosnell contributed to this article.