Although it’s vital for every business to keep an accurate record of their money, retailers face unique challenges in accounting and maintaining proper financial records: monitoring and calculating the cost of inventory. Though daunting, these tasks are essential to accurate accounting. Read on to learn about the pros and cons of retail accounting, how to calculate the cost of inventory, how to track inventory amounts and more about accounting best practices and tools.

>> Read Next: The Top Accounting Challenges Small Businesses Face

What is retail accounting?

Retail accounting is a special type of inventory valuation commonly used among retailers. As such, the term “retail accounting” is a bit misleading, as it is more of an inventory management method than an accounting method.

In retail accounting, you estimate your inventory’s value rather than calculate it manually. You also assume constant prices, price changes and price change rates across all units of the same item. These assumptions make for quicker calculations that largely eliminate the need for physical inventory counts while at least somewhat accurately suggesting the amount of cash tied up in your company’s inventory.

Searching for accounting software and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

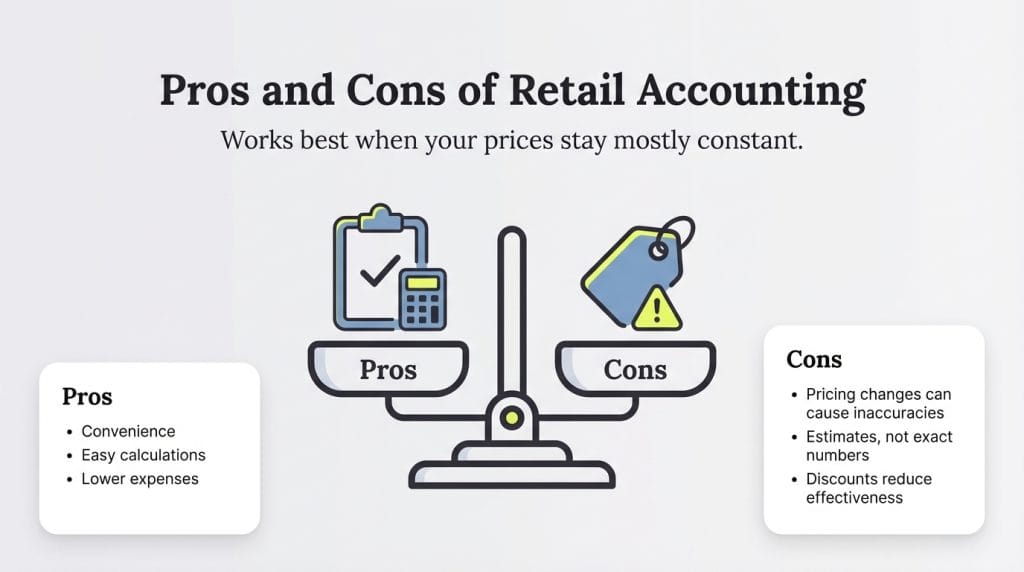

Pros and cons of retail accounting

Retail accounting has some upsides that make it a helpful way of valuing your inventory. However, there are some drawbacks retail businesses need to keep in mind.

Pros of retail accounting

Here are some of the benefits of retail accounting.

- Convenience: With retail accounting, your physical inventory matters less than your knowledge of all your items’ retail prices. If you operate multiple storefronts, this convenience becomes especially important, as you won’t have to spend as much time conducting physical inventories.

- Easy calculations: Because the retail accounting method operates on the assumption that all units of one item are priced the same and experience the same price changes, calculating your inventory’s value is simple. This streamlined calculation makes preparing financial statements far easier as well.

- Lower expenses: Although it’s still important to conduct manual inventory counts, you won’t have to do them as frequently if you practice retail accounting. This can lower your expenses since manual counts require you to either keep your storefront closed while your staff checks your stock or pay them overtime for taking inventory after-hours.

Cons of retail accounting

Some of the downsides of retail accounting include the following.

- Inaccuracies in the event of pricing changes: If the prices of your items change often, retail accounting can be inaccurate. That’s because frequent pricing changes undermine the fundamental assumption of retail accounting — that all units of one item have the same prices, price changes and price change rates.

- Estimates rather than exact numbers: Because retail accounting assumes unrealistic pricing conditions, it provides — at best — an estimate of your inventory’s value. If you need exact price values, retail accounting isn’t likely to meet your needs.

- Ineffectiveness with discounts: Retail accounting assumes a constant markup, so when you run promotions, retail accounting can quickly become inaccurate.

Retail accounting works best when your prices stay mostly constant.

Calculating the cost of inventory with retail accounting

To keep track of your revenue and profit, you must monitor the cost of the goods you sell and the dollar amount of the inventory you have left. There are many methods for calculating costs. Be sure to keep track of which method you use, as you’ll need to know this when it comes time to file your taxes. Also keep in mind that you need to stick with one accounting method for your business from year to year. Any changes in the accounting method you use must be approved through the IRS, generally by filing Form 3115. You can learn more about accounting methods by reading IRS Publication 538.

Below are some methods of calculating the cost of inventory that are valuable for retail accounting.

Inventory: Costing method

One of the key challenges of running a retail business is tracking inventory, especially if you buy multiple inventory units that don’t all cost the same amount. If this is the case, you need to figure out a way to assume the cost of goods sold so that you can compare this to your ending inventory and calculate your profit. To do this, you must make some cost-flow assumptions. Note that this method does not track the physical movement of goods sold but rather assigns cost to the inventory, so you can determine your profit later.

You can do this in various ways. Most retail companies use one of three costing methods to track their inventory. For each of these costing methods explained below, we’ll use the following scenario:

Let’s say you own a game store that sells dice. You have a small bucket of dice that you never allow to go empty. You bought 30 dice at 5 cents apiece, then purchased a second order of 25 dice at 7 cents each and a last order of 15 dice at 10 cents each. In total, you’ve purchased 70 dice. Only 20 are left at the time you track your inventory, and you’re not sure what cost to assign to the 50 dice you’ve sold.

To find out, you should use one of these three costing methods:

1. First in, first out (FIFO)

If you use the FIFO costing method, you take the cost of the first order you purchased, compare it to the revenue you’ve brought in and assign that revenue to the cost of goods sold.

For the above example, you assume you sold the cheaper dice first. Because the 30 dice at 5 cents each were ordered first, you’ll match this against your inventory and assume that 30 of the dice you sold cost 5 cents each. You’ll then assume that the next 20 you sold were from the second order, meaning those dice cost you 7 cents each.

Following the FIFO method, you’ll take 30 and multiply it by 0.05 and add that to 20 multiplied by 0.07. The cost of goods sold is $2.90, and the cost of your ending inventory (the inventory you have left) is $1.85 (five dice at 7 cents, plus 15 dice at 10 cents). The FIFO method would be best to use in this scenario if customers took dice out of the bottom of your bucket.

2. Last in, first out (LIFO)

Because you’re refilling your bucket of dice with your most recent order, it might be possible you’ve sold more of the dice you last put in than the dice you put in first if your customers are taking dice from the top of the bucket. If this is the case, you can use the LIFO costing method. This method is similar in theory to the FIFO method, but instead of matching the cost of the first order of dice to the number of goods sold, you match the cost of the last order of dice to the number of goods sold.

In this case, 15 of the 50 dice you’ve sold would have cost 10 cents ($1.50), 25 of the dice cost 7 cents ($1.75) and 10 dice cost 5 cents ($0.50). When you add these numbers together ($1.50 + $1.75 + $0.50), this would make your total cost of goods sold $3.75 and the cost of your ending inventory $1 (20 dice at 5 cents apiece).

3. Weighted average

It might be more likely that the dice have gotten mixed up in your bucket, and there’s a good chance you’ve sold a number of dice from all three orders you placed. In this situation, you may want to use the weighted-average costing method by dividing the total cost of the dice by the total number of dice you purchased.

In this case, it would end up being $4.75 divided by 70 dice, or approximately 7 cents per die. You know you sold 50 dice, so you match the number of items sold to the average cost of 7 cents, which is a total of $3.50 for the cost of goods sold and $1.40 for ending inventory.

FIFO (first in, first out), LIFO (last in, first out) and weighted average are the three most popular methods for inventory cost tracking.

Inventory: Retail method

Depending on the type of inventory you sell, you may be able to use the simpler retail method to calculate the cost of goods sold and the cost of your ending inventory. If you sell products that have a consistent markup, you can divide the purchase and beginning inventory costs by the cost-to-retail percentage, which is done by dividing the cost of the product by the amount you’re selling it for. Take this number and subtract the sales total multiplied by the percentage, then subtract it from the cost of goods sold to get the ending inventory total.

For example, if you buy collector’s sets of chess for $75 each and sell them for $100 each, the cost-to-retail percentage is 75 percent. If your beginning inventory costs a total of $1,000 and your subsequent chess set purchases cost $2,000 (for a total of $3,000), the relative retail prices would be approximately $1,333 and $2,666, for a total of $3,999 at retail price. Multiply this number by 75 percent and subtract it from the total cost of goods sold (before multiplying it by the cost-to-retail ratio), which is $3,000, and then you have your ending inventory cost of $999.

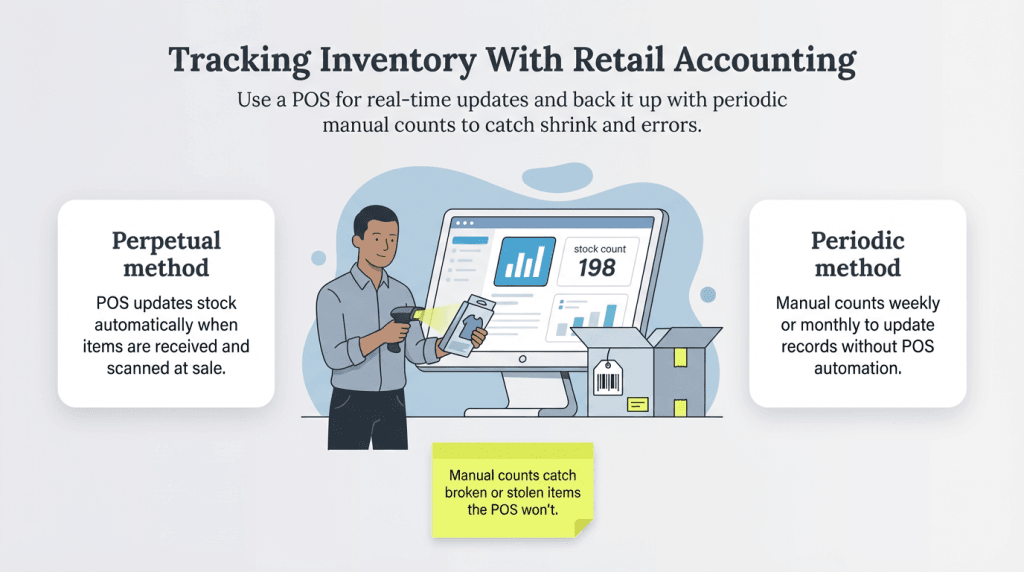

Tracking inventory amounts with retail accounting

Now that you’ve calculated how much you’re spending and making on your inventory, you need to figure out how to keep track of the amount of inventory you have in stock. This helps you do two things: ensure you have enough products in stock to meet customer demand and keep accurate records that will be important for accounting purposes, including taxes.

A POS system can keep track of your inventory without the need for manual counts. See our picks for the

best POS systems.

Below are some methods of tracking inventory that are useful during retail accounting.

Inventory: Perpetual method

The easiest way to track your inventory is via the perpetual method, which keeps track of the items you sell and the ins and outs of your inventory as changes occur. This is done automatically with a fully integrated point-of-sale (POS) system. As you receive inventory, you enter it into the POS system, and the item is assigned a barcode. When the item is sold, the sales employee using the POS system scans the barcode, and at the end of the transaction, the numbers in your inventory log — as well as the costs associated with the item — update automatically. This process can save a lot of time and effort for you and your team.

However, even though the POS system will update your inventory numbers automatically, it’s important to still do manual counts of your products, as the POS program won’t update your numbers for depleted inventory not related to sales. If, for example, a game store employee accidentally breaks a collector’s figurine or items are stolen in a break-in, the POS system can’t account for the loss in inventory because those instances didn’t have to do with ringing up a sale. You should do a manual inventory count at least once a year to keep your records in order, though it may be wise to count monthly and adjust your records accordingly.

If you have an e-commerce store as well as a brick-and-mortar shop, be sure to track inventory across both channels. You’ll want to look for a POS system that can track your inventory on various online stores, like Amazon, in addition to in-person sales.

Inventory: Periodic method

The periodic method of tracking your inventory can be less convenient and more labor-intensive, but it might be preferable if your company can’t afford a fully capable POS system. This inventory-tracking method requires you to manually count and track inventory periodically, such as weekly or monthly. A major drawback of this method is that, because you don’t have a POS system automatically tracking your sales, you don’t have an easy way to determine what items were sold, stolen or broken.

Regardless of the method you choose for determining the cost of goods sold and for counting inventory, it’s vital to keep accurate records and to stay on top of evaluating your inventory and calculating costs. Doing so can save you time at the end of the year when you’re preparing tax statements, and it helps you keep track of your revenue and profits.

Example of retail accounting

To help illustrate the above retail accounting approaches, let’s look at an example. Let’s say you own a hardware store that sells several tools. Let’s also say you have a 30 percent markup on all items, and you know that your inventory was valued at $100,000 last quarter. In this case, if you’ve made $50,000 in sales at the end of your current quarter and purchased $5,000 of new inventory during the quarter, you can use retail accounting to determine your inventory’s value.

To start, we’ll list the key values in this example:

- Initial at-cost inventory value: $100,000

- New at-cost inventory purchases: $5,000

- Total at-cost inventory: $105,000

- Total retail sales: $50,000

- Total retail sales with markup: $50,000 * 30% = $15,000

With these numbers determined, you can estimate your inventory’s value. To do so, subtract your total retail sales with markup from your total at-cost inventory. This gives you $105,000 – $15,000 = $90,000, which is the value of your inventory according to the retail accounting method.

Accounting 101

One of the most important parts of successful accounting — whether you own a retail business or any kind of company — is keeping accurate records. There are three main financial statements you or your accountant need to keep up to date: an income statement, a balance sheet and a cash flow statement. These financial statements are vital for all businesses, not just retail stores.

Most businesses in the U.S. rely on Generally Accepted Accounting Principles (GAAP), so it's critical for business owners to know the basics of

GAAP accounting.

Income statement

On an income statement, you track revenue — all of the money your business is earning. For retail businesses, this comes mostly from customers buying your goods. From the revenue, you subtract the cost of goods sold that you’ve calculated using one of the methods detailed above. The resulting number is the amount you have left to pay your overhead costs. You can track your fixed and variable expenses, like rent or employee salaries, on your income statement as well. [Learn the difference between net income and profit]

Balance sheet

A balance sheet is an essential resource for keeping track of assets, liabilities and equity. On one side of the balance sheet, you list your assets, such as equipment. On the other side, you list your liabilities, such as business credit cards. Your assets minus your liabilities equals your shareholder’s equity, which is the value of your business outside of what you owe. These three things — assets, liability and equity — should always balance one another, hence the name of this document.

Balance sheets are different from income statements. Whereas income statements cover a period of time, like a week, month or year, balance sheets are for an exact date and time.

Cash flow statement

The cash flow statement is similar to the income statement in that it tracks the money that comes in and out of your business. However, the cash flow statement is more specific about when these transactions occur. For example, in your income statement, you might have listed an invoice in your sales, but your client might have 30 days to pay the invoice. The cash flow statement records the actual date the cash is received. Keeping accurate records of your cash flow with this financial statement is crucial to keeping your company afloat.

>> Free Tool: Cash Flow Calculator

Accounting software for retail accounting and beyond

Accounting can be a long and arduous process, especially if you don’t have experience with the various principles and formulas. You can outsource accounting tasks, hire an in-house accountant or try to do the accounting yourself. If you opt to do the accounting yourself, it may be worth looking into accounting software.

Accounting software keeps track of all of your finances, including purchase and sales orders, created invoices, accounts receivable, and accounts payable. Most modern solutions will integrate with your POS system for coordinated inventory and cost tracking. The best accounting software also helps you fill out important financial documents, like income statements, balance sheets and cash flow statements. Accounting programs often assist with accuracy and can be a good way to organize your financial information. You can explore leading accounting software options in our review of QuickBooks Online and our review of Xero.

Always take control of your retail accounting

Keeping track of your accounts has to be one of the top priorities in your retail business. Because of your inventory, accounting can be more complicated, but selecting an appropriate method to determine the cost of goods sold and keeping track of your stock either periodically or perpetually will help. Be sure to use important financial documents, such as income statements, balance sheets and cash flow statements, to monitor your company’s financial health. Accounting software may be able to track your finances and make the accounting process more manageable and help you avoid errors and tax consequences. [Read related article: Accounting Mistakes That Cost Small Businesses Significant Growth]

Mike Berner and Max Freedman contributed to this article.