Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

When Does Your Business Credit Score Matter?

What is the difference between your personal and business credit score, and when does your business credit score matter?

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Many businesses need good credit to be fiscally successful. With good business credit, you’re likely to get more favorable terms with your vendors, credit card processors and lenders. A business credit score measures the overall creditworthiness of a business, much like a personal credit score measures the overall creditworthiness of an individual. While the concept behind each credit score is similar, there are significant differences every business owner should understand.

What is a business credit score?

While distinct from your personal credit score, your business credit score is similar in concept. A business credit score is used to demonstrate how financially sound and reliable a business is. It also shows how likely the business is to make its payments on time.

Like personal credit scores, a business credit score is a numerical measure representing a business’s creditworthiness. However, unlike personal scores that usually range from 300 to 850, business credit scores use a scale of 0 to 100.

Three major credit bureaus determine business credit scores: Dun & Bradstreet, Equifax and Experian. The scores determine creditworthiness for several things, including availability and rates of business loans, credit cards, and payment terms. Strong business credit and a responsible payment history can also reduce the cost of borrowing money.

“Each credit bureau will collect data and information about a company’s financial history and attach a score, but each bureau has a different set of criteria they value when attaching a score,” Jeffrey Bumbales, a marketing consultant, told business.com.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

What is FICO?

FICO (Fair Isaac Corporation) provides a three-digit credit score that lenders use to assess risk and determine your creditworthiness. While FICO is primarily known for personal credit scores, they also offer the FICO Small Business Scoring Service (SBSS), which combines personal and business credit data. Your score dictates the type of business loan you can get, as well as how much you can borrow, for how long and at what cost. It helps companies make quick lending decisions. The higher your score, the greater your chances of getting approved for a loan and the lower your interest rate.

FICO score ranges

FICO SBSS scores range from 0 to 300, with most lenders considering scores above 140 acceptable for small business loans. The Small Business Administration (SBA) typically requires a minimum score of 165 for its 7(a) loans.

Did You Know?

Most of the best small business lenders accept credit scores of 500 and up. A few require higher scores, however. For example, our review of Biz2Credit found that those in need of a loan must have a credit score of at least 650.

This chart shows personal FICO score ranges commonly used by lenders when evaluating business owners for loans:

FICO score

Ranking

Under 580

Poor

580-669

Fair

670-739

Good

740-799

Very good

800 and up

Excellent

How is a business credit score different from a personal credit score?

While the concept behind a business credit score and a personal credit score is similar, they are distinct. A business credit score does not impact one’s personal FICO score, for one. If the business can’t pay back a loan, it won’t affect the owner’s personal credit score. But that is not the only difference between the two. Here’s a look at some more:

Access

Unlike private personal credit scores, business credit scores are publicly available and are attached via an employer identification number (EIN). A personal credit score is tied to your Social Security number. You can obtain an EIN instantly through the IRS website at no cost, and this number becomes the foundation of your business credit profile.

Scoring criteria

Business credit scores are also determined by a different (though sometimes overlapping) set of criteria than personal credit scores, said Luke Voiles, CEO of Pipe.

“Personal credit scores are determined through FICO’s algorithms based on your personal credit history,” he said. “Business credit scores, however, are typically determined by looking at payment history, amounts owed, length of credit history, credit mix and new credit. On the business score side, there is not the same consistency you get with FICO. There are many providers of business scores that are measured and scaled differently, so it can be confusing for small businesses to understand their scores.”

Tells a different story

According to Mike Ross, managing partner at commercial collection agency Miller, Ross & Goldman, a business credit score often reflects whether a business pays its vendors and creditors early, on time, or late.

“A perfect score of 100 indicates that the subject company typically pays 30 days before agreed terms or invoice payment due dates,” he said. “A 90 indicates 20 days before, and an 80 indicates payment on time. Scores below 80 are then progressively reflective of the number of days a company typically pays beyond agreed invoice terms. For example, a 70 is indicative of an average 15 days beyond agreed terms. There are other relevant factors and scoring models on how business credit is calculated, including industry risk, average debt load, years in business and company size.”

Bottom Line

A business credit score and a personal credit score look at different things to ascertain creditworthiness, but both give lenders an indication of your ability to repay a loan. Even if you have a bad credit score, there are business loans you can get.

What is a business credit score used for?

Much like how a personal credit score determines an individual’s borrowing eligibility, a business credit score is primarily useful when a company needs financing. Beyond lending decisions, business credit scores influence insurance premiums, supplier relationships, and even potential partnerships or acquisition opportunities.

“A business’s credit score is usually most important when trying to secure financing,” Bumbales said. “The better a business’s credit score, the more lucrative options it will have when applying for a loan or other financing products.”

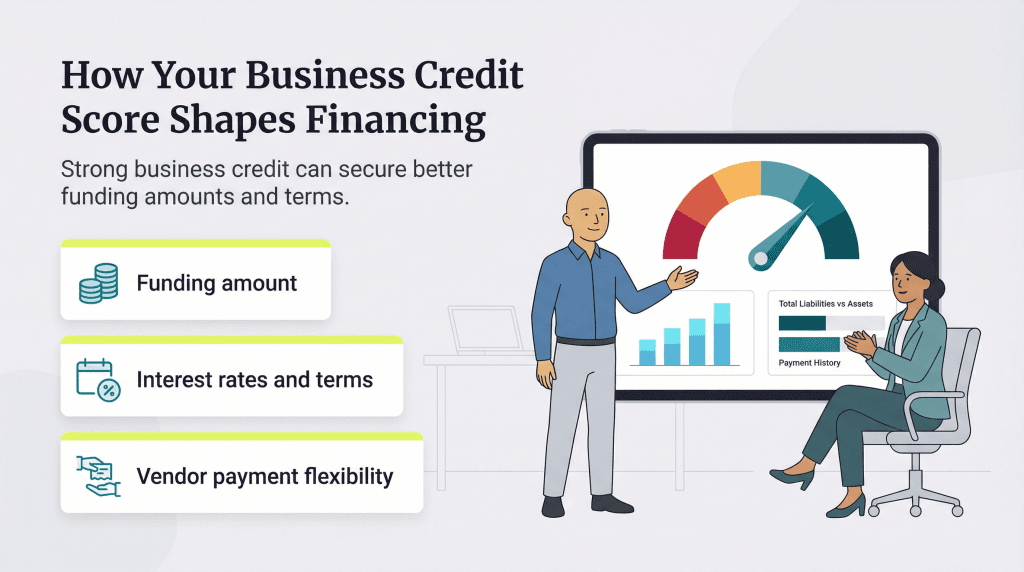

How does your business credit score impact financing and borrowing?

A business credit score can influence multiple pieces of financing a company can obtain, including the amount of funding, repayment terms and interest rate. The score is used to determine whether the lender should extend business credit, how much to lend and the terms.

Other companies you do business with may also use your business credit score to decide whether to extend more generous payment terms.

Considering financing a purchase or borrowing money? It’s essential to understand your current business credit score and how any new funding might impact it in the future.

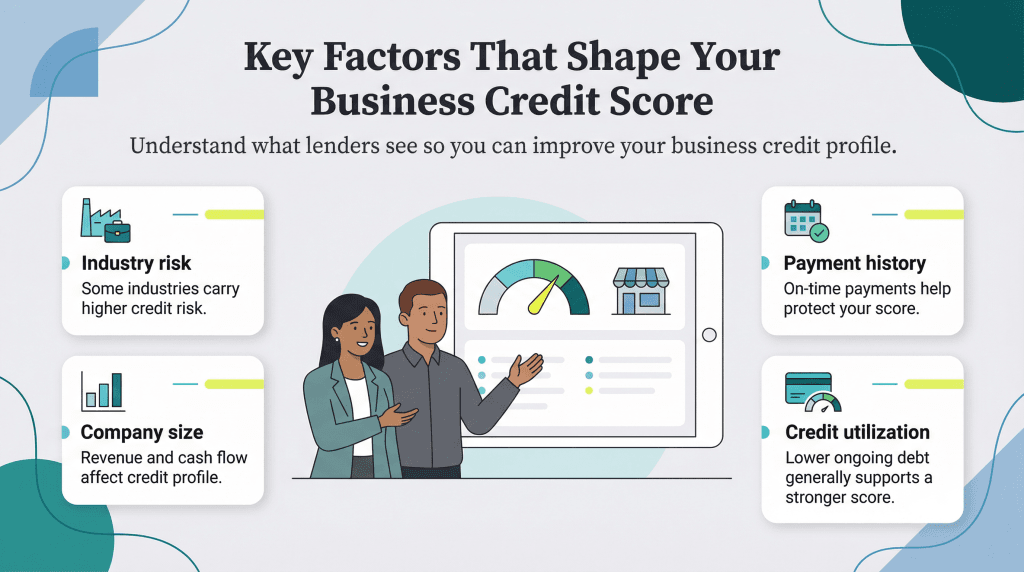

Business credit score factors

While each credit rating agency has its own methods of calculating a business credit score, there are a few common factors.

Industry risk: Even if your business is financially sound and has a strong business plan, operating in a risky industry could reduce your business credit score. For example, businesses in the legal cannabis industry face legal challenges many other companies do not. That can be a drag on an otherwise financially stable cannabis business’s credit score.

Company size: The size of a business in terms of revenue matters significantly to a business’s credit score. Company size is used to determine important information like debt-to-income ratio and cash flow. The latter influences a business’s ability to pay its bills on time and meet its debt service obligations.

Payment history: Meeting all your payments in full and on time keeps your business credit score healthy. Avoiding any collections referrals or liens is critical, as those can remain on your credit history for up to seven years.

Age of credit history: Like a personal credit score, your business’s credit score is influenced by its credit history. A positive track record over a long period influences your credit score for the better. In other words, a business that has been operational for several years is better positioned than a brand-new company.

Credit utilization: Another major factor is how many lines of credit or loans you have on your books. A business with high debt usage is likely to see a negative impact on its credit score. This is especially true if many new lines of credit were opened within the past year.

Tip

If your application for a business loan is turned down because of a poor credit score, find out which areas are hurting you and work on improving them. If it's your credit utilization, reduce your debt outstanding.

How can I get my business credit score?

To obtain your business credit score, you have to request a credit report from the three major credit bureaus by visiting their respective websites. While this report is free for personal credit scores, you will usually pay to get your business credit score.

Credit bureau

Business credit report and score

Starting price for one-time purchase

Dun & Bradstreet

Yes

$61.95

Equifax

Yes

Around $40

Experian

Yes

$49.95

How can I improve my business credit score?

If your business credit score isn’t as good as you were hoping, don’t worry. These are some steps you can take to improve it.

Monitor your business credit score regularly. “Simply keeping an eye on business credit scores is an impactful first step in improving it,” Voiles said. “Many business owners are unaware they exist, unsure of how to access them, or don’t check them regularly or take them into account when managing their business.”

Keep your business and personal finances separate. “Business owners should strive to keep their business finances and personal finances separate,” Bumbales said. “Headaches such as [a high] personal debt-to-income ratio, lack of business credit and more can arise if a business owner does not keep their personal finances and business finances separate.”

Make payments on time. “Beyond careful monitoring, making on-time payments to creditors is one of the best things a business owner can do to improve their business credit score,” Bumbales said.

Reduce your overall debt-to-income ratio. “Improving your business credit score can be done similarly to improving your personal credit score: by being a responsible borrower,” Bumbales said. “Pay your obligations on time and avoid creating too much debt compared to your revenue. If you have had any past strikes on your credit, make sure to resolve them as soon as possible.”

Even with a healthy business credit score, a lender might require a business owner to personally guarantee a loan. According to Ross, this typically includes a personal credit check and is especially common when the business is a sole proprietorship or has only recently launched.

While a business credit score and a personal credit score are distinct, it is best to maintain a good mark for both; they can sometimes complement one another. Business credit reports can be just as important in securing business financing as a strong personal credit score can guarantee. Maintaining good business credit reduces the cost of borrowing money. Also, it avails your business to more favorable payment terms with creditors and vendors alike.

“While one doesn’t necessarily impact the other, with some exception, the benefits of habitual early and on-time payment practices on both fronts will have broad and positively impactful benefits over the course of time — for both the business and the individual,” Ross said.

Bottom Line

Your business credit score directly impacts the cost of borrowing. The stronger your business's financial position, the better you look to lenders and vendors.

Business credit score FAQs

Most financial experts recommend checking your business credit score at least quarterly, with monthly monitoring ideal for businesses seeking financing or experiencing rapid growth. Many credit monitoring services offer real-time alerts for significant changes, making it easier to stay informed without constant manual checks.

Business credit scores don’t look like personal credit scores. As mentioned above, a perfect business score is 100, meaning you usually pay 30 days early. A 90 means you pay 20 days early, and an 80 means you pay right on time. By most standards, 80 and above is the very good range and will get you favorable interest rates. If your score is between 50 and 79, you are in the good or fair range: You pay all of your bills, but some are late. Anything below 50 will set off red flags and impact your ability to borrow money.

Yes, closing a business credit card can impact your score by reducing available credit and potentially shortening your credit history. Consider keeping older accounts open with minimal usage rather than closing them, especially if they don’t carry annual fees.

Several platforms now offer free business credit monitoring. Nav provides free access to your Experian and Dun & Bradstreet summary scores. However, detailed reports typically require paid subscriptions, with annual plans often providing better value than one-time purchases.

Kimberlee Leonard contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.

Donna Fuscaldo, who has 25 years of experience navigating the convergence of business, finance, and technology, is a trusted advisor to small business owners. Her expertise in business borrowing, funding, and investment strategies equips her to provide reliable counsel on everything from business loans to accounting and retirement benefits.

At business.com, Fuscaldo covers business grants and other financing options, business credit cards and retirement funds.

Her analysis has also graced publications like The Wall Street Journal, Dow Jones Newswires, Bankrate, Investopedia, Motley Fool, Fox Business and AARP, solidifying her authority in the field. Beyond her contributions to the financial landscape, Fuscaldo also lends her wisdom on employment matters, with her expertise sought after by platforms like Glassdoor and others.

Armed with a bachelor's degree in communication arts and journalism, Fuscaldo has the unique ability to simplify complex business and career-related topics into actionable insights. This makes her a valuable resource for professionals seeking practical solutions in today's dynamic business environment.

Armed with a bachelor's degree in communication arts and journalism, Fuscaldo has the unique ability to simplify complex business and career-related topics into actionable insights. This makes her a valuable resource for professionals seeking practical solutions in today's dynamic business environment.