Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

6 Benefits of Forming an S Corporation

Setting up your business as an S corp can help you reduce your tax liability and protect your personal assets.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Leaving your nine-to-five to start your own business is a big decision, but it’s only the first step on your journey. Once you become an entrepreneur, you have numerous decisions to make. For example, you must choose a location, implement a hiring process, and settle on traditional and digital marketing strategies.

Selecting a business structure is one such crucial decision you’ll need to make early on. If you’re considering incorporating, you have several options, including to set up as an S corporation. We’ll explain S corporations and their pros and cons to help you decide on the right business structure for your endeavor.

What is an S corporation?

An S corporation, often called an S corp, draws its designation from Subchapter S of the tax code. To start an S corp, a small business owner would file articles of incorporation in the state where it’s headquartered and then file for S corporation status with the IRS. While an S corp shares similarities with a C corporation, distinct income tax regulations and self-employment tax benefits distinguish the two structures.

Forming an S corporation is a strategic business decision that extends beyond simple paperwork. Incorporating protects your personal assets from business liabilities, provides substantial tax advantages and establishes credibility with customers, vendors and financial institutions.

Tip

Before setting up an S corp, you must apply for an employer identification number (EIN). An EIN lets you hire employees, open a business bank account and pay small business taxes.

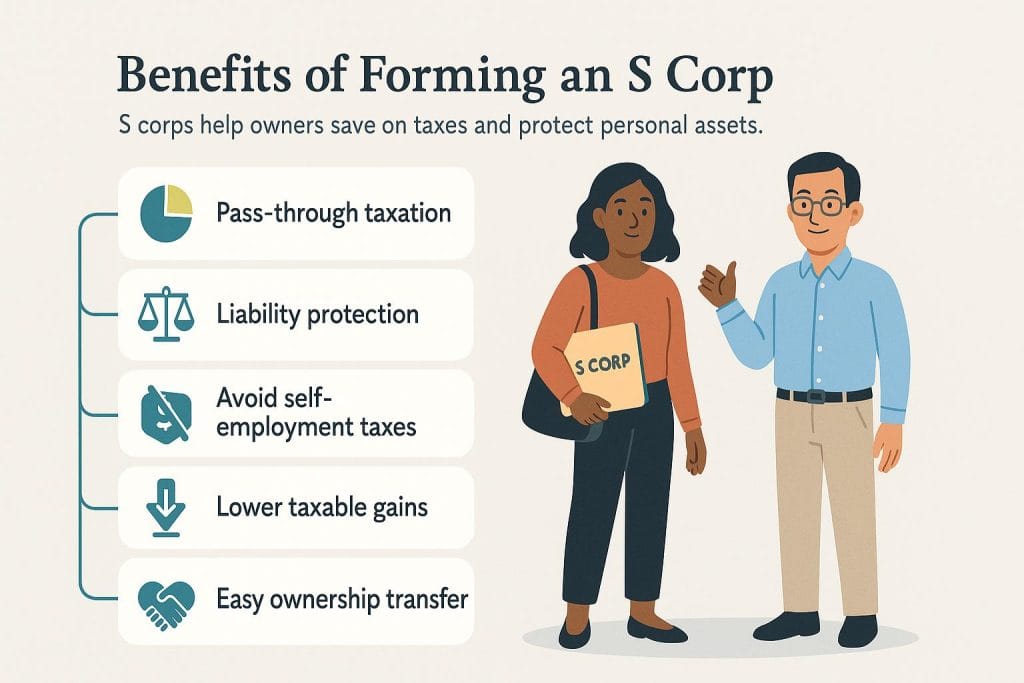

Benefits of forming an S corp

Forming an S corp brings significant benefits to a business owner. Consider the following advantages:

1. An S corp brings pass-through taxation

Like an LLC, an S corp does not pay taxes at the corporate level. Any income or losses are reported only on the business owner’s personal income taxes. As a result, business owners avoid the double taxation that affects C corporations.

Because net losses are “passed through” as well, the individual shareholder may be able to reduce their tax liability by offsetting other income with any S corp losses.

However, there is an important caveat related to compensation management: Any shareholder who works for the company must pay themselves reasonable compensation. This means the shareholder must receive wages comparable to what similar roles pay in your industry and geographic location. According to IRS guidelines, factors including training, experience, duties, time devoted to the business, and comparable salaries determine reasonable compensation. Failing to meet this standard may result in the IRS reclassifying distributions as wages, potentially triggering penalties and back taxes.

2. An S corp offers liability protection

According to the IRS, S corps are “considered by law to be a unique entity, separate and apart from those who own it.” The owners of an S corp have limited liability for the company’s actions. This means owners can’t be held responsible for the company’s actions or debts unless the business owners have signed a personal guarantee.

3. An S corp allows you to avoid self-employment taxes

S corporation shareholders who work in the business are classified as employees for tax purposes, not self-employed individuals. This distinction creates substantial tax savings. While LLC members typically pay the full 15.3 percent self-employment tax on all business income, S corp owner-employees only pay Social Security and Medicare taxes on their W-2 wages. Any remaining profits distributed as dividends avoid self-employment tax entirely, potentially saving thousands of dollars annually for profitable businesses.

4. An S corp reduces your taxable gains

If you plan to sell your business in the future, an S corp is attractive for yet another reason: When you sell the company, your capital gains tax treatment can be more favorable than with a C corporation sale. S corp stock sales typically qualify for long-term capital gains treatment after holding the stock for more than one year, with federal rates ranging from 0 to 20 percent depending on income levels, plus a potential 3.8 percent net investment income tax for high earners.

5. An S corp has a life of its own

An S corp is an excellent option if you plan to build a lasting business rather than a side hustle that you plan to sell in a few years. Unlike an LLC, an S corp has an unlimited life span.

Your business maintains perpetual existence, continuing operations regardless of changes in ownership, management or shareholders. This permanence provides stability for long-term contracts, lending relationships and business partnerships. The company persists even if founding shareholders retire, sell their shares or pass away, ensuring business continuity for employees, customers and stakeholders.

6. It’s easy to change S corp ownership

With an S corp, ownership is easily transferred through the sale of the company stock. Additionally, if you determine that S corp status no longer suits your business needs — perhaps due to growth requiring more than 100 shareholders or international investors — you can revoke the election by filing a statement with the IRS, signed by shareholders holding more than 50 percent of the stock.

Tip

When selling company stock, you will need to structure a stock purchase agreement that formally transfers ownership of your company's stocks between two parties.

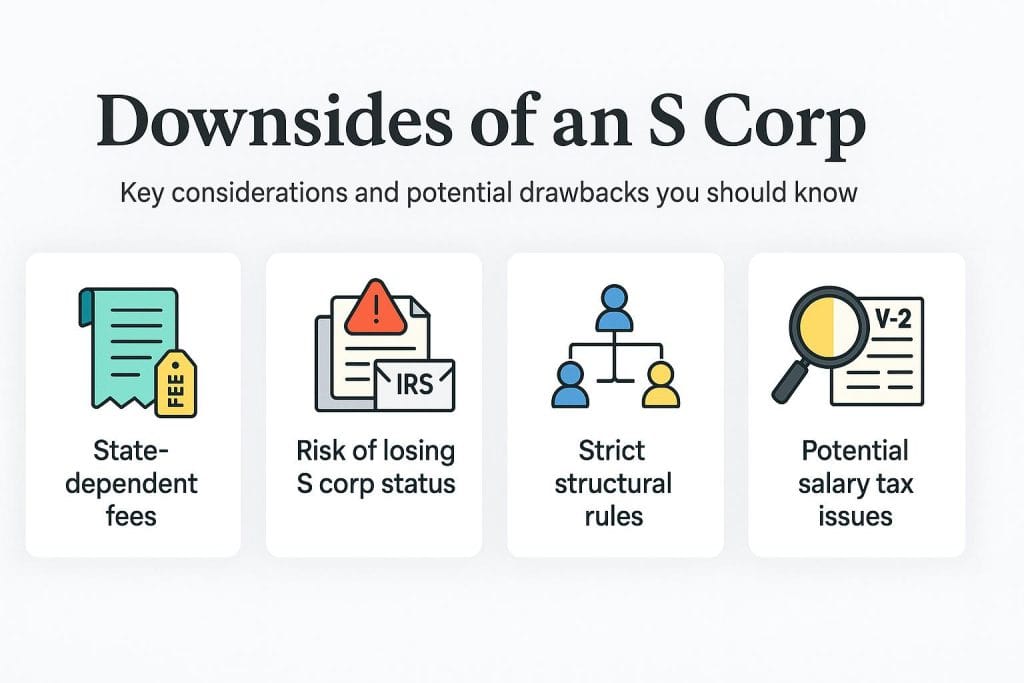

Downsides of an S corp

There are many benefits of setting up an S corp, but you should be aware of these disadvantages:

S corps may incur fees. State filing fees for S corporations vary significantly, with annual report fees ranging from $0 in states like Ohio to $800 in California as of 2024. Additional costs include registered agent fees (typically $100 to $300 annually), franchise taxes in certain states and professional tax preparation fees that often exceed those for simpler business structures.

S corps have the potential for costly mistakes. If you make any mistakes regarding stock ownership, consent or notification to the IRS, it could cost you your S corp status.

S corps have strict requirements. Compared with other types of incorporation, an S corp has a strict management structure. You must appoint a board of directors and officers and hold annual shareholder meetings.

S corps have potential tax liabilities. The IRS scrutinizes S corporation compensation closely, particularly for shareholder-employees. Setting your salary below market rates to minimize payroll taxes raises audit risks. The IRS can reclassify distributions as wages retroactively, resulting in employment tax liabilities, penalties and interest charges that can date back three years or more.

Tip

If you think an S corp may be the right legal structure for your business, consult a business attorney who can inform you of your options and recommend the appropriate next steps based on your situation.

Other business structures to consider

If you’re on the fence about setting up an S corp, there are other options to consider.

“Business owners should think about entity structure because it’s really key,” said Candice Caruso, SVP, Chief Business Banking Officer at WSFS Bank. “An entity structure that may have served you well at the beginning of your business may not be the right structure as you continue to grow and evolve. It’s important to reassess that over time and see what advantages [other structures] may provide you.”

Here’s a breakdown of different types of business structures:

Business structure

Ownership

Owner’s liability

Tax

S corporation

1+ people

Not held personally liable

Corporate tax

C corporation

1+ people

Not held personally liable

Corporate tax

LLC

1+ people

Not held personally liable

Self-employment tax

Partnership

2+ people

Held personally liable unless structured as a limited partnership

Self-employment tax

Sole proprietor

1 person

Held personally liable

Self-employment tax

Here’s more information about these business structures:

C corporation: A C corp operates as a separate tax entity from its owners, filing its own tax return and paying corporate income tax at a flat 21 percent federal rate as of 2024. Unlike S corps, C corporations can have unlimited shareholders from any country, multiple classes of stock, and institutional investors. However, C corp shareholders face double taxation when receiving dividends — the corporation pays tax on profits first, then shareholders pay personal income tax on distributed dividends.

LLC: A limited liability company is a business entity that separates the business’s assets and the owner’s personal assets. To set up an LLC, you must file articles of incorporation with the state. However, an LLC is less expensive and less tedious to manage than an S corp.

Partnership: In a partnership, the members can structure the business as they see fit. All partners will have an equal share in the company and its profits and losses. You should form a partnership only with someone you trust.

Sole proprietorship: In a sole proprietorship, the business and the individual are the same; there is no legal separation. Sometimes, people who freelance or have a side gig operate as sole proprietors because they don’t have to do anything to establish one. However, you can be held personally liable for any lawsuits or debts incurred by the business.

Tip

If you plan to dissolve a partnership, both you and your former business partner can be sued during and after the dissolution process.

S corporation FAQs

An S corp gets its name because it is taxed under Subchapter S of the Internal Revenue Code, making it a "pass-through" business. This means the company's income isn't taxed at the corporate level but "passes through" to the shareholders.

According to the IRS, businesses must meet the following requirements to qualify for S corp status:

Be a domestic corporation

Only have allowable shareholders

Have a maximum of 100 shareholders

Offer only one class of stock

Can't be an ineligible corporation, like certain financial institutions or insurance companies

To form an S corporation, begin by incorporating your business in your state by filing articles of incorporation with the secretary of state and paying the required filing fees. Next, obtain an EIN from the IRS if you haven't already. Within 75 days of incorporating (or by March 15 if electing for the current tax year), file Form 2553, Election by a Small Business Corporation, signed by all shareholders. The IRS typically responds within 60 days with an acceptance or rejection letter. If approved, your S corp election becomes effective on the date specified in your filing, usually the beginning of the current tax year if filed timely.

An S corp typically makes sense when your business generates sufficient profit to pay yourself a reasonable salary plus additional distributions. A common rule of thumb suggests considering S corp status when your net business income exceeds $60,000 annually, as the self-employment tax savings often outweigh the additional compliance costs at this threshold. C corps suit businesses planning to raise venture capital, go public, or expand beyond 100 shareholders. LLCs work well for businesses holding appreciating assets like real estate, or those preferring simpler administration without the formal requirements of corporate governance.

Yes, you can switch from an S corp to a C corp through voluntary revocation or automatic termination. For voluntary revocation, file a statement with the IRS signed by shareholders owning more than 50 percent of the stock, specifying the revocation date. The change typically takes effect the following tax year unless you specify a prospective date. Be aware that once you revoke S corp status, you generally must wait five years before re-electing it, unless the IRS grants special permission. Automatic termination occurs if you violate S corp requirements, such as exceeding 100 shareholders or issuing a second class of stock.

Jamie Johnson has spent more than five years providing invaluable financial guidance to business owners, leading them through the financial intricacies of entrepreneurship. From offering investment lessons to recommending funding options, business loans and insurance, Johnson distills complex financial matters into easily understandable and actionable advice, empowering entrepreneurs to make informed decisions for their companies. As a business owner herself, she continually tests and refines her business strategies and services.

At business.com, Johnson covers accounting practices, budgeting, loan forgiveness and more.

Johnson's expertise is also evident in her contributions to various finance publications, including Rocket Mortgage, InvestorPlace, Insurify and Credit Karma. Moreover, she has showcased her command of other B2B topics, ranging from sales and payroll to marketing and social media, with insights featured in esteemed outlets such as the U.S. Chamber of Commerce, CNN, USA Today, U.S. News & World Report and Business Insider.