As a business owner, part of the job is managing risk, including following best practices, complying with applicable laws and carrying the right business insurance. If you have employees, that includes workers’ compensation (also called workman’s comp or workers’ comp) coverage.

But figuring out how much coverage to carry isn’t always straightforward. Carrying more insurance than you need can tie up capital, while not having enough leaves your company dealing with expensive claims and potential legal headaches if something goes wrong. Here’s a closer look at the factors that influence your coverage needs and how to choose a policy that makes sense for your business.

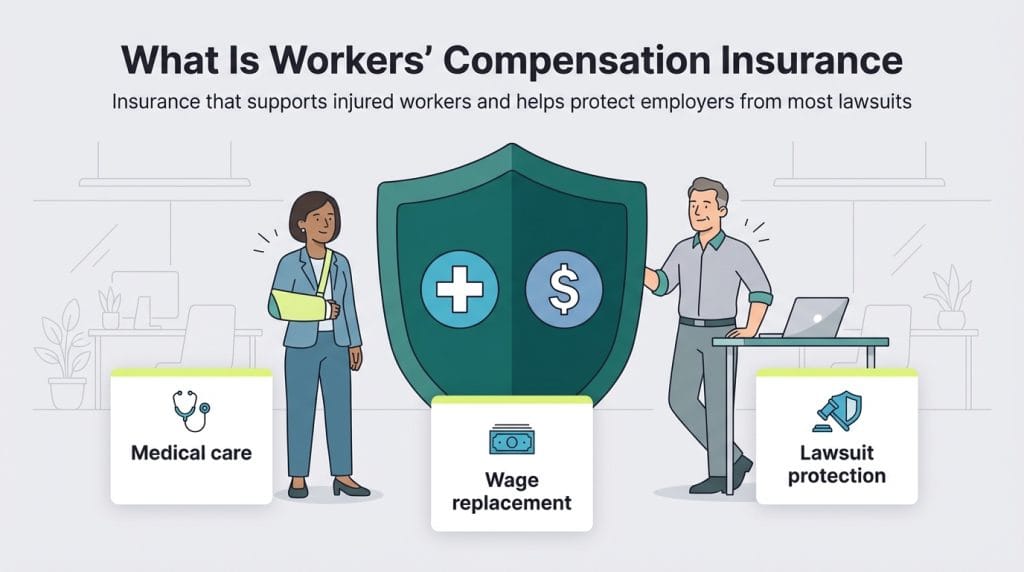

What is workers’ compensation insurance?

Workers’ compensation insurance is coverage that provides benefits and protection for employees who are injured in a workplace accident or become ill on the job. It helps ensure workers receive medical care and wage replacement and, in most cases, protects employers from direct legal action after a work-related injury or illness. Workers’ comp works much like other types of business insurance: Employers pay into a policy or state-managed system, and benefits are paid out if a covered incident occurs.

“When employees are injured on the job, workers’ compensation provides financial coverage for their medical bills, lost wages and other expenses,” said Jeff Somers, a startup founder and product leader with experience building and scaling early-stage companies. “In addition to protecting employees, workers’ compensation limits employers’ exposure to lawsuits after work-related injuries.”

How to determine how much workers’ compensation insurance you need

Figuring out how much workers’ compensation coverage you need isn’t a one-size-fits-all process. The right amount depends on several factors, including state requirements, payroll size and the level of risk tied to your industry. While insurance brokers or agents can help guide the process, understanding what affects your rate makes it easier to spot gaps or unnecessary costs.

To estimate your total workers’ compensation insurance cost, start by asking the following questions.

What does your state require for workers’ comp insurance?

Workers’ compensation requirements are set at the state level. Texas is the most notable outlier and allows most private employers to opt out of workers’ compensation coverage, though “nonsubscribers” there face different liability risks. In many other states, coverage is required as soon as you hire your first worker, whether they are full-time or part-time employees.

“Since workers’ compensation laws are regulated at the state level, business owners should first determine when workers’ compensation insurance is required for their business,” Somers advised. “Usually, it’s as soon as they hire an employee.”

Some states allow workers’ comp exemptions if you are the sole employee of your business. Somers suggests weighing the potential cost of a workplace injury against the price of coverage before relying on that exemption.

“Since most health insurance plans exclude coverage for work-related injuries, sole proprietors may be putting their livelihood on the line if they opt to skip workers’ comp coverage for themselves,” Somers cautioned.

What is the average age of your workforce?

The average age of your workforce can influence workers’ compensation risk because injury patterns, experience levels and recovery timelines tend to shift as teams skew younger or older. Insurers don’t price policies strictly by age, but changes in workforce demographics can affect the types of claims a business may see over time.

Quinten Lovejoy, founder of The 300 Group, noted that both younger and older teams bring different risks. “As employees age, the propensity for injury increases,” Lovejoy said. “At the same time, a younger workforce brings about less experience and an increased chance of on-the-job injury.”

An aging workforce is becoming more common across many industries. Bureau of Labor Statistics projections show participation among older workers is expected to continue rising through the early 2030s, changing the risk profiles employers need to consider.

Recovery timelines after a workplace injury can vary widely depending on the role, severity of the incident and the employee's overall health. Because longer claims can drive higher costs, many business owners review coverage limits, safety training and return-to-work policies as part of their workers' comp strategy.

What risks do your workers face?

The level of risk tied to your employees’ daily work plays a major role in how much workers’ compensation coverage is needed. Insurers look closely at job duties because higher-hazard roles tend to produce more frequent or more severe claims.

“With higher levels of risk comes the need for high levels of coverage,” Lovejoy said. “A roofing contractor obviously has a higher risk than someone working in a jewelry store.”

Occupational hazards are often the biggest driver of cost differences because insurers assign classification codes — standardized job categories developed by the National Council on Compensation Insurance (NCCI)— to estimate injury risk. Each code carries a base rate per $100 of payroll that can vary widely by industry. For example, clerical office roles may fall below about $0.20 per $100 of payroll in some markets, while higher-risk work such as framing or roofing can reach $8 to $14 or more per $100 of payroll, depending on the state and carrier.

Following strong safety practices can help reduce claims over time. Maintaining OSHA compliance (standards set by the Occupational Safety and Health Administration) may also help lower risk, although higher-hazard industries will typically have to pay higher premiums regardless of prevention efforts. According to OSHA, falls remain the leading cause of death in construction, followed by struck-by incidents, electrocutions and caught-in/between hazards — collectively known as the “Fatal Four.”

What are the financial risks?

Understanding the financial exposure your business faces can help you decide how much workers’ compensation coverage makes sense. Medical costs, wage replacement rules and state benefit requirements vary widely, which means the real cost of a claim and its impact on your premiums can look very different depending on where you operate.

When reviewing your coverage, consider the types of financial risk your business could face, such as:

- Higher medical costs or wages that can raise the total cost of a claim

- State benefit rules that determine how long payments continue

- Overtime costs or slower productivity while employees recover

- Higher premiums after claims or in higher-risk roles

Additionally, you’ll face even more financial risks if you don’t carry required workers’ comp coverage. Penalties vary by state, but employers may face fines, stop-work orders or retroactive premium charges if an audit finds coverage should have been in place.

How many people does your business employ?

The size of your workforce can influence workers’ compensation costs, but not always in the way business owners expect. Premiums aren’t based on headcount alone. Payroll totals and the type of work employees actually do tend to matter more. As teams grow, though, there’s simply more opportunity for injuries to happen, and that can influence claims patterns over time.

In practical terms, adding employees often means higher total payroll and a broader mix of job duties, two factors that insurers use when calculating workers’ comp premiums.

Hiring more employees often changes how workers' comp premiums are calculated. Reviewing options from the

best business insurance providers can help you understand how growth may affect your coverage needs.

How much does workers’ compensation insurance cost?

Workers’ compensation pricing can look confusing at first because there isn’t a single national rate. Costs vary widely depending on where your business operates, the type of work employees perform and how insurers evaluate risk. Instead of focusing on one average price, it helps to understand the factors that shape premiums and why quotes can differ so much from one company to another.

- Location and state rules: Geography plays a major role in workers’ comp pricing. The Oregon Workers’ Compensation Premium Rate Ranking study — often used as a national comparison benchmark — found that the premium index ranged from about $0.50 per $100 of payroll in North Dakota to roughly $2.52 in Hawaii, with a national median of $1.09. These figures compare relative cost levels between states rather than the exact premiums employers pay, which is why getting a localized quote remains essential.

- Business size, payroll and job risk: Real-world premiums depend heavily on payroll totals and the duties employees perform. Marketplace data from Insureon suggests many small employers pay around $54 per month on average for workers’ comp coverage, though actual costs can fall well below or far above that number depending on industry risk and workforce size.

- Claims history and your experience modification rate (EMR): Insurers also look at past claims and workplace safety trends when pricing coverage. In many states, experience mods are calculated using data from the NCCI or a state-specific rating bureau. “The NCCI is the authority that looks at a company’s claims history and makes a projection of its risks based on the business itself and national trends of that industry,” Lovejoy said.

- Carrier appetite and policy differences: Even businesses with similar risk profiles may receive different quotes depending on the insurer. John Espenschied, agency principal and owner at Insurance Brokers Group, recommended getting multiple quotes when evaluating workers’ comp coverage. “Each insurance carrier will have different risk appetites for business,” he said. “Some companies will consider high-risk companies like roofers, while other companies will never offer workers’ compensation for a roofing business. This means the rates can fluctuate between one carrier and another.”

The NCCI does not operate in every state. Some jurisdictions use independent rating bureaus that perform similar functions when calculating experience modification rates and classification rules.

How are workers’ compensation premiums calculated?

Insurers typically look at a few core factors when calculating workers’ compensation premiums: payroll totals, job classification rates and a company’s experience modification rate (EMR). The exact formula can vary by state and carrier, but these elements form the foundation of most pricing models.

- Payroll: Workers’ comp premiums are generally tied to payroll, with insurers looking at costs per $100 of wages. The actual rate can shift quite a bit depending on the state and the type of work employees perform. Many carriers rely on data from the NCCI, while others follow state-run rating systems. Even so, a higher-risk business in a lower-cost state may still pay more than a lower-risk company operating in a higher-cost market.

- Job classification rate: Classification codes are basically how insurers group jobs by risk level. Desk-based roles usually fall into lower-risk categories, while more physical trades — like roofing or construction — tend to carry higher base workers’ comp rates. You may also hear these referred to simply as class codes, and they play a big role in how premiums are calculated.

- Experience modification rate (EMR): An EMR reflects a company’s past workers’ comp claims compared with similar businesses in its industry. A lower EMR can help reduce premiums, while a higher one may increase costs because it signals greater historical risk.

While pricing models differ slightly between insurers, premiums are often illustrated using a simplified formula:

Classification rate × EMR × (Payroll ÷ 100) = Estimated premium

How to save on workers’ compensation insurance costs

Workers’ comp premiums aren’t entirely within a business owner’s control. The type of work your team performs and your claims history both play a role in pricing, and those factors can feel frustrating when you’re trying to manage costs. Still, many companies find there are practical ways to reduce risk over time and keep premiums from climbing faster than expected. Consider the following:

- Build safety training into everyday operations: A clear safety program can help employees recognize risks early, whether they work in a warehouse or a small office. Over time, fewer incidents can lead to a more stable EMR and smoother renewal pricing.

- Pair training with the right equipment: Safety policies tend to work best when they’re backed by proper gear. If employees handle hazardous materials or work in physically demanding environments, providing gloves, eye protection or respirators can help limit injuries that lead to claims.

- Address hazards before they turn into claims: A quick walkthrough of your workspace can often reveal small issues that become expensive later, such as frayed wiring, poorly positioned desks or missing machine guards. Fixing these problems early is usually far less costly than dealing with a workplace injury after the fact.

- Consider annual billing if cash flow allows: Some insurers offer a lower overall price when premiums are paid annually rather than monthly. The discount won’t make sense for every business, but for companies planning to keep coverage long term, paying upfront can sometimes reduce administrative fees and overall costs.

A

workers' comp settlement is an agreement that resolves some or all of an employee’s injury claim, often through a lump-sum payment or structured benefits. Depending on state rules, a settlement may close future wage claims while leaving medical coverage open.

Best workers’ compensation insurance practices

Managing workers’ compensation coverage isn’t just about choosing the right policy; it also comes down to how consistently a business reviews risks, communicates with employees and responds when incidents occur. The practices below can help companies stay organized, support injured workers and avoid unnecessary premium increases over time.

- Review policies before renewal: Many businesses take another look at their workers’ comp policies each year, usually a few months ahead of renewal. Changes in staffing, job duties or services can shift classification codes and pricing, so a quick review early on can help catch costly misclassifications.

- Stay current on premiums: Keeping premiums paid and up to date helps avoid coverage lapses that could leave both the business and its employees exposed after an accident.

- Keep communication clear and consistent: Employees should understand what workers’ comp covers, how to report an injury and what support the company provides during recovery. Clear communication tends to reduce confusion and helps incidents move through the claims process more smoothly.

- Support injured employees in getting care: When injuries happen, helping employees access appropriate medical care quickly can make a difference. In serious situations, that may mean helping an employee get emergency care right away. For less urgent injuries, it often comes down to following state guidelines and the company’s policy when arranging evaluations.

- Document incidents promptly: Starting an internal review soon after an accident helps capture accurate details while events are still fresh. Documenting who was involved, what happened and where it occurred can support smoother claims handling and help identify ways to prevent similar injuries.

- Take steps to prevent repeat incidents: Once the cause of an injury is identified, many businesses look for practical ways to reduce future risk, from improving housekeeping and signage to installing safety equipment or adjusting workflows. “Installing appropriate safety equipment not only lets you comply with OSHA and other regulations, but it is also an investment in your employees, uninterrupted operations and corporate risk reduction,” said Anthony Dublino, regional area manager for SafeRack.

- Report injuries early: Prompt reporting and claim submission can help move the workers’ comp claim process forward faster and reduce uncertainty for employees. Early action also shows workers that their well-being is taken seriously, which can encourage cooperation throughout recovery.

- Create return-to-work programs: Lovejoy recommended establishing structured return-to-work plans for employees recovering from injuries. “Companies should have a formal ‘return to light duty’ program,” he said. “If employees are not fit to return to their normal job duties, they can still return to work and perform modified duties and, as such, reduce the overall claim amount.” These programs can help employees stay connected to the workplace while helping businesses manage claim costs.

Kimberlee Leonard and Jennifer Dublino contributed to this article. Source interviews were conducted for a previous version of this article.