Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

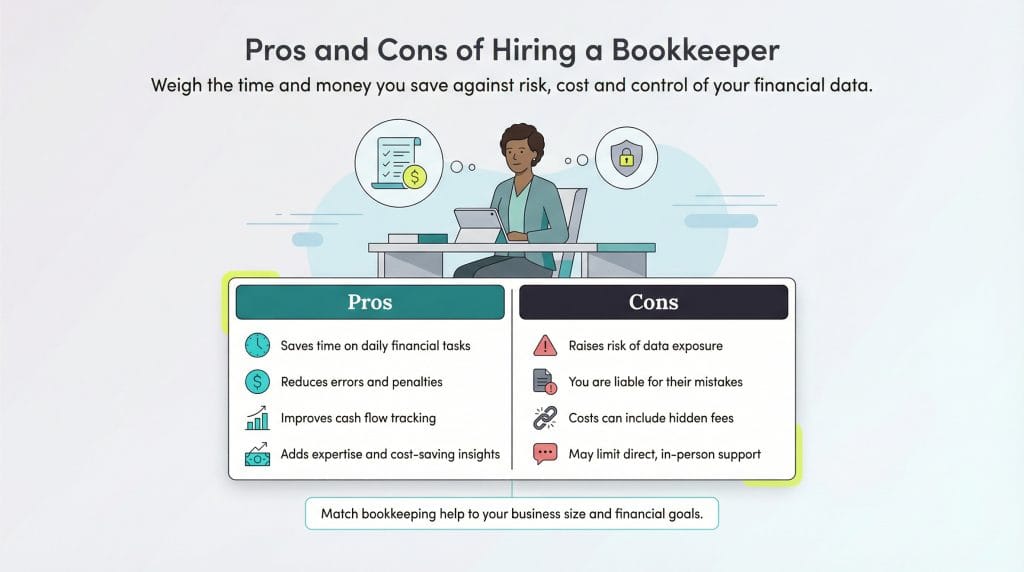

A bookkeeper can help you save money and time. Learn how hiring this financial professional may affect your business.

Small business owners are often used to handling many tasks. They may contact suppliers, manage marketing, monitor sales and respond to customer inquiries and complaints. They may even take on accounting and bookkeeping tasks. However, performing financial duties yourself may do more harm than good. Hiring a bookkeeper might be the wiser choice.

Bookkeepers help a business owner manage day-to-day finances. These experts monitor cash flow from different accounts, oversee bills and invoices and organize your books to improve money management. We’ll share the pros and cons of hiring a bookkeeper and explain how these financial professionals operate.

A bookkeeper is a financial professional who handles administrative tasks related to recording transactions, managing accounts and preparing financial reports.

Bookkeepers are responsible for maintaining accurate financial records, following up on past-due payments, sending billing reminders, processing payments for suppliers and running payroll. They’re a more appropriate choice than accountants for basic financial tasks because their hourly rates are generally less expensive. [Related Article: Importance of a Strong Finance Team for Accounting and Seeking Capital]

However, according to Charlie McClain, principal at GrowthPoint Bookkeeping, bookkeepers’ responsibilities go beyond basic financial tasks.

“Beyond data entry, a skilled bookkeeper provides foundational insights into your business’s financial health, offering clarity that can inform more strategic decision-making,” McClain explained.

Mark Wilkinson, co-founder and chief financial officer (CFO) at TileCloud, emphasized that bookkeepers play a crucial role in maintaining financial accuracy. “Bookkeepers often act as an early warning system, able to spot discrepancies or errors before they become bigger issues,” Wilkinson noted. “In small businesses especially, they often take on additional tasks like helping with budgeting or tracking cash flow, which can be a lifesaver for [business] owners trying to juggle everything.”

While bookkeepers can be a valuable asset to your business, allowing someone else to manage your finances does pose some risks. Here are the advantages and potential drawbacks of hiring a bookkeeper.

Before hiring a bookkeeper, it’s important to understand which type best suits your business needs. Consider the following options.

Hiring an in-house bookkeeper is ideal if you have a medium-sized business and want to keep track of the bookkeeper’s day-to-day duties. However, this type of bookkeeper requires a steep financial investment. If you hire an in-house bookkeeper, you must pay for all the resources they need, including their salary and employee benefits.

If you only need a bookkeeper to reconcile your accounts periodically, consider hiring a freelancer. These independent professionals typically charge an hourly rate based on their expertise and experience.

With the rise of cloud-based accounting software and remote work, businesses can easily hire a virtual bookkeeper. Better yet, some of the best accounting software services include access to live virtual bookkeepers through their platforms (or offer this feature as a paid add-on).

“These bookkeepers work remotely using online and virtual software to manage your financial records,” Wilkinson explained. “They’re perfect for small businesses that want easy access to their numbers on the go and prefer a flexible, virtual collaboration model.”

Large enterprises often use bookkeeping agencies to manage their finances, but small and midsize businesses can also benefit from this approach. The cost of using an agency varies based on the type and level of service required.

Every sector has unique financial considerations that businesses operating within it must account for when doing bookkeeping. McClain noted that niche-specific bookkeepers incorporate these specialized needs into their work.

“Niche-specific bookkeepers focus on a particular industry or business model, such as real estate agencies, medical practices or e-commerce stores,” McClain said. “Their specialized expertise with industry regulations, unique expenses and revenue patterns allows them to offer more targeted advice, create more accurate financial reports and improve overall operational efficiency.”

When you outsource your bookkeeping duties to a third party, that company sets up and trains a dedicated team to manage your financial tasks. The outsourcing partner typically provides the necessary infrastructure, including computers with accounting software, voice-over-internet protocol systems for billing reminders, office space and other essential resources.

Here are some factors to consider when choosing a bookkeeper:

Hiring a bookkeeper can cost anywhere from a few hundred dollars per month to lower double-digit hourly rates. McClain noted that costs vary based on expertise and certification level.

“In practice, a small business might pay $30 to $60 per hour for a qualified bookkeeper with QuickBooks certification,” McClain explained. “More advanced bookkeeping or advisory services may range from $75 to $100 per hour. CPA [certified public accountant]-level support often starts around $125 to $200 per hour.”

While many of the best accounting software solutions can handle bookkeeping functions, some bookkeepers may prefer dedicated bookkeeping tools. Here are some popular bookkeeping and accounting options to consider for your finance team.

FreshBooks is a popular accounting solution with many bookkeeping tools for small businesses. It can generate invoices, handle expense management and create financial reports. The software has an easy-to-use interface and integrates with PayPal, Google Workspace, Stripe and other platforms. It also has a mobile app that lets you update and track your books on the go. Read our detailed FreshBooks review to learn more about features and pricing.

You can organize your books and collaborations with Zoho Books on one platform. The software allows you to add your bookkeepers and accountants and monitor them through the platform. In addition to invoicing and billing reminders, Zoho Books can sync with bank accounts to track expenses and payments. It also allows you to keep an inventory of your office supplies or product stock to know when and how to replenish them easily. You can also request reports, such as profit and loss statements and tax summaries. Our in-depth Zoho Books review has more details about features and functions.

Xero is cloud-based accounting software that lets you handle all accounting and bookkeeping tasks on one platform. You can check product inventory, save contacts and evaluate business performance through generated reports. It also has a sales tax feature that helps you file your taxes and prepare sales tax returns with automatic calculations. Read our review of Xero for more information on features and pricing.

Kashoo is considered a top QuickBooks alternative; it has essential accounting and bookkeeping services suitable for very small businesses. It helps you track expenses and bills, create invoices and generate basic reports, such as income statements and balance sheets. The platform is easy to use but doesn’t offer full bookkeeping features like product inventory and pre-invoice documents. You can access your account through a mobile app for on-the-go tracking.

The potential disadvantages of hiring a bookkeeper are the same as the possible drawbacks when hiring any team member, whether in-house or outsourced. The question isn’t whether or not to hire a bookkeeper but how to find one with maximum skill at the lowest cost and risk. Spending a little more to get organized, avoid costly penalties and improve your financial future is well worth the money.

Derek Gallimore and Jennifer Dublino contributed to this article.