Many small business owners purchase insurance when they launch their business and then treat it as a fixed expense that runs quietly in the background. The policy renews each year automatically, the premium is paid and the coverage details don’t get a second look until something goes wrong or a new policy is needed. Perhaps a claim is filed, a landlord requests an updated certificate or a new client contract demands coverage the business doesn’t have.

The problem with this approach is that businesses change. Revenue grows. Employees are hired. New locations open. Equipment is purchased. Service offerings expand. Contracts impose new requirements. The insurance program that was perfectly adequate two or three years ago may have significant gaps today, and those gaps remain invisible until a loss occurs that exceeds or falls outside your coverage.

An annual insurance review is the most reliable way to catch these gaps before they cost you money. This guide provides a structured, repeatable framework for conducting that review — from gathering your current policies to implementing changes and preparing for next year.

How to review your business insurance

To review your business insurance annually, follow these steps.

Step 1: Gather your current policies and documentation.

Begin by assembling every active insurance policy your business carries. This includes your business owner’s policy or standalone general liability, commercial property, workers’ compensation, commercial auto, professional liability, cyber liability, umbrella or excess liability, employment practices liability and any other specialty coverages. If you’re unsure whether you’ve captured everything, your insurance agent can provide a summary of all policies they manage on your behalf.

For each policy, document the coverage type, insurance carrier, policy number, coverage limits (per-occurrence and aggregate), deductibles, annual premium and renewal date. Having this information organized in a single summary document makes the rest of the review process significantly more efficient.

Also gather any certificates of insurance (COIs) you’ve issued to landlords, clients, lenders or other third parties over the past year. These certificates represent coverage commitments you’ve made, and they need to remain accurate and up to date. If you’ve changed carriers, adjusted limits or modified coverages, any outstanding certificates may need to be reissued.

Step 2: Assess what’s changed in your business.

This is the most important step in the entire review process. Your insurance program was built around a snapshot of your business at a specific point in time. This step determines whether that snapshot still matches reality.

Walk through each major dimension of your business and note any changes since your last review.

- Revenue: Has your annual revenue increased or decreased significantly? Revenue is often a key rating factor for general liability insurance, particularly for customer-facing businesses. Significant revenue changes may warrant a review of your coverage limits and classifications. While there’s no universal threshold, many advisors recommend reassessing your policy when your revenue changes materially year over year. Growth in revenue means growth in exposure — more customer interactions, more transactions and more opportunities for a claim.

- Employees: Have you hired new staff, added contractors or changed your workforce composition? Employee headcount directly affects workers’ compensation premiums and may trigger new insurance obligations. Adding employees in a new state may require additional workers’ comp coverage for that state. If your team has grown meaningfully, employment practices liability insurance (EPLI) becomes a more pressing consideration.

- Physical space: Have you moved, expanded, opened a new location, downsized or started working from home? Changes to your physical footprint affect commercial property coverage, business interruption limits and the insurance requirements in your lease. A new location needs to be added to your policy. A vacated location should be removed to avoid paying for unnecessary coverage.

- Equipment and property: Have you purchased significant new equipment, expanded your inventory, invested in technology upgrades, or completed renovations or buildouts? Your commercial property coverage needs to reflect the current replacement value of everything it covers. Business owners frequently accumulate property value over time without updating their policy, creating a growing gap between actual values and insured values.

- Products and services: Have you launched new product lines, added service offerings or entered new markets? New offerings can introduce liability exposures that your existing policies don’t cover. Adding a consulting practice to a product business may require professional liability coverage for the first time. Launching an e-commerce channel may warrant cyber liability coverage.

- Contracts and relationships: Have new clients, landlords or lenders imposed insurance requirements during the past year? Review any contracts signed since your last review for insurance provisions you need to meet. Pay particular attention to minimum coverage limits, additional insured requirements and any coverage types new to your program.

- Vehicles: Have you added or removed business vehicles? Do employees now use personal vehicles for business purposes who didn’t before? Changes here affect your commercial auto and hired and non-owned auto coverage.

- Digital operations: Have you started collecting more customer data, launched an online store, adopted new technology platforms or moved to cloud-based systems? Expansion of your digital footprint increases your cyber liability exposure and may warrant new or increased cyber coverage.

>> Learn how cyber insurance can help your business.

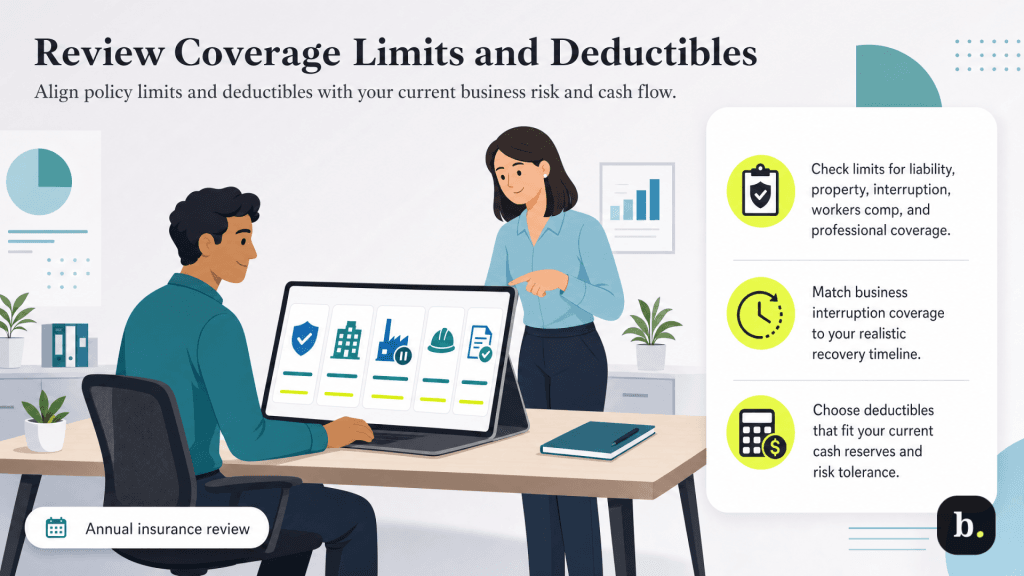

Step 3: Review your coverage limits and deductibles.

With a clear picture of how your business has changed, evaluate whether your current coverage limits are still adequate for each policy.

- General liability: Are your per-occurrence and aggregate limits sufficient for your current revenue level and client requirements? If your revenue has grown significantly or you’ve signed contracts with higher limit requirements, your current limits may need to increase. If you’re approaching or exceeding the threshold where an umbrella policy becomes cost-effective, discuss that option with your agent.

- Commercial property: Does your coverage reflect the current replacement cost of all insured property? This is not the original purchase price or the depreciated value — it’s what it would cost to replace everything at today’s prices. Undervaluing your property on the policy is particularly risky because many commercial property policies include a coinsurance clause that penalizes you if your insured value is below a specified percentage of actual replacement cost. The penalty reduces your payout even on partial losses, compounding the impact of being underinsured.

- Business interruption: Is the coverage amount and duration sufficient to sustain your business through a realistic worst-case scenario? Calculate your current monthly fixed expenses — rent, payroll, loan payments, utilities, insurance premiums — and multiply by the number of months it would realistically take to resume operations after a catastrophic property loss. If that number exceeds your business interruption limit, you need more coverage.

- Workers’ compensation: Is your employee classification and payroll reporting accurate and current? Workers’ comp premiums are based on classification codes and payroll, and your policy is audited at the end of the term. Inaccurate reporting during the policy period — underreporting payroll, misclassifying employees into lower-risk categories, etc. — results in audit adjustments and back-premiums that can be significant.

- Professional liability: If you’ve expanded your service offerings or taken on larger, more complex engagements, your errors and omissions limits and coverage scope may need updating. The financial exposure from a professional error on a large project is different from the exposure on a small one, and your limits should reflect the scale of work you’re currently performing.

Additionally, evaluate whether your current deductibles still make sense given your financial position. A higher deductible reduces your premium but increases your out-of-pocket exposure when a claim occurs. If your business has grown and your cash reserves are stronger, you may be comfortable with a higher deductible in exchange for premium savings. Conversely, if cash flow is tight, a lower deductible provides more predictable costs when a loss occurs.

You may be able to

deduct business insurance, such as general liability premiums, on your tax returns. Be sure to review your options with your CPA annually.

Step 4: Identify gaps and unnecessary coverage.

Based on your assessment of business changes and your coverage limit review, identify risks that are currently uninsured or underinsured and coverages you may no longer need.

Common gaps that surface during annual reviews include:

- Cyber liability coverage that was never purchased, despite the business handling increasing volumes of customer data

- Professional liability limits that haven’t kept pace with the scope and scale of services offered

- Hired and non-owned auto coverage that’s missing, even though employees regularly drive personal vehicles for work

- Business interruption limits that are based on revenue from several years ago and no longer reflect current operating expenses

- Employment practices liability that was never added despite a growing headcount

- Umbrella coverage that would provide critical additional protection at a relatively modest cost

On the other side, look for coverage you’re paying for that no longer applies:

- Commercial property for a location you’ve vacated

- Equipment coverage for assets you’ve sold or decommissioned

- Higher-tier plans for risks that have diminished

Eliminating unnecessary coverage isn’t just about saving money — it frees up budget that you can redirect toward closing genuine gaps.

Step 5: Shop for competitive rates.

Your annual review is the natural time to ensure you’re getting competitive pricing for your coverage. This doesn’t necessarily mean finding the cheapest premium — it means finding the best value for the protection you need.

Request renewal quotes from your current carrier and comparison quotes from at least two or three additional carriers. If you work with an independent insurance agent or broker, they can access multiple carriers on your behalf, which is significantly more efficient than contacting carriers individually. Independent agents are particularly valuable here because they’re not limited to a single insurer’s products.

When comparing quotes, resist the temptation to focus only on premiums. Compare the full picture: coverage types, limits, deductibles, exclusions, endorsements, and the carrier’s financial strength and claims reputation. A lower premium with lower limits, broader exclusions or a higher deductible may actually provide worse value than a slightly more expensive policy with stronger coverage. Check the carrier’s AM Best rating to assess financial stability — an insurer that can’t pay claims is worthless regardless of how low the premium is.

Ask about available discounts. Many carriers offer multi-policy discounts for bundling coverages, claims-free discounts for businesses with clean loss histories, industry association discounts and payment discounts for annual rather than monthly premium payments. Your agent can identify which discounts you qualify for and ensure they’re applied.

One important consideration: Switching carriers purely for a lower premium isn’t always the right move. If your current carrier has handled claims well, provides responsive service and offers competitive terms, the stability and reliability of that relationship have value. Factor in the full picture, not just the price tag.

Step 6: Meet with your insurance agent or broker.

Schedule a dedicated meeting with your insurance agent or broker to walk through the findings of your review. This is not a five-minute phone call — block enough time for a thorough conversation. Come prepared with your current policy summaries, your list of business changes, any new contracts or lease agreements with insurance requirements, and the competitive quotes you’ve gathered.

Ask your agent to review your findings and identify any gaps or redundancies you may have missed. A good commercial insurance agent will bring industry-specific knowledge and an understanding of emerging risks that you wouldn’t necessarily think to ask about. They can flag trends in your industry’s claims environment, recommend coverage adjustments based on how businesses similar to yours are being affected and help you prioritize which gaps to close first if budget is a constraint.

If you’ve filed any claims during the past year, discuss how they were handled, whether the claim revealed any coverage issues and how the claims may affect your renewal premiums. Claims experience is one of the most influential factors in your renewal pricing, and your agent can help you understand the impact and develop strategies to mitigate premium increases.

This meeting is also the time to review your certificates of insurance. Confirm that all parties who require additional insured status are properly listed, that the coverage limits on outstanding certificates match your current policy limits and that any new relationships requiring certificates are addressed.

Step 7: Implement changes and document everything.

Once you’ve made any decisions, implement all coverage changes, limit adjustments and carrier switches before your renewal date. Allowing changes to take effect at renewal avoids mid-term adjustments and keeps your policy periods clean.

Request updated certificates of insurance for every third party that requires them — landlords, clients, lenders and partners. Distribute them proactively rather than waiting to be asked. Proactive certificate distribution demonstrates professionalism and prevents the scramble that occurs when a third party discovers your certificate has lapsed or doesn’t reflect current coverage.

Update your internal records. Create or refresh a summary document listing all active policies, including the carrier name, policy number, coverage type, limits, deductibles, annual premium and renewal date. Store your policy documents in a secure, accessible location — both digital copies (using cloud storage or high-quality document management software) and physical copies if you prefer a paper backup. This summary document becomes the starting point for next year’s review.

Finally, set a calendar reminder for 60 to 90 days before your next renewal date. The most effective insurance reviews happen on a predictable schedule. If you make the annual review a standing item on your business calendar, it becomes a routine part of operations rather than a task that gets deferred until a problem forces your hand.