Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

When to Get a Standalone Insurance Policy vs. Business Owner’s Policy Bundle

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

When you’re shopping for business insurance, one of the first decisions you’ll face is whether to purchase individual standalone policies for each type of coverage or to bundle your core coverages into a single package. The most common bundle is a business owner’s policy, or BOP, which combines general liability and commercial property insurance into one policy at a lower premium than purchasing both separately.

The right answer isn’t always one or the other. Many businesses use a bundle as their foundation and supplement it with standalone policies for risks the bundle doesn’t cover. Understanding what a BOP includes, what it leaves out and when standalone policies are the better choice helps you build an insurance program that covers your actual risks without paying for coverage you don’t need. Then, learn how to decide between a standalone policy and a BOP bundle, and when a hybrid approach makes the most sense.

FYI

If you're ready to purchase standalone or bundled insurance policies, business.com's guide to the best business insurance is a great place to find reputable insurers.

What is a business owner’s policy (BOP)?

A business owner’s policy is a bundled insurance package designed for small to mid-sized businesses with relatively standard risk profiles. It combines two essential coverages — general liability insurance and commercial property insurance — into a single policy with a single premium, typically priced lower than buying each coverage separately. Most BOPs also include business interruption coverage as a standard component, adding a third layer of protection at no additional cost beyond the bundled premium.

Insurers set eligibility criteria for BOPs based on factors like annual revenue, number of employees, industry classification, and the square footage of the insured premises. Not every business qualifies — higher-risk industries, very large operations, and businesses with complex or unusual exposures may not be eligible for a standard BOP and will need to build their coverage program from standalone policies.

One critical point that is frequently misunderstood: A BOP is not a comprehensive insurance program. It covers your core general liability and property needs, but it doesn’t include workers’ compensation, commercial auto, professional liability, health insurance or several other important coverage types. These always require separate standalone policies regardless of whether you have a BOP.

When you purchase a business owner’s policy, your BOP will usually include general liability, commercial property and business interruption coverage.

General liability

The general liability component of a BOP provides the same coverage you’d get from a standalone general liability policy. It covers third-party bodily injury claims (e.g., a customer is injured on your premises), third-party property damage claims (your business operations damage someone else’s property) and advertising injury claims (allegations of libel, slander or copyright infringement in your marketing). Standard coverage limits are commonly $1 million per occurrence and $2 million in aggregate, though limits vary by insurer and plan.

Bundling general liability into a BOP doesn’t reduce the scope or quality of the coverage. You’re getting the same protection at a lower price because the insurer benefits from packaging multiple coverages together.

Commercial property

The commercial property component covers business-owned physical assets: the building itself (if you own it), furniture, fixtures, equipment, inventory, signage, and in many cases, tenant improvements and betterments you’ve made to a leased space. Coverage typically protects against damage or loss from fire, theft, vandalism, windstorms, lightning and certain other perils.

An important limitation: Flood damage and earthquake damage are almost universally excluded from standard commercial property coverage, whether it’s within a BOP or a standalone policy. If your business is located in an area with flood or earthquake risk, you’ll need separate policies for those specific perils.

Business interruption

Business interruption coverage, included in most BOPs, pays for lost income and ongoing operating expenses if your business is forced to close temporarily due to a covered property loss. If a fire damages your retail space and you can’t operate for three months while repairs are completed, business interruption coverage helps pay your rent, employee wages, loan payments and other fixed costs during the closure.

The coverage amount and duration vary by policy. Some policies cover lost income for up to 12 months, while others have shorter periods. Most include a waiting period (typically 48 to 72 hours) before coverage begins. When evaluating a BOP, pay attention to the business interruption terms — this coverage can be the difference between surviving a major property loss and closing permanently.

What a BOP doesn’t cover

Understanding what a BOP excludes is just as important as understanding what it does. The following coverages are not part of a standard BOP and must be obtained through standalone policies or, in some cases, optional insurance endorsements added to the BOP.

Coverage Type

Why It’s Not in a BOP

Workers’ Compensation

Legally mandated coverage governed by state-specific rules; always a separate policy

Commercial Auto

Covers business-owned vehicles; requires its own policy with state-mandated liability limits

Professional Liability (E&O)

Covers claims from professional services and advice; distinct risk category from general liability

Cyber Liability

Covers data breaches and digital threats; some insurers offer it as a BOP endorsement, but dedicated standalone policies provide broader protection

Employment Practices Liability (EPLI)

Covers employee claims of wrongful termination, discrimination, harassment; typically standalone

Directors and Officers (D&O)

Covers personal liability of company leadership; relevant for businesses with boards or investors; always standalone

Liquor Liability

Required for businesses serving alcohol; available standalone or as an endorsement, depending on insurer

Flood and Earthquake

Excluded from standard property coverage; requires separate standalone policies

Product liability deserves a specific note. Basic product liability coverage is often included within the general liability component of a BOP, but the limits may be insufficient for businesses that manufacture products, sell food or deal in goods with elevated injury risk. If product-related claims are a significant exposure for your business, you may need a standalone product liability policy or enhanced limits beyond those provided by the BOP.

When a BOP makes sense

A BOP is the right choice for a significant share of small businesses. It makes sense when:

Your business has standard general liability and commercial property needs without unusual risk concentrations

You operate from a physical location and need property coverage alongside liability

You want the simplicity of managing one policy with one premium and one renewal date for your core coverages

You’re looking for cost savings on coverages you’d need to buy anyway

The types of businesses that are strong BOP candidates include:

Retail shops, restaurants and cafes

Office-based professional services firms

Salons and spas

Small manufacturers

Medical and dental offices

Similar brick-and-mortar or office-based operations

These businesses share a common profile: They operate from a physical location, interact with customers or the public, and have well-understood, relatively standard general liability and property risks.

The cost advantage of a BOP is another factor to consider. Insurers price BOPs lower than the combined cost of standalone general liability and commercial property policies because bundling reduces their administrative costs and increases customer retention. For a business that needs both coverages, there’s rarely a financial reason to buy them separately.

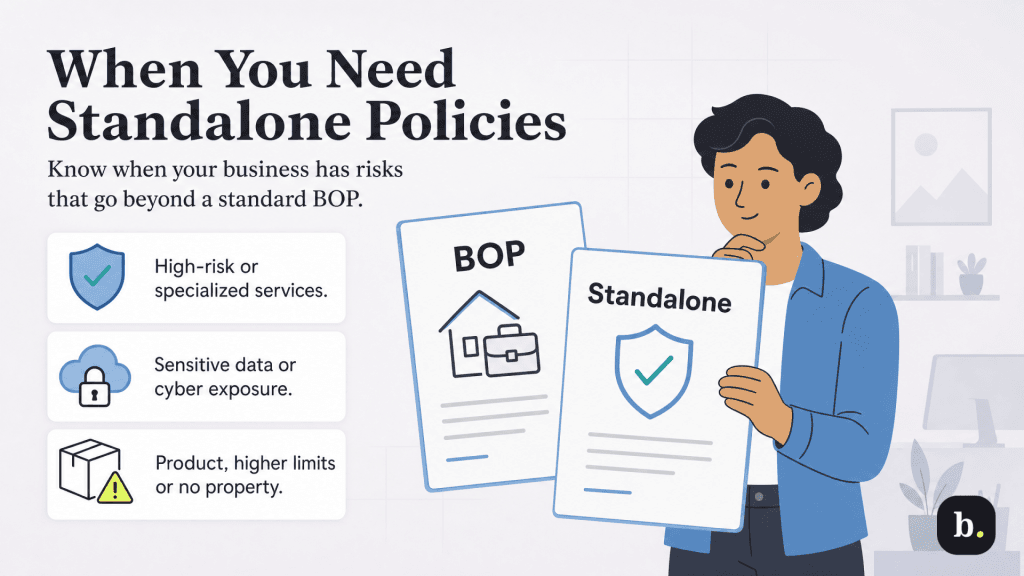

When you need standalone policies

Though there are distinct advantages to a BOP and bundling your insurance policies, there are situations where you may need standalone policies instead or in addition to a bundle.

Your risks exceed what a BOP covers.

If your business has significant professional liability exposure — you provide consulting, IT services, design, accounting, legal or medical services — you need a standalone professional liability (errors and omissions) policy. A BOP’s general liability component explicitly excludes claims arising from professional services and advice. No amount of general liability coverage will protect you against a client’s allegation that your professional work caused them financial harm.

If you handle sensitive customer or employee data, a standalone cyber liability policy provides dedicated coverage for data breaches, ransomware attacks, regulatory fines, notification costs and business interruption resulting from cyber incidents. While some insurers offer cyber liability as an endorsement that can be added to a BOP, standalone cyber policies typically provide broader coverage, higher limits and more robust incident response services.

If your primary risk is product-related — you manufacture goods, produce food or sell consumer products with meaningful injury potential — the product liability sublimit within a BOP’s general liability component may not be sufficient. A standalone product liability policy with higher dedicated limits may be necessary to protect your business adequately.

You need higher limits than a BOP provides.

BOPs typically offer general liability limits of $1 million per occurrence and $2 million in aggregate. For many small businesses, these limits are adequate. But if your contracts require higher limits — enterprise clients, government contracts and large commercial landlords sometimes require $2 million or more per occurrence — you may need a standalone general liability policy with higher base limits.

Alternatively, a commercial umbrella policy can sit on top of your BOP and provide additional liability coverage above the BOP’s limits. Umbrella policies are often the most cost-effective way to achieve higher total limits because they extend coverage across multiple underlying policies (general liability, commercial auto, employer’s liability) rather than requiring you to increase each policy’s limits individually.

Similarly, if your property values exceed the limits available within a BOP — because you maintain large inventories, own expensive equipment or have invested heavily in tenant improvements — a standalone commercial property policy may offer higher limits and more customization than a BOP’s property component allows.

You don’t need property coverage.

The property component is a core part of what makes a BOP a BOP. If your business doesn’t have commercial property to insure — because you’re entirely remote, home-based or mobile — you’re paying for coverage you don’t need. In this case, a standalone general liability policy (and any other relevant standalone policies) is more cost-effective.

This scenario is increasingly common. Consultants, freelancers, software developers, online-only businesses and other professionals who work from home or client sites often don’t have a commercial lease, don’t own significant business equipment beyond a laptop and don’t maintain inventory. For these businesses, a standalone general liability policy paired with standalone professional liability and possibly cyber liability provides comprehensive protection without the cost of unnecessary property coverage.

Your industry has specialized requirements.

Some industries require specialized policy forms and coverages that aren’t available within a standard BOP. Contractors need builder’s risk and inland marine coverage. Transportation companies need motor truck cargo and trailer interchange coverage. Healthcare providers need malpractice insurance policies written on forms specific to their specialty. Cannabis businesses in states with legal markets often require industry-specific policy forms because standard insurers exclude cannabis-related operations.

If your industry requires coverage that a BOP simply can’t provide, those coverages will be standalone by necessity. In some of these cases, the specialized standalone policies may replace the need for a BOP entirely, while in others, you may still use a BOP for your general liability and property needs and add the specialized coverages on top.

Tip

Other types of specialty insurance include travel insurance, motorcycle insurance and identity theft insurance. Specialized insurance may be unique and even unusual in some cases, depending on business needs.

How to decide between a standalone policy vs. a BOP bundle

Rather than approaching the BOP-versus-standalone question as a binary choice from the outset, use the following framework to build your insurance program from the ground up.

1. Start with the legally required coverages. Workers’ compensation, unemployment insurance, state-mandated disability and commercial auto (if you own business vehicles) are always standalone policies regardless of anything else in your program. Get these in place first.

2. Determine whether you need both general liability and commercial property. If you operate from a physical location, lease commercial space or own significant business property, the answer is almost certainly yes — and a BOP is likely the most cost-effective way to obtain both. If you’re remote, home-based or don’t have commercial property, a standalone general liability policy without the property component is the better fit.

3. Identify your business-specific risks that fall outside a BOP. Professional liability, cyber liability, employment practices liability, product liability beyond basic limits, liquor liability and any industry-specific coverages all require standalone policies or endorsements. List every risk exposure that your BOP wouldn’t cover.

4. Get quotes for both scenarios. Ask your insurance agent or broker to quote a BOP plus the necessary standalone add-ons and, separately, an all-standalone program. Compare the total premium and total coverage of each scenario. In most cases, a BOP-based hybrid approach (see below) will be cheaper for equivalent coverage, but the all-standalone approach may make sense if you don’t need property coverage or if your risks don’t align well with a standard BOP’s structure.

5. Work with a licensed commercial insurance agent or broker. An experienced broker can run both scenarios, identify gaps you might miss, and recommend the structure that provides the best combination of coverage and cost for your specific situation. They can also identify which insurers offer BOP endorsements for coverages like cyber liability or liquor liability, which may simplify your program and reduce your total cost compared to purchasing those as fully standalone policies.

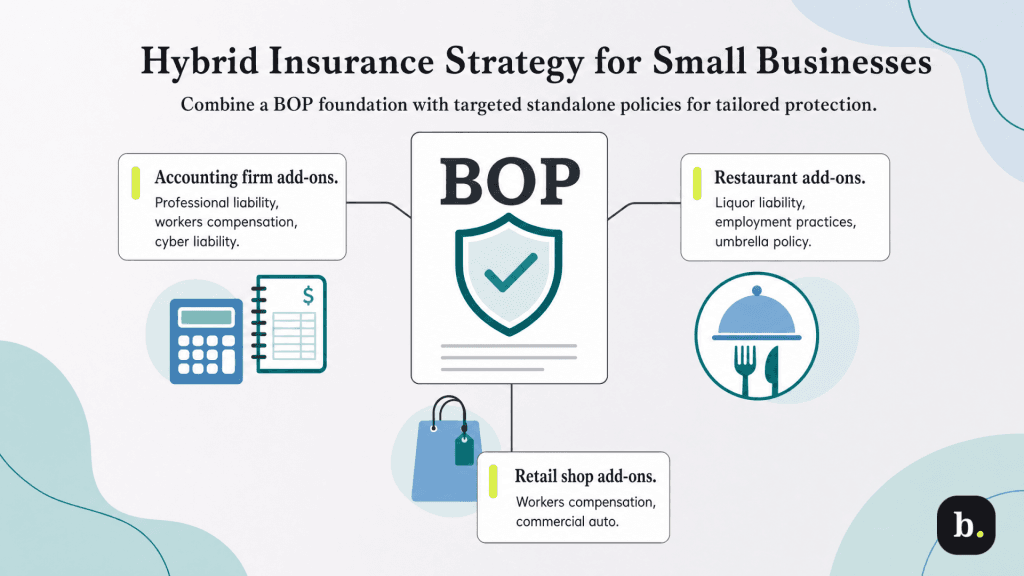

The hybrid approach: BOP plus standalone policies

In practice, the most common and most effective insurance structure for small businesses is a hybrid: a BOP as the foundation for core general liability and property coverage, supplemented by standalone policies for specific risks the BOP doesn’t address. This approach gives you the cost efficiency and simplicity of bundling your standard coverages while ensuring you have dedicated, appropriately sized coverage for your specialized exposures.

To illustrate how this works in practice, consider the following examples.

A small accounting firm with a leased office, three employees and clients who require professional liability coverage might carry a BOP (covering general liability, commercial property and business interruption) plus standalone professional liability, workers’ compensation and cyber liability. The BOP handles the firm’s standard premises and general liability needs, while the standalone policies address professional risk, employee injury risk and data security risk that the BOP doesn’t touch.

A retail shop with a delivery van and five employees might carry a BOP plus standalone workers’ compensation and commercial auto. The BOP covers the shop’s general liability, inventory, fixtures and business interruption needs. Workers’ comp covers employee injuries. Commercial auto covers the delivery vehicle. Each coverage addresses a distinct risk that the others don’t.

A restaurant serving alcohol with 15 employees might carry a BOP with a liquor liability endorsement, standalone workers’ compensation, employment practices liability insurance and a commercial umbrella policy for additional liability limits. The BOP provides the core property and liability foundation; the liquor liability endorsement extends the BOP to cover alcohol-related claims; and the standalone policies address employment risk, employee injury risk and the need for higher total liability limits.

In each case, the BOP serves as an efficient base layer, and the standalone policies fill gaps that the BOP was never designed to cover. The result is a comprehensive insurance program tailored to the business’s actual risk profile.

Ensuring your business is protected

For most small businesses with a physical location and standard risk profiles, a business owner’s policy is the most cost-effective way to secure core general liability and commercial property insurance coverage. It bundles two essential coverages into a single, lower-cost package and typically includes business interruption coverage as well. But a BOP is a foundation, not a complete insurance program — most businesses need at least one or two standalone policies alongside their BOP to cover risks the bundle doesn’t address.

If your business is remote, has no commercial property to insure or has highly specialized risk exposures that don’t fit within a standard BOP, standalone policies give you the flexibility to build a program tailored precisely to your needs without paying for coverage that doesn’t apply.

The right structure is the one that covers all of your actual risks at the most reasonable cost. Start with the legal requirements, build your core liability and property coverage (via BOP or standalone), layer in standalone policies for your specialized exposures and revisit the structure annually to ensure it still fits your business as it evolves.

Adam Uzialko, the accomplished senior editor at Business News Daily, brings a wealth of experience that extends beyond traditional writing and editing roles. With a robust background as co-founder and managing editor of a digital marketing venture, his insights are steeped in the practicalities of small business management.

At business.com, Adam contributes to our digital marketing coverage, providing guidance on everything from measuring campaign ROI to conducting a marketing analysis to using retargeting to boost conversions.

Since 2015, Adam has also meticulously evaluated a myriad of small business solutions, including document management services and email and text message marketing software. His approach is hands-on; he not only tests the products firsthand but also engages in user interviews and direct dialogues with the companies behind them. Adam's expertise spans content strategy, editorial direction and adept team management, ensuring that his work resonates with entrepreneurs navigating the dynamic landscape of online commerce.