Blockchain tech has expanded beyond recording cryptocurrency transactions. Telecom companies, transport and logistics firms, retailers, healthcare providers and media companies use blockchain daily for various purposes. Now, the technology is making inroads in the digital marketing sector. Advocates expect blockchain to reduce ad fraud, protect customer data and direct more revenue to blog and news site owners who allow ads on their sites.

We’ll define blockchain, explain its appeal and explore how it’s being used in digital marketing. We’ll also assess the likelihood of today’s digital marketing giants adopting the technology.

Searching for digital marketing services and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

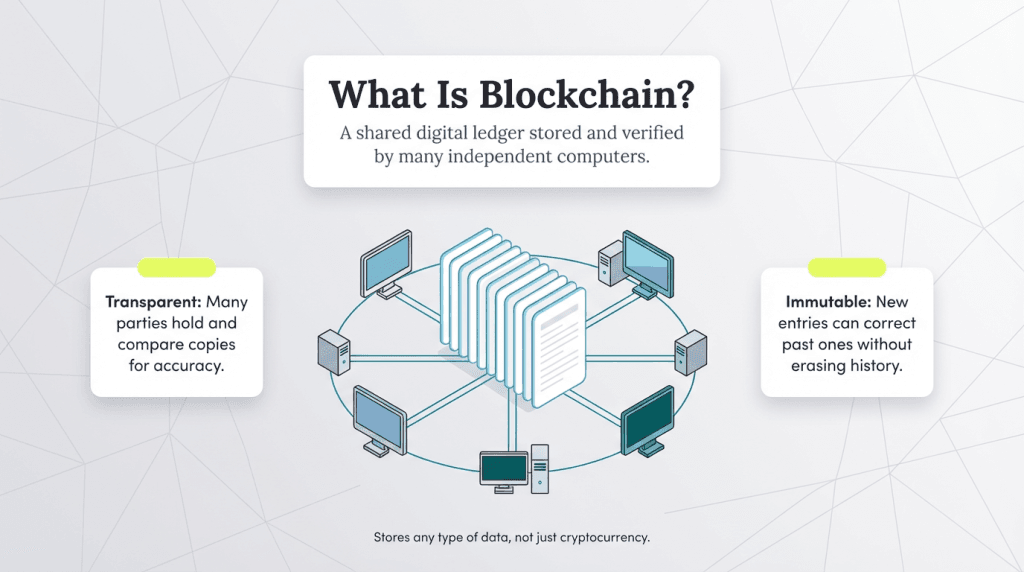

What is blockchain?

A blockchain is a database that records information. “The blockchain is, most simply put, many individual computers that are networked to store data and facilitate transactions,” explained Tim K, head of marketing at the derivatives liquidity protocol company Synthetix.

“The biggest difference from traditional computer networks or databases is that instead of one company or person owning it, selling the service and profiting from it, it is generally free for anyone to participate in a distributed fashion,” Tim added.

Blockchain advocates emphasize the technology’s two compelling and unique selling points over a traditional database:

- Blockchain databases are transparent: Unlike a standard centralized database or ledger, blockchain databases are held by multiple independent parties who cross-reference each other for accuracy. Members of the public can check multiple copies of the database to verify an individual data record.

- Blockchain databases are immutable: Data cannot be changed after it has been entered into a ledger. If a mistake is made, a new data item must be added to the ledger to reverse the previous one. Both data items exist and are visible on all copies of the ledger.

While cryptocurrency transactions were initially the primary type of data recorded on the blockchain, the technology can store any type of data.

How will blockchain affect digital marketing?

Blockchain technology can impact your digital marketing strategy in the following ways.

1. Blockchain can improve keyword tracking.

What one person sees on Google is often unique to them. Search results vary based on factors like location and device, making it challenging for marketers to track keyword rankings accurately. However, if blockchain were integrated into search, individual page rankings could be stored on the blockchain, along with data on location and device usage for each ranking position.

Marketers could use these data analytics insights to identify actions needed to improve visibility in specific regions and on particular devices. The same data could help determine why some locations appear in Google’s Local Pack results while others do not.

Beyond simple keyword tracking, the blockchain can also facilitate a deeper marketing understanding of a target audience’s wants and needs.

“I feel like in crypto and the blockchain, it goes beyond the Web2 equivalent of keyword searching and SEO,” explained Justin Vogel, the co-founder of Safary, a Web3 analytics company. “The Web3 equivalent is sentiment analysis to understand how people are talking about my project in real time.”

Vogel noted that this approach will become increasingly important as consumer tracking faces growing challenges due to heightened privacy concerns and other limitations within traditional Web2 marketing.

If your address on Google and Yelp is incorrect, change it. Listing the wrong address hurts

online brand awareness and lowers your chances of appearing in the Google Local Pack.

2. Blockchain can improve lead quality.

Consumers who give your brand their data are likely interested in your company. This makes it much easier to generate sales leads and convert leads to sales as these prospects are already primed for engagement.

Currently, marketers collect data from various sources, consolidate it and run campaigns based on the combined information. This method is imperfect and many campaigns end up relying on inconsistent or incorrect data.

However, because blockchain transactions are decentralized, marketers must go directly to the source — the consumer. Brave exemplifies this with its ad-supported browser, which blocks traditional ads by default but allows users to opt into seeing ads sold via Basic Attention Tokens (BAT). Users earn 70 percent of the ad revenue in BAT while Brave retains 30 percent.

How does Brave target ads? Users share as much or as little personal data as they choose. Advertisers select audiences based on anonymous demographic data, never learning the identities of those viewing their ads. This privacy-focused model may represent the future of digital advertising.

“I think Brave is a great product and a good use of blockchain advertising,” Tim K shared. “They continue to innovate a very competitive alternative to Chrome browser and their direct rewards to users for opting into viewing ads will surely be imitated and improved in the future.”

3. Blockchain provides tools for tackling ad fraud.

As marketers know too well, advertising fraud is a persistent issue. Verasity, an anti-ad fraud industry company, reported in its Whitepaper 2024 that ad fraud led to a loss of $84 billion in ad spend in 2023; this is projected to rise to $170 billion by 2028.

To combat ad fraud, Verasity’s VeraViews tool uses blockchain to analyze first- and third-party data to determine a score reflecting how likely it is that a user saw an ad. Tools like VeraViews promise advertisers they’ll only pay for valid views and assure publishers of faster, more accurate payments thanks to blockchain’s speed and immutability.

“Blockchain addresses can be attached to browsers, apps or extensions installed by customers who are verified by KYC, social or account means,” Tim K explained. “This would create an unfakable, auditable digital record stored in the blockchain permanently to prove they are real, unique individuals.”

4. Blockchain delivers enhanced transparency for consumers.

Authenticity and business transparency are vital for brands that want to attract Gen Zers and millennials, especially when it comes to supporting causes like fair trade and environmental responsibility. Additionally, consumers often prefer dealing with organizations with a sustainable business model.

For example, a coffee brand could use blockchain to publicize its supply chain. Someone who wants to purchase ethically sourced coffee might check the blockchain of a brand they’re considering using to determine who grows their beans and how much they get paid. They could track the entire life cycle of that brand’s coffee to see when it left the farm, how long it was on the ship and which facility ground the beans. Consumers could even see the average temperature the coffee beans were stored at on the transport ship.

Blockchain offers transparency and its immutability means it can be trusted. For brands, this enhanced transparency can lead to greater efficiency and lower transaction costs.

Behind bitcoin, ethereum is the second-most popular choice of cryptocurrency for

401(k) retirement plan inclusion.

5. Blockchain prioritizes user privacy.

A key component of blockchain technology is its ability to prioritize user privacy. This stands in contrast to current digital marketing practices, which emphasize harvesting as much identifiable user data as possible.

“Blockchain can be used for making sensitive consumer information more difficult to hack by encrypting it and inheriting the enhanced security of blockchain,” Tim K explained. “It could also be used to gain the trust of consumers to opt in for more personalized services and volunteer more sensitive data by virtually guaranteeing their information cannot be misused or accessed without their permission.”

This shift in privacy is rooted in the differences between the current Web2 internet and the emerging, blockchain-powered Web3, particularly in how digital marketing and “identity” are treated.

“I think that there’s an interesting thing here, where basically you have a world in which in Web2 people’s identities are public and your transactions are private,” Vogel noted. “That is one privacy paradigm — public personas, private transactions.” In contrast, with crypto and Web3, consumer identities are private, but transactions are public. “For example, you can see all of a person’s transactions on, say, Amazon, but you don’t know who that person is unless they’ve identified themselves in some way,” Vogel added.

This unique privacy approach allows individual users to create multiple Web3 personas, each hiding as much of their real-world identity as desired while making transactions public. Users could develop specific personas for various activities, allowing digital marketers to tailor content to each persona’s public transactions without needing to access the user’s real-world identity.

6. Blockchain can improve loyalty rewards programs.

The blockchain makes all transactions visible, verifiable and irrefutable, which can help digital marketers and brands better tailor their offerings to long-time customers. For example, a fully verified transaction history can help marketers tailor their rewards and loyalty programs to uniquely appeal to each customer.

“The blockchain could be used in ways that allow consumers and customers to receive rewards for when they do opt in to more personalized offers and advertising experiences,” explained Tim K. “It could enhance loyalty programs with digital collectibles, micropayments and transferable points.”

Brand and digital marketers can further leverage the blockchain by adding transactions to a specific user’s blockchain history. These “badges” can be unique rewards, digital tokens or specific unlockables that demonstrate customer loyalty and are visible across the web.

“I think there are a lot of unique advantages in the non-financial transaction piece of this technology,” says Vogel. “[These include features like] being able to tag, reward and label users, create loyalty and have loyalty level up with different badges that can be seen across different companies and across time, using tools like NFTs [nonfungible tokens] and various mechanisms to show a user’s progression.”

What businesses or industries will blockchain tech affect?

According to Inkwood Research, the global digital marketing software sector is expected to reach $286.93 billion by 2032. However, it’s uncertain how significant a role blockchain will play in that growth. While it’s still early to gauge its full impact, initial adoption in digital marketing has been slow — but there is potential for future integration.

Market leaders seem unaffected by blockchain tech right now.

Google, Facebook and other tech giants have invested hundreds of billions of dollars to create the following:

- Enormous demographic databases that cover billions of people around the world.

- Advertising platforms that effectively deliver client results, encouraging continued use.

The commercial advantage of incorporating blockchain for these companies remains unclear, as it would require them to surrender control partially or fully over their data and platforms.

Blockchain may work for ad demand-side platforms.

Blockchain is making progress in selling ads on third-party sites, similar to the Google AdSense business model.

Common complaints with existing systems include their susceptibility to click fraud and the tendency for publishers to be shortchanged due to numerous intermediaries, such as demand-side platforms.

IBM and Mediaocean are among the most prominent players pushing to create a blockchain-based network similar to AdSense. However, they face growing competition in this space as more companies explore blockchain’s potential in advertising.

No blockchain social media platform has found major success.

A number of blockchain social media companies have launched and subsequently struggled. Consider these examples:

- Peepeth: This platform, inspired by X (formerly Twitter), was designed to promote “mindful discourse and effective altruism.” However, the platform has not received updates since January 2021 and its current status is uncertain.

- Sapien: Initially a social news platform similar to a cross between the Facebook news feed and Pinterest, Sapien has since evolved into a broader initiative focused on becoming a decentralized autonomous organization.

- Steemit: Steemit has achieved a higher level of success than other examples. This social network allows creators to earn money from user-generated content based on an upvoting system. As of 2024, it has over 1 million registered users.

Other blockchain-based social media apps, such as Sociall and WildSpark, have floundered. In fairness to these apps’ creators, it’s almost impossible to create a new social platform that scales quickly enough to benefit from the “network effect,” which the leading platforms enjoy regardless of whether they’re blockchain-powered.

Social media

influencer marketing fraud is a big problem in which "influencers" charge for access to mostly fake followers. Search the internet for "fake follower tools" to find apps that can help you determine the quality of an influencer's following.

Advertisers and publishers seem happy with the status quo.

Advertisers are not significantly pressuring lawmakers to further regulate existing digital marketing platforms, let alone compel them to adopt a blockchain model. However, as the technology matures, advertisers may consider blockchain for its potential cost-saving benefits.

Meanwhile, Brave has carved out a nice niche for itself; it now has 30.1 million daily active users and 1.6 million content creators. In addition to its “Rewards” feature, the company has launched its own search engine that offers paid-for search advertising; users can opt out of this service by paying for an ad-free experience.

Right now, it’s hard to see blockchain influencing digital marketing trends in the short to medium term. But keep an eye on developments in this dynamic sector. Remember, 15 years ago, few people thought cryptocurrencies had a future and the vast majority were wrong.

“We’re in the ‘AOL era’ of blockchain and haven’t yet realized its full potential,” said Tim K. “I believe blockchain will become widely adopted by companies in a bid to win the trust, loyalty and business of consumers by incorporating it in various ways that are more user-friendly than today’s experience.”

Jeremy Bender contributed to this article.