When an online order comes through, most business owners are focused on the same thing: getting it approved, packed and out the door. The last thing anyone wants to discover days or weeks later is that the payment was fraudulent and the money is already gone.

That’s the reality of online payment fraud. In most cases, when a fraudulent card transaction slips through, the merchant absorbs the loss — not the cardholder and not the issuing bank. That can mean losing the sale, the product or service you already delivered and, in many cases, paying a chargeback fee on top of it.

This guide explains how online payment fraud happens, the tactics fraudsters use and the tools and strategies small businesses can employ to stop suspicious transactions before they turn into lost revenue and frustrated customers.

What is online payment fraud?

Online payment fraud is the use of stolen, compromised or fake payment information to make purchases without the legitimate cardholder’s knowledge or authorization. And in many cases, nothing looks suspicious at first. The payment is approved, the order looks legitimate and the product often ships before anyone realizes something is wrong.

By the time the real cardholder notices the unauthorized charge and disputes it with their bank, the merchant is often left absorbing the loss. That may include the transaction amount, the product or service already delivered, processing fees and, in many cases, a chargeback.

Unlike in-person transactions, where EMV chip cards can shift some credit card fraud liability, online purchases are considered card-not-present transactions. In practice, that usually means the merchant is responsible for proving the transaction was legitimate.

How online payment fraud works

Most fraudulent online transactions don’t start with a massive purchase or an obviously suspicious order. More often, they start quietly — a few small test transactions, a strange pattern or activity that doesn’t look like much at first. Here’s how it usually unfolds.

- A fraudster gets payment or account information: Fraud may start with stolen card data, compromised login credentials, synthetic identities (fake identities created using a mix of real and made-up personal information), automated bot attacks or card information purchased on the dark web.

- They test whether the information works: One common early-stage tactic is card testing, where fraudsters run small transactions — sometimes for just a few cents — to confirm that a stolen card number is active. If the test transaction goes through, the card may be used for larger purchases, either at your business or somewhere else.

- A larger purchase is made: Once the payment information is confirmed to be active, the fraudster may place one or more higher-value orders using the same card or account. Depending on your online store, that could mean physical products, digital goods, gift cards or subscription services.

- The transaction looks legitimate at first: Because online transactions happen without a physical card, signature or face-to-face verification, merchants have fewer built-in ways to confirm that the person making the purchase is the authorized cardholder. The order may be approved, processed and shipped before anyone realizes something is wrong.

- The real cardholder disputes the charge: The fraud usually comes to light when the cardholder notices the unauthorized transaction and contacts their bank. At that point, the merchant may lose the sale, the product or service already delivered and any chargeback fees tied to the dispute.

By the time the fraud is discovered, the transaction often looks complete, the order may already be fulfilled and the financial loss usually falls on the merchant. That’s what makes online payment fraud so difficult — and so expensive — to catch after the fact.

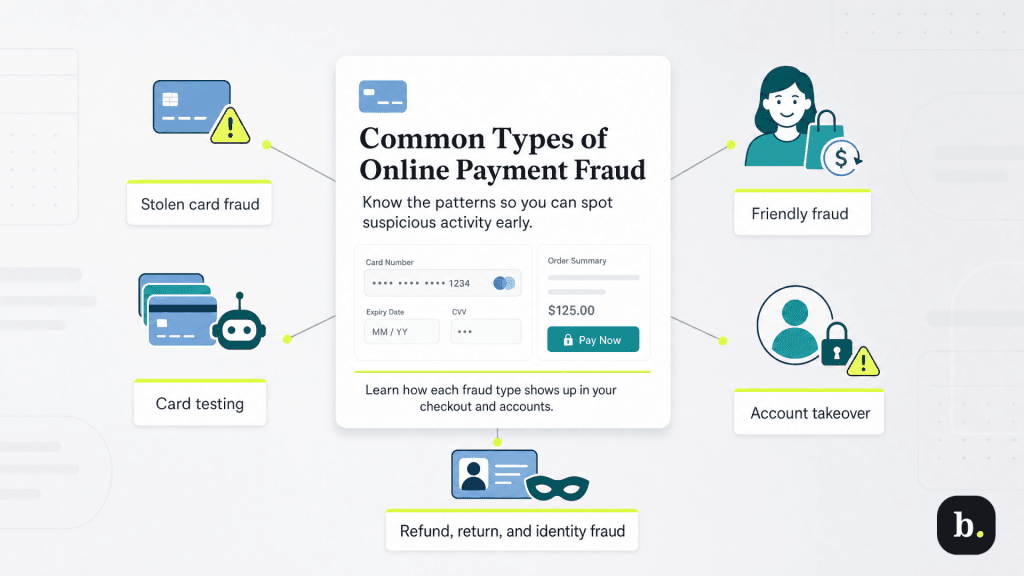

Common types of online payment fraud

Not all online payment fraud looks the same. Some schemes rely on stolen card numbers. Others involve real customers, compromised accounts or fraudsters looking for weak spots in your checkout process. The more familiar you are with the most common fraud patterns, the easier it becomes to spot suspicious activity before it turns into lost revenue, chargebacks or damaged customer trust.

Stolen card fraud

Stolen card fraud is exactly what it sounds like: a fraudster gets access to someone else’s credit card information and uses it to make unauthorized purchases online. Those card details may come from data breaches, phishing scams, skimming devices or card information sold on the dark web.

At first, the transaction may look completely routine. The payment is approved, the order is processed and the product ships. The fraud often doesn’t come to light until the real cardholder spots the charge on their statement and disputes it with their bank. By then, the merchant may be out the sale, the product and the chargeback fee.

Card testing

Card testing is often one of the earliest warning signs that fraudsters have found your checkout page. Instead of placing one large order, they use bots to run dozens, hundreds or even thousands of small transactions to see which stolen card numbers are still active.

The transactions themselves may be tiny — sometimes just a few cents — but the impact can add up quickly through processing fees, operational headaches and potential chargebacks. Common warning signs to look for include a sudden spike in low-dollar transactions, repeated attempts from the same IP address or multiple orders placed in rapid succession using similar billing or shipping details.

Card testing is more common than many business owners realize. Visa’s 2026 Global eCommerce Payments & Fraud Report found that card testing impacted 33 percent of merchants worldwide in the past year.

Friendly fraud

Friendly fraud happens when a customer makes a legitimate purchase, receives the product or service and later disputes the charge with their bank anyway. Sometimes, the buyer regrets the purchase. Sometimes a family member bought the item or service and the cardholder doesn’t recognize the charge. In other cases, it’s an intentional attempt to get something for free.

That’s what makes friendly fraud so difficult to catch. The original transaction usually looks completely legitimate, and the dispute itself is where the fraud begins. And it’s becoming harder for merchants to ignore. In the above-cited report, Visa found that 64 percent of merchants reported increasing rates of “first-party misuse” — the industry’s term for friendly fraud — in the past year.

Account takeover

In an account takeover attack, a fraudster gains access to a legitimate customer account on your website and uses that existing trust to make unauthorized purchases.

This often happens through credential stuffing (using stolen username and password combinations from previous data breaches), phishing attacks or social engineering scams. Once inside the account, the fraudster may place orders using stored payment methods, change shipping details or access sensitive customer information.

Because the activity is happening inside a real customer account, account takeover attacks can be especially difficult to spot and can be uniquely damaging to customer loyalty and trust.

Refund and return fraud

Refund and return fraud happens when someone manipulates your return, refund or dispute process for financial gain.

In some cases, a fraudster makes a purchase using stolen payment information, then requests a refund to a different card or account. In others, they claim an order never arrived, dispute a legitimate charge or return counterfeit, damaged or entirely different merchandise while keeping the original item.

For businesses with generous return policies, these schemes can quietly eat away at revenue if they go unnoticed. In its fraud report, Visa found that 61 percent of merchants reported rising refund or policy abuse in the past year, making it one of the most common forms of post-purchase fraud.

Identity fraud

Identity fraud happens when someone uses another person’s personal information to open accounts, place orders or pass identity checks they wouldn’t otherwise clear.

That information may include a name, address, date of birth or, in more serious cases, a Social Security number. Because the personal details themselves are real (even though they belong to someone else), these transactions can sometimes slip past basic verification tools.

Often, identity fraud doesn’t come to light until the real person notices unfamiliar accounts, unauthorized charges or other suspicious activity tied to their name.

Fraud usually shows up in patterns, not isolated transactions. Watch for sudden spikes in low-dollar purchases, mismatched billing and shipping details or multiple orders from the same IP address. If something feels off, take a closer look before the order ships.

Fraud prevention tools and technologies

By this point, one thing is probably clear: online payment fraud isn’t slowing down. Statista estimates that e-commerce losses to online payment fraud topped $56 billion worldwide in 2025 and could exceed $131 billion by 2030.

Effective fraud prevention doesn’t usually come down to one setting, one filter or one magic tool. The businesses that catch fraud most consistently tend to layer multiple checks together, with each tool flagging a different type of risk. Here are fraud prevention tools and technologies to consider:

Address Verification Service (AVS)

Address Verification Service, or AVS, compares the billing address a customer enters at checkout with the billing address the issuing bank has on file for that card. The system typically returns a match, partial match or no-match result. A mismatch doesn’t automatically mean fraud. A customer may have recently moved, entered a work address or simply made a typo. But when an AVS mismatch shows up alongside other warning signs, it can be an important signal that something deserves a closer look.

Many of the best credit card processors include AVS by default as part of their fraud screening tools. For most small businesses, a smart approach is to flag AVS mismatches for review rather than automatically declining every order, unless your fraud rate calls for a more aggressive approach.

CVV verification

CVV verification checks the three- or four-digit security code printed on a physical payment card to help confirm that the customer has access to the card itself, not just the card number. It’s a simple but effective way to catch fraud involving stolen card data from breaches, phishing scams or compromised online accounts, where the card number may be exposed but the CVV often isn’t.

For most online businesses, CVV verification should be a standard part of e-commerce security at checkout. It adds very little friction for legitimate customers while giving your payment system another useful signal when something doesn’t look quite right.

3D Secure (3DS)

3D Secure, often called 3DS, adds an extra identity check during checkout by asking the cardholder to verify the transaction through their issuing bank. The latest version, 3DS2, is designed to keep that process as frictionless as possible.

In many cases, customers won’t even notice it happening. 3DS2 uses risk-based authentication to evaluate transactions behind the scenes, and the customer is usually asked for additional verification — similar to multifactor authentication — such as a one-time passcode, fingerprint or facial scan only when something looks higher risk.

For many merchants, the biggest advantage of 3DS is the potential liability shift. When a transaction is successfully authenticated through 3DS, fraud-related chargeback liability typically shifts from the merchant to the issuing bank. In other words, if that transaction later turns out to be fraudulent, the merchant usually isn’t left absorbing the loss. That protection alone makes 3DS one of the most valuable fraud prevention tools available to online businesses.

That said, adding an extra authentication step can create a little friction for the small number of transactions that require active customer participation. For most merchants, though, it’s usually worth it, especially when the payoff is fewer fraudulent orders, fewer chargebacks and stronger customer trust.

Velocity checks

Some of the clearest fraud signals have nothing to do with the card itself; they come from how quickly transactions are happening.

Velocity checks look for activity that exceeds the limits you’ve defined within a certain time frame. That might mean the same card being used multiple times in a few minutes, several purchases coming from the same IP address within an hour or a string of failed payment attempts followed by one successful transaction. Patterns like these are often early warning signs of card testing, automated bot activity or other forms of attempted fraud.

The key is setting thresholds that match your business. For example, a busy coffee shop’s regular transaction velocity would look very different from that of a business equipment supplier. If you set your rules too aggressively, you risk losing real customers. But set them too loosely, and suspicious activity may slip through.

Device fingerprinting

Not every fraud signal comes from the payment details themselves. Sometimes the biggest clues come from the device behind the transaction. Device fingerprinting identifies the phone, tablet or computer being used to make a purchase by analyzing a combination of technical details, such as the browser version, operating system, screen resolution, IP location and other behind-the-scenes characteristics. Together, those details create a unique digital “fingerprint” for that device. This can be especially useful for spotting patterns that might otherwise go unnoticed, like the same device logging into multiple customer accounts, testing different digital payment methods or placing orders under different identities.

Most businesses won’t need to configure device fingerprinting themselves. It’s already built into many advanced fraud screening tools and works behind the scenes as transactions come through.

Machine learning and AI-based fraud screening

Some of the most effective fraud prevention tools don’t rely on fixed rules at all. Instead, they use machine learning and AI to evaluate each transaction in real time, looking for subtle patterns that may signal fraud. That might include unusual purchasing behavior, location mismatches, unfamiliar devices, repeated payment attempts or transaction patterns that don’t fit a customer’s typical behavior. Because these systems analyze millions of transactions across thousands of businesses, they can spot suspicious activity that would be nearly impossible for a human reviewer to catch consistently at scale.

And AI-based fraud screening is quickly becoming mainstream. The Visa report cited earlier found that 53 percent of merchants already use generative AI for fraud management, while another 22 percent say they’re likely to add it in the next 12 months.

As new fraud patterns emerge, these models continue learning from fresh transaction data, helping them get better at separating legitimate customers from high-risk activity. Tools like Stripe Radar, Signifyd, Kount and ClearSale are well-known examples. Some AI-powered fraud tools are built into popular payment processors, while others are available as paid add-ons or standalone services.

Other e-commerce fraud-prevention tactics

Automated tools are a great first line of defense, but they don’t catch everything. That’s why some lower-tech practices are still important, especially when an order doesn’t look quite right. Here are a few smart safeguards to keep in place:

- Don’t rely on automation alone: If something about an order feels off, take a closer look before it ships. A mismatched billing and shipping address may mean nothing on its own. But pair it with a new customer account, rush shipping, an unusually large order or a generic email address, and it may be worth a manual review. And when in doubt, contact the customer. A quick email or phone call often clears things up, while fraudsters usually disappear.

- Strengthen checkout and account security: Fraud prevention doesn’t stop at the payment page. Weak passwords, bot attacks and compromised customer accounts can create problems long before a transaction is submitted. To help combat this, require strong passwords, encourage two-factor authentication (or use an authenticator app), use CAPTCHA or bot detection on login and checkout pages, and limit repeated login or payment attempts within short time windows. For added protection, use payment tokenization instead of storing card data directly.

- Add safeguards to shipping and fulfillment: You have fewer options after the order ships. Use trackable shipping with delivery confirmation on every order, and consider signature confirmation for higher-value purchases. Be especially cautious with expedited shipping, unusually large first-time orders or shipments to addresses that don’t match billing details. And if something doesn’t sit right, waiting an extra day before shipping may save you a much bigger headache later.

- Monitor patterns and act quickly: Keep an eye on your business for anything out of the norm, such as an increase in chargebacks and unusual order activity. Keep detailed records on authorization details, shipping confirmations and customer communications. And if you notice a spike in fraud, let your payment processor know. They may be able to tighten your payment gateway settings or help you figure out what’s going on.

The best

online payment security combines smart technology with practical day-to-day habits, helping you reduce fraud, cut chargebacks and protect legitimate sales without making checkout harder for real customers.

Balancing security with the customer experience

Fraud prevention is a balancing act. Add too little security, and fraudulent transactions slip through. Add too much, and legitimate customers may get frustrated, abandon their shopping carts or never come back. That’s why the goal isn’t to eliminate fraud entirely. For most businesses, that isn’t realistic — and trying too hard can create just as many problems as it solves. The real goal is to catch suspicious activity while still delivering the great customer experience buyers expect.

Here are three ways to strike that balance:

- Layer low- and high-friction safeguards: Use low-friction tools like AVS, CVV verification, velocity checks, 3D Secure and AI-based risk scoring to screen most transactions quietly in the background. Save higher-friction measures — like manual reviews, order holds or direct customer outreach — for the transactions that genuinely look risky.

- Track false declines: Don’t just watch for fraud. Keep an eye on false declines too (legitimate transactions that get flagged or blocked by mistake). If too many good orders are getting stopped, your fraud settings may be costing you sales.

- Communicate when extra verification is needed: If you need to pause an order or verify a purchase, tell the customer why. A simple message like “For your security, we need to verify this order” is far better than a silent decline or an unexplained delay.

Smart fraud prevention protects revenue and customer trust

Online payment fraud is a growing threat, but it doesn’t have to catch your business off guard. With the right tools, a few common-sense checks and some practical safeguards, most businesses can reduce fraud without making checkout harder for legitimate customers.

Start with the protections already built into many payment systems, such as AVS, CVV verification, 3D Secure and baseline fraud screening. As your business grows, add stronger safeguards where they make sense — from velocity checks and account security to delivery confirmation and AI-based fraud screening.

Most importantly, keep your strategy flexible. Fraud tactics change, customer expectations evolve and your online payment security needs will grow right alongside your business. When your safeguards are working quietly in the background, you can focus on what matters most: protecting revenue, earning customer trust and delivering a great customer experience.