Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

It's essential for small and midsize business owners with e-commerce storefronts to understand the potential threats and damage of bot activity.

As technology advances, internet bot activity — both good and bad — is growing. Unfortunately, advanced bots have made it easier for fraudsters to commit crimes. According to the 2024 Imperva Bad Bot Report, almost a third of all internet traffic was attributable to bad bots.

Since bot traffic affects many verticals, small and midsize businesses (SMBs) need to understand the potential threats posed by bots. Here’s a look at bot-driven credit card testing fraud, how these attacks work and how you can protect your business and customers from this e-commerce threat.

A bot is an automated program that mimics human activity, according to Dr. Arun Vishwanath, author of “The Weakest Link.” “Think of it as a tireless worker executing tasks at lightning speed — whether it’s logging into accounts, spamming emails or gaming systems to commit fraud. Unlike humans, bots don’t tire, hesitate or make mistakes, which makes them formidable,” he said.

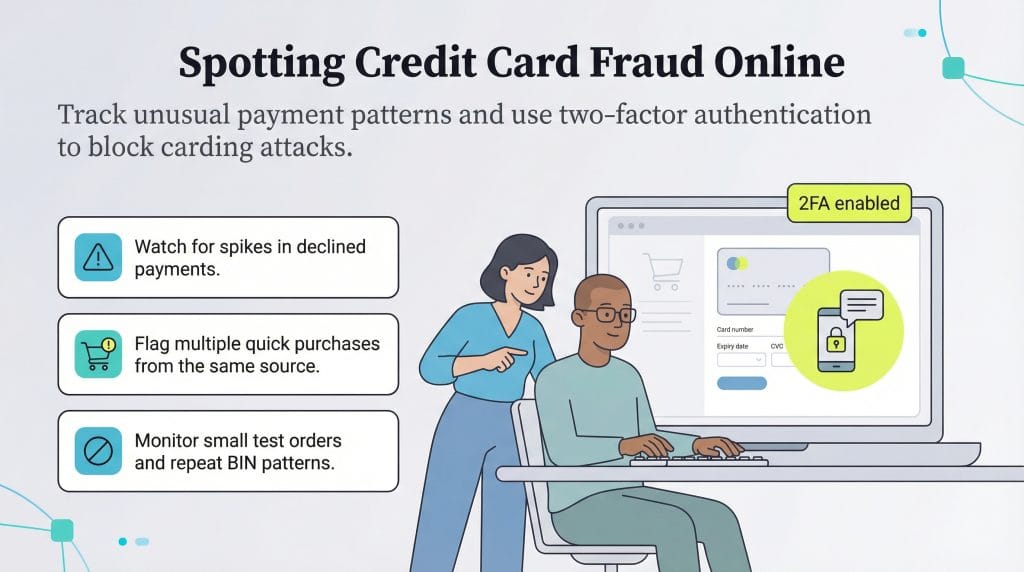

Bots often target online retailers by testing stolen credit cards with small purchases at odd hours, such as midnight, he explained. “Businesses might also notice unusual spikes in transactions — bulk purchases right before a sale or patterns that don’t match typical customer behavior,” added Vishwanath. “These are red flags. Spotting bots is a game of vigilance and pattern recognition, but tools like fraud detection software can help even the odds.”

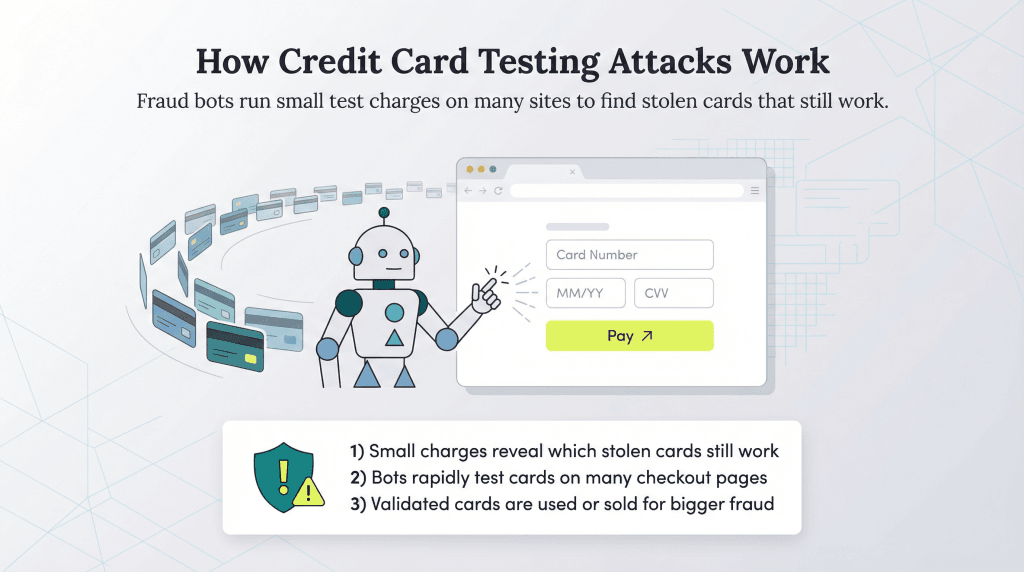

Credit card testing fraud, also known as carding and card cracking, is when cybercriminals make a small online purchase to test whether a stolen credit card number is valid.

Credit card testing often goes unnoticed by fraud detection solutions and is usually discovered only when it’s too late. Without proper measurements in place, credit card testing fraud can be costly and damaging to both SMBs and cardholders.

Fraudsters can potentially abuse any user-related function on your company’s website, such as the ability to enable payments. Once the scammer purchases a list of stolen credit card numbers, they test them to see which ones are valid by making small transactions on unsuspecting e-commerce sites.

Fraudsters can enable bots to do this work efficiently. A bot can submit orders on multiple websites automatically to check credit card validity much faster than a fraudster inputting card numbers one by one could.

The fraudster’s end goal is to find valid credit cards they can use to make large online purchases or sell the list of validated credit cards to other cybercriminals.

In 2019, a carding bot called the Canary Bot was discovered by PerimeterX, a provider of solutions designed to curb online fraud. The Canary Bot was designed to target e-commerce platforms. Mimicking a real shopper, the bot added products to an online shopping cart, set shipping information and completed the sale on multiple businesses within the platform.

The bot was discovered because its pattern differed from that of human shoppers. For example, activity increased before the holiday shopping season, which isn’t typical, since people usually wait for sales. The bot’s transactions also didn’t follow the usual human shopping time patterns; instead, the transactions happened randomly throughout the day.

Bot-driven credit card testing hurts SMBs with chargebacks, shipped goods that are never recovered, lost revenue from fraudulent sales and rising operational costs. After all, getting to the bottom of higher decline rates or failed transactions takes up precious time — and may distract customer service staff from more important day-to-day activities. It also hinders analyzing corporate data, obscuring the genuine customer numbers and potentially distorting real growth levels.

Damage to your brand reputation may occur, especially if you end up caught in the middle of credit card fraud warnings or payment disputes between a consumer and their credit card provider. Your reputation may be harmed in other ways, too — if your business unintentionally allows one fraudster to enter the networks, other cybercriminals might follow. Plus, higher decline rates can make your transactions seem riskier to card issuers/networks, potentially leading to legitimate transactions being queried or blocked more frequently.

In the age of security breaches and hacks, data centers and credit card agencies unintentionally give hackers abundant access to credit card numbers. Typically, hackers sell a bulk list of stolen card numbers on the dark web, where a buyer — the fraudster — is lurking.

A fraudster can purchase lists of credit card numbers; the list’s resale value depreciates over time. Many cardholders and banks take preemptive measures to shut down credit cards if there is a breach, but a small, unauthorized purchase may go unnoticed.

Luckily, you can spot red flags when carding attacks occur. Here are some things to look for:

While both large and small businesses face increasing credit card fraud, SMBs are potentially more vulnerable since they often have fewer protections in place and less knowledge about current attacks, according to Brittany Allen, senior trust and safety architect at Sift. “One of the most important things you can do for your business is to implement strong, AI-powered fraud detection tools, which use machine learning to identify and block suspicious transactions,” she advised. “With the speed, sophistication, automation and scale of today’s fraud attacks, businesses won’t be able to keep up unless they have the right technology in place.”

Robust fraud prevention technologies can identify these patterns quickly, explained Allen. For example, pinpointing transactions at odd hours since bots frequently operate when human activity is low. “Other signals include a high velocity of failed transactions or unusual purchasing patterns, such as small, frequent purchases,” she said.

If you’re a small business owner, these are some of the key recommendations to mitigate the risks of credit card fraud:

Neil Cumins and Jennifer Dublino contributed to this article.