Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Learn when you should require a deposit and how to ensure upfront payment collection

When you’re an employee, you don’t have to worry about invoicing for your work. Collecting customer payments is someone else’s job, and you receive a paycheck regularly to compensate you for your work. However, small business owners don’t have this luxury. They provide the service, create professional invoices and collect payments. They often put in significant upfront work and investment, shouldering all the risk and trusting their clients will pay them.

Searching for accounting software and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Sometimes, small business owners experience nonpaying clients who refuse to compensate them for services rendered. They must decide whether to pursue the debt collection process, put in more work or walk away. To help avoid these situations, many freelancers, independent contractors and small business owners require an upfront deposit to protect their interests. We’ll examine circumstances where requiring a deposit is a good idea and share best practices for collecting upfront payments.

Businesses have different payment requirements, which may include payment in full before delivering a product or service, payment upon completion, or an upfront deposit before starting work or delivering a product.

Here are a few examples of businesses that require payment in full before you can enjoy their products or services:

Things get more complicated when you’re selling intangible goods and services. However, many service businesses don’t require upfront payments or deposits, including the following:

It makes sense for some businesses to request a deposit before performing a service or providing an item, including the following:

Your unique business, industry and circumstances will dictate whether your customers will pay upfront entirely, pay a deposit, or pay upon product delivery or service completion.

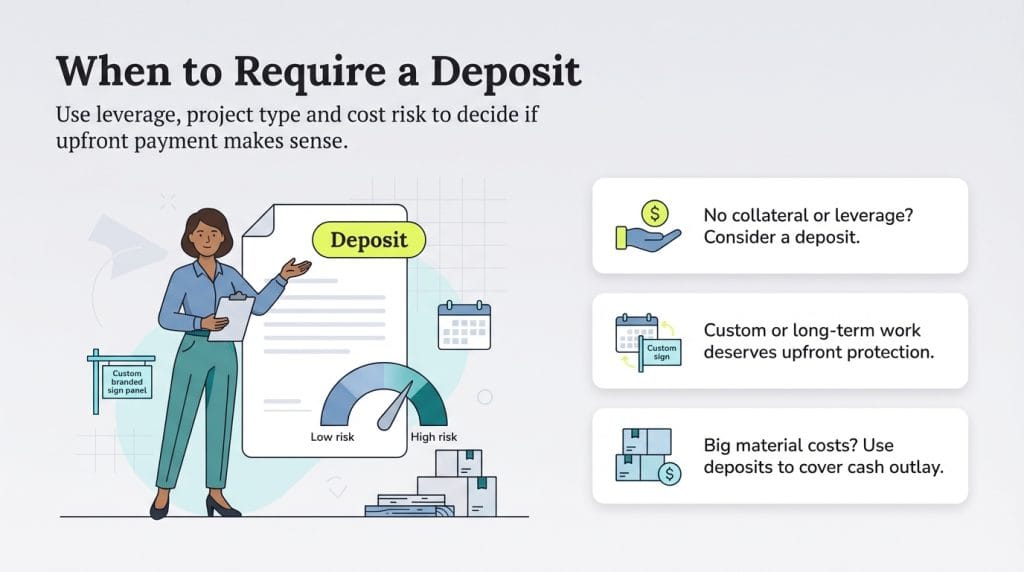

It’s up to you to decide if an upfront payment or deposit is appropriate for your business. Here are five questions to ask when determining where you fall on the payment spectrum.

Whether you have collateral will affect your decision to require a deposit or upfront payment. If you hold the customer’s property as collateral, you don’t need to charge upfront for your services or ask for a deposit.

Consider the businesses and service providers that don’t require an upfront payment. Most have recourse to ensure they’re paid. For example:

Whether you have recourse when asking for payment will help determine if you should require a deposit or upfront payment. When you have recourse, you don’t need to secure payment. For example:

However, freelancers, small business owners, and contractors dealing with intangible goods don’t always have recourse. For example:

If you don’t have significant leverage to demand the money the client owes you, you should consider getting paid upfront.

It makes sense to require a deposit or upfront payment for custom products and services.

Let’s say you have a sign shop, and a customer orders a sign with its logo to help market a retail store. This sign must be unique and customized. However, custom-made orders present the following risks to your business:

In this situation, asking for payment before investing time and resources into creating the custom offering makes sense.

If you’re working on a project that will take weeks or months to complete, it makes sense to request an initial payment so you’re not scraping by while working on it. In this kind of job, you may want to consider charging either a monthly retainer or using milestone payments.

Additionally, professionals with long-term customer contracts often ask for payment at the beginning of the month to cover the work they’ll complete. Kathy Gilchrist, accountant and CEO of CFOKathy.com, cites bookkeeping as a typical scenario where clients are charged before a professional completes their monthly work. “Some benefits of charging this way are that you don’t have to worry about not getting paid and dealing with collections,” Gilchrist noted. “And you know the amount of revenue you will have coming in regularly at the beginning of each month.”

If your business must buy expensive materials before beginning work, asking for a deposit to cover these costs is appropriate. Gilchrist cited construction companies as an example of a business that should require customer deposits to cover the materials they must purchase to do the job. “Getting a deposit gives [construction companies] the cash to pay for those materials so that they don’t have to borrow and pay interest on those materials during the time it takes to complete the job,” Gilchrist explained.

Asking for a deposit can feel awkward, but it doesn’t have to. Erik Schneider, founder of Executive Investigation and Consulting, LLC, shared the following ways to mitigate the risks of asking for a deposit and ensure everyone is on board.

Here are six additional tips to help you get favorable results when asking for upfront payment.

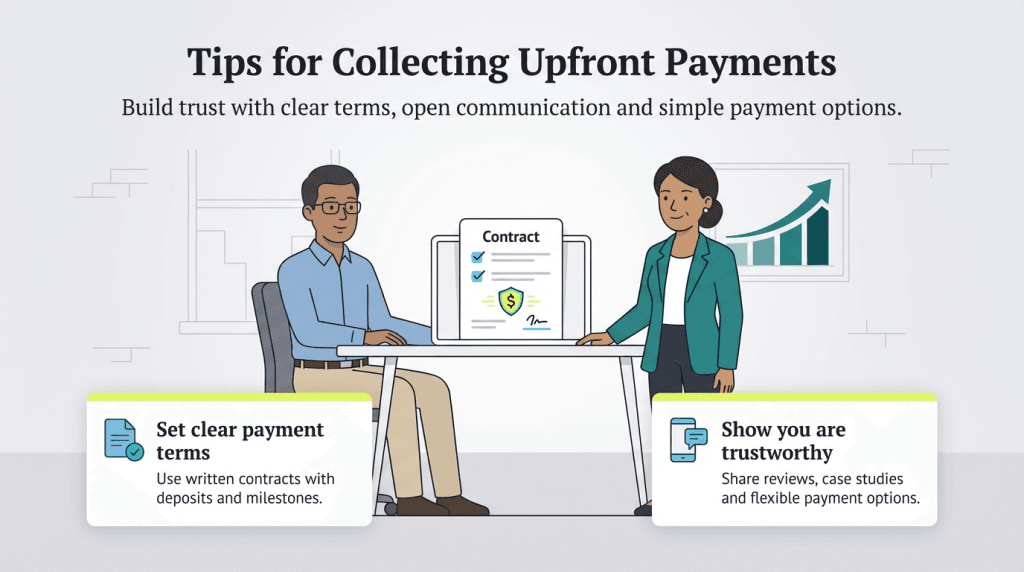

Clients don’t want to get duped out of their money. If you have an unprofessional website, no internet presence and no good customer reviews, it’s doubtful they’ll pay upfront.

To present yourself as a trustworthy vendor and brand, produce testimonials and case studies, collect referrals and bolster your web presence to create an engaging website.

People respond to positive and negative reinforcement. Understanding this, you may benefit from offering a slight discount for early payment or charging a penalty for late payment. You could also provide value-added benefits, such as priority service for clients who pay in advance.

In today’s business world, it’s not uncommon for the entirety of a relationship to take place over email. While email is often convenient, picking up the phone or meeting with a client in person can be very beneficial — particularly if you have a client who ignores you. Phone conversations and in-person meetings help establish trust and make customers feel more at ease when parting with their money.

In your initial conversations, clearly explain your payment terms to potential clients, emphasizing that adhering to these terms allows you to focus on delivering the best possible work. When clients understand and agree to your payment expectations, collecting upfront payments and deposits becomes easier.

Presenting business proposals and client contracts is an excellent idea, especially when selling a service. Proposals and contracts describe the work’s scope, costs and payment terms so there’s no confusion later. Getting the client to agree to this by signing off on the contract provides you with a legal document you can use in court if necessary.

If potential clients balk at paying 100 percent upfront, ask for a 50 percent deposit. To give new clients peace of mind, you can also arrange milestone payments triggered after completing specific deliverables.

However, including terms with a milestone or deposit payment structure is advisable. For example, you might increase the overall price to account for the added risk. Alternatively, you could say the deposit pays up until a specific point in the process, after which the remainder is due.

Asking for money upfront isn’t for everyone and doesn’t work in every situation. Here are some pros and cons to consider.

Pros of asking for a deposit or upfront payment include the following:

Cons of asking for a deposit or upfront payment include the following: