Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Excess Liability Insurance Explained

Learn how excess liability insurance works, what it covers, how it differs from umbrella policies and how to tell if your business needs it.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

A business’s general liability coverage isn’t always enough to absorb a major claim. When policy limits under your business insurance coverage are exhausted, excess liability insurance can provide another layer of protection. This guide explains how excess liability insurance works, what it covers, how it compares to umbrella insurance and how to decide whether it’s the right fit for your business.

What is excess liability insurance?

Excess liability insurance is additional business insurance that raises the coverage limits on an existing liability policy after that policy has been maxed out. In other words, it gives your business another layer of financial protection when a major claim exceeds the limits of your primary coverage.

It’s most commonly added to a general liability insurance policy, but it can also increase coverage under commercial auto liability policies and certain other business insurance policies. Think of excess insurance as a “second-in-line” policy: It doesn’t come into play until the underlying liability policy has paid up to its maximum limit.

What does excess liability insurance cover?

Excess liability insurance usually covers the same claims as the underlying policy, and those claims will vary depending on the policy type. For example, the excess liability policy for general liability will cover slip-and-fall accidents, while the excess liability policy for commercial auto insurance will cover at-fault accidents, third-party injuries or property damage.

The following are commonly covered by excess liability insurance:

Bodily injury: Medical expenses, rehabilitation costs and legal judgments for injuries to third parties.

Property damage: Costs to repair or replace damaged property belonging to others.

Personal and advertising injury: Claims involving libel, slander, invasion of privacy or false advertising.

Legal defense costs: Attorney fees, court costs and related legal expenses.

Settlement costs: Negotiated settlement amounts within policy limits.

Understanding the excess insurance meaning becomes especially important as verdicts and settlements grow larger. According to WTW’s casualty market analysis, third-party litigation funding is expected to reach $31 billion annually by 2028, fueling larger verdicts and settlements that can quickly exhaust primary liability limits.

Excess liability doesn’t typically cover the following:

Intentional acts: Deliberate wrongdoing or criminal behavior.

Workers’ compensation claims: Employee injuries (covered by separate workers’ compensation policies).

Professional liability: Errors and omissions in professional services.

Product liability: Coverage usually applies only if the underlying policy includes product liability and the claim isn’t excluded elsewhere in the policy.

Cyber liability:Data breaches and cyberattacks (requires separate coverage).

Property damage to your own assets: Coverage applies only to third-party property.

Did You Know?

Getting very high excess liability limits isn’t as straightforward as it used to be. Brown & Brown’s 2026 Market Trends Report notes that coverage above $25 million is still tight, which is pushing some businesses toward layered programs or specialty E&S carriers.

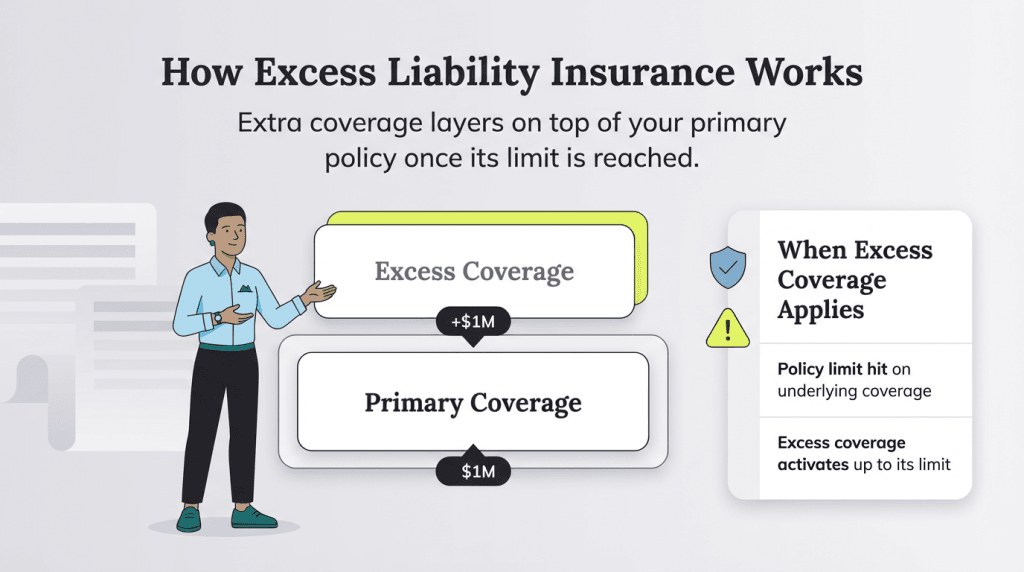

How does excess liability insurance work?

An excess liability insurance policy sits in the background until the underlying policy’s limits have been exhausted. The excess liability insurance policy will kick in once the underlying policy hits its coverage limits. Once in play, it will pay up to its policy limits.

To understand excess insurance in practice, consider this scenario: You have a general liability insurance policy with a per-occurrence limit of $1 million, plus an excess liability insurance policy providing another $1 million in coverage. Together, you have a total of $2 million in general liability protection.

If a customer who falls at your location ends up with a serious injury and sues you for $1.5 million, the general liability insurance policy would cover the first million; the excess insurance policy would handle the remaining $500,000.

However, if the customer’s claim totaled $3 million, the general liability policy would cover the first million, and the excess liability policy would cover the second million. Your business would still be responsible for the remaining million.

Do you need excess liability insurance?

Consider your company’s business insurance risks and coverage needs when deciding whether to opt for excess liability insurance. Understanding what excess insurance means for your specific situation is key — it exists to protect you in those rare but financially devastating scenarios where your general liability policy simply isn’t enough.

Ask yourself the following questions about your company’s coverage:

Asset evaluation: Does your company have significant business assets that could be at risk in a large lawsuit?

Industry risk assessment: Does your industry have higher-than-average liability exposures?

Customer interaction level: How frequently does your business interact with the public or customers?

Geographic considerations: Are you operating in states with higher litigation rates or larger jury awards?

Contractual requirements: Do your clients or contracts require specific liability coverage limits?

The bigger your business — and the more interaction it has with consumers — the more likely it is that you’ll need an excess insurance policy. Businesses with increased risk, including those that use heavy machinery and equipment, have more exposure and should carry larger liability limits.

Tip

If you have more than one liability policy, including general liability, employer's liability, and commercial auto, you may opt for an umbrella policy instead of an excess liability policy. In many cases, one umbrella policy can extend coverage across multiple underlying policies, which may make it a more cost-effective option.

What does excess liability insurance cost?

Excess liability insurance costs vary widely because policy prices depend on several factors. While rates differ by business type, size and risk profile, the premium you pay ultimately reflects how much exposure an insurer believes your business carries. Some of the biggest pricing factors include the following:

Coverage limits: The more coverage you buy, the more you’ll usually pay.

Industry type: Businesses in high-risk industries often pay more for excess coverage.

Company size and revenue: Larger companies generally face higher premiums.

Claims history: A history of claims can drive costs up.

Geographic location: In some states, litigation costs — and insurance premiums — tend to run higher.

Underlying policy limits: Higher underlying limits can sometimes reduce excess coverage costs.

Risk management practices: Strong safety programs and loss-prevention efforts may help lower premiums.

Cost-effectiveness evaluation

When evaluating excess liability coverage, consider the following:

Asset protection ratio: Coverage may need to equal or exceed your company’s net worth, depending on your risk exposure.

Revenue multiple: Some risk professionals suggest using annual revenue as one reference point when evaluating coverage needs.

Industry benchmarks: Compare your coverage to similar businesses in your sector.

Total cost of risk: Factor in potential out-of-pocket expenses for uninsured claims.

Excess liability vs. umbrella insurance

Commercial umbrella insurance policies and excess liability insurance policies both add liability coverage to specific policies, but there’s a key difference. An umbrella policy usually provides coverage for more than one underlying policy. An excess liability policy is meant to extend only one underlying policy, usually general liability, but it may also cover commercial auto.

Feature

Excess Liability

Umbrella Insurance

Coverage scope

Single underlying policy

Multiple underlying policies

Policy breadth

Follows form of underlying policy

May provide broader coverage

Cost

Often costs less for comparable limits

May cost more but can provide broader protection

Flexibility

Limited to one policy type

Covers various liability exposures

Claims handling

Often simpler when tied to one underlying policy

May involve broader claims coordination

Coverage gaps

Typically follows the underlying policy’s terms

May provide broader gap protection, depending on the policy

Minimum underlying limits

Varies by carrier

Typically requires higher underlying limits

When to choose excess liability

Single high-exposure area: Your business has one primary liability concern.

Cost sensitivity: Budget constraints may favor the lower-cost option.

Simple operations: Limited liability exposures across business activities.

Carrier relationships: Strong relationship with your current liability insurer.

When to choose umbrella coverage

Multiple liability exposures: Business operations involve various liability risks.

Comprehensive protection: Your business needs broader coverage across multiple liability policies.

Gap coverage needs: Depending on the policy terms, umbrella coverage may help fill certain coverage gaps beyond the underlying policy.

Multi-policy coordination: You prefer broader coverage that may extend across multiple underlying policies.

Generally speaking, both umbrella and excess liability insurance policies typically maintain the underlying insurance policies’ terms and conditions, including many of the underlying policy’s exclusions.

Kimberlee Leonard is an insurance expert who guides business owners through the complicated world of business insurance. A former State Farm agency owner herself, Leonard started her decades-long career as a financial consultant advising on investment strategies before switching her focus to insurance and risk mitigation for businesses.

At business.com, Leonard covers topics related to business insurance, such as workers' compensation rates, professional negligence, insurance riders, hold harmless agreements and more.

Leonard has developed insurance primers on everything from small business insurance costs to specific policies, such as excess liability insurance. She has also reviewed business software tools, analyzed employee retirement plan providers and continues to share insights on financial topics as they relate to business. Leonard's work has been published in Forbes, U.S. News and World Report, Fortune, Newsweek and other respected outlets.