Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

This payroll deductions calculator can help employers and employees determine how much their take-home pay should be.

Whether you’re an employer running payroll or a W-2 employee trying to understand where your paycheck is going, it’s important to know which federal, state and benefits-related deductions come out of each pay period. Understanding these deductions ahead of time can help you plan your personal or business finances more effectively and build a budget that accounts for any tax obligations you may owe.

You can use our payroll deductions calculator to estimate accurate take-home pay for you or your employees. With this tool, you’ll get a clear snapshot of your financial picture and make sure your payroll deductions line up with current regulations and expectations.

When using the payroll deductions calculator, it’s helpful to understand the following terms. These definitions explain how each input affects your estimated take-home pay.

This is the total amount you’ve earned from the start of the calendar year up to your most recent paycheck. YTD earnings help determine whether you’re approaching annual tax or benefit limits.

This is the tax category you choose when you file your return, such as single, married filing jointly or head of household. Your filing status directly affects how much federal tax is withheld from each paycheck.

This refers to how often you’re paid, such as weekly, biweekly or monthly. Your pay period determines how your annual salary is divided across individual paychecks.

This is a federal tax credit available for each qualifying child under 17. For 2025, the credit is worth up to $2,200 per child and can reduce your federal tax withholding.

This is a tax credit for dependents who don’t qualify for the child tax credit; it’s worth up to $500 per eligible dependent.

This indicates whether you work multiple jobs or if your spouse is also employed. These situations can increase your combined income and result in higher federal withholding.

This includes earnings outside your primary employment, such as freelance income, interest, dividends, rental income or investment gains. Additional income may increase your tax liability.

These are non-tax deductions taken from your paycheck, such as union dues, disability insurance premiums or certain health benefits.

This is your total income before any deductions or taxes are taken out. Gross pay includes wages, salaries, employee bonuses and overtime.

This is the amount you contribute to employer-sponsored retirement plans before taxes. Based on the most recently published IRS limits (for the 2025 tax year), employees under age 50 can contribute up to $23,500, while those age 50 and older can contribute an additional $7,500 in catch-up contributions (or up to $11,250 if ages 60-63 and their plan permits). The IRS updates these limits annually for inflation, so future contribution ceilings may rise once new figures are released.

This is the portion of your health insurance premiums that you pay through payroll. Premiums may reduce your taxable income if they’re deducted pre-tax.

These are taxes withheld by your state or local government. Nine states — Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington and Wyoming — don’t tax wage income, while other states have rates ranging from 2.5 percent to 13.3 percent. This matters if you work in one state and live in another or employ workers across multiple states.

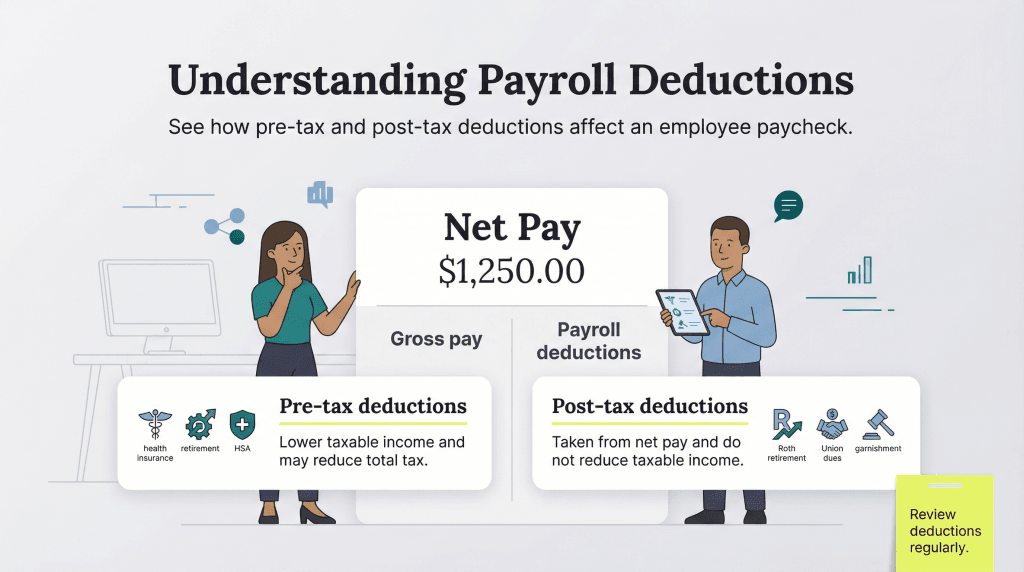

These are deductions taken before tax calculations, such as contributions to health savings accounts (HSAs), flexible spending accounts (FSAs) or commuter benefit programs. Pre-tax deductions lower your taxable income.

These are deductions taken after your taxes are calculated, such as Roth retirement contributions, charitable giving programs or certain insurance premiums.

These are expense reimbursements added to your paycheck after taxes, such as mileage or travel reimbursements.

This is the federal payroll tax that funds Social Security. Employees and employers each pay 6.2 percent on wages up to the annual Social Security wage base. According to the most recently published limit (for the 2025 tax year), that cap is $176,100. The Social Security Administration updates this wage base every year, so future limits will increase once new figures are released.

This federal payroll tax funds Medicare. Employees and employers each pay 1.45 percent on all wages. High earners pay an additional 0.9 percent on wages above $200,000 for single filers or $250,000 for married couples filing jointly.

This is the amount of federal income tax withheld from your paycheck based on your filing status, income, dependents and other adjustments.

Payroll deductions are the amounts taken out of an employee’s gross pay before they receive their final take-home paycheck. These deductions cover taxes, employee benefits and other required withholdings that help determine an employee’s net pay.

Typical payroll deductions include federal and state income taxes, Social Security and Medicare taxes (FICA), retirement plan contributions, health insurance premiums and other employee-selected benefits. Employers also account for current IRS tax brackets and standard deductions when calculating how much to withhold from each paycheck.

Gross payroll is the total amount an employee earns before any deductions are taken out — essentially their full employee compensation for the pay period. Net payroll, often called take-home pay, is the amount the employee actually receives in their paycheck after all taxes, benefits and other withholdings have been subtracted from gross pay.

The way you calculate gross payroll depends on whether the employee is salaried or hourly:

Once you have the gross payroll amount, you can calculate net payroll by following these steps:

Modern payroll software simplifies the complicated process of managing payroll deductions by automating calculations and staying up to date with changing tax rules. These systems automatically apply the correct federal, state and local tax rates, manage retirement plan contributions based on employee elections and calculate benefit deductions accurately each pay period.

Payroll platforms stay current with the most recently published tax tables and IRS updates — including changes to tax brackets, standard deductions and contribution limits — which helps employers remain compliant without having to track each update manually. This automation reduces errors, saves time and produces clear digital pay stubs that show every deduction in detail.

Many of the best online payroll software tools also integrate with time-tracking systems and benefits administration platforms, creating a seamless workflow that minimizes manual data entry and supports accurate, on-time payroll processing.