Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Learn what a 7702 account really is, how it differs from retirement accounts and whether it's right for your financial goals.

You’ve been responsible with your money by investing in your 401(k) retirement plan at work and perhaps even opening an individual retirement account (IRA) to boost your retirement savings. Then a financial agent approaches you about a “7702 plan” that promises high returns, minimal risk and penalty-free withdrawals. If it sounds too good to be true, that’s because the marketing often obscures what a 7702 plan actually is. The term “7702 plan” itself is misleading — it’s not a type of account but rather refers to a section of the tax code that governs cash value life insurance policies. This confusion is often intentional, as agents use the technical-sounding name to make whole life insurance seem like a revolutionary investment product.

The reality is that 7702 plans are simply cash-value life insurance policies dressed up in financial jargon, and they come with significant limitations that agents don’t always fully explain. While these policies can offer tax advantages and liquidity features, they also carry high fees, complex structures and opportunity costs that may not align with your financial goals. Understanding the difference between the marketing hype and the actual product is crucial before making any decisions. This guide will cut through the confusion and give you the complete picture of what 7702 plans really are and how they stack up against traditional retirement savings options.

A 7702 plan, also called a Section 7702 plan or 7702 account, is a cash-value life insurance policy that meets the requirements of Section 7702 of the U.S. tax code — specifically, the definition tests that distinguish life insurance from investment products for tax purposes. These policies may be universal, variable universal, indexed universal or whole life insurance. The term “7702 plan” refers to any permanent life insurance policy with a cash value component that complies with Section 7702’s requirements.

Notably, a 7702 plan isn’t a qualified retirement plan, though many people who see the term “7702 plan” mistake it for this special type of tax-friendly benefit. Additionally, a 7702 plan’s value depends on the type of life insurance policy you choose, your premium costs, policy performance, fees and surrender charges, all of which can significantly impact returns.

Cash-value life insurance policies accumulate value over time beyond the death benefit. The cash value grows on a tax-deferred basis and can be accessed during the policyholder’s lifetime through withdrawals (up to the amount of premiums paid) or policy loans, which generally don’t create taxable events as long as the policy remains in force. However, accessing cash value through loans reduces the death benefit, and if the policy lapses with outstanding loans, it could create a significant taxable event. These policies are primarily life insurance products designed to provide death benefits to beneficiaries, not retirement planning vehicles.

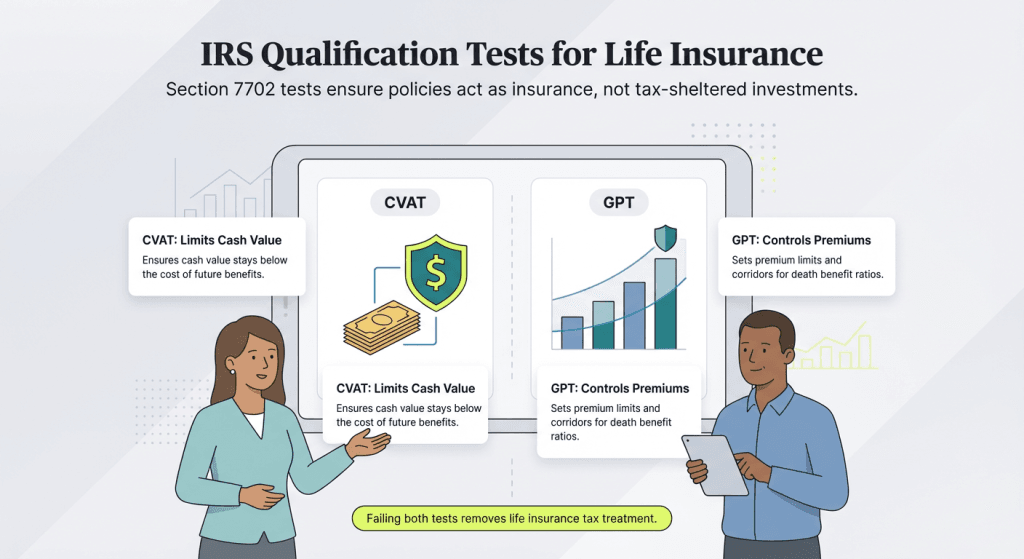

To qualify for tax-advantaged treatment under Section 7702, a life insurance policy must pass one of two actuarial tests established by the IRS. These tests ensure that policies function as legitimate life insurance rather than investment products structured to avoid taxes.

The Cash Value Accumulation Test (CVAT) ensures that the cash surrender value of a life insurance contract cannot exceed the net single premium that would be actuarially required to fund all future benefits under the policy. In simpler terms, the amount of money a policyholder could receive by canceling the policy cannot be greater than the calculated cost to purchase those same benefits with a single upfront payment.

For example, if you have a $200,000 life insurance policy with a $20,000 cash value, the actuarially determined net single premium to fund all future benefits must be more than $20,000. If it would only cost $18,000 to fund all future benefits upfront, your policy will not pass the CVAT. Policies that typically use the CVAT include whole life insurance, which accumulates cash value steadily over time.

The Guideline Premium and Corridor Test (GPT) is an alternative qualification test that focuses on premium limitations and maintaining required ratios between the death benefit and cash value (known as “corridors”). Unlike CVAT, which limits cash value accumulation relative to benefits, GPT allows policyholders to maximize cash accumulation within defined premium and corridor limits.

The GPT establishes limits on how much can be paid into the policy as premiums while maintaining the minimum death benefit-to-cash value ratios required to qualify as life insurance. This test is more complex than CVAT but allows for greater flexibility in premium payments and cash value accumulation.

If a life insurance policy fails to pass either the CVAT or GPT, it loses its tax treatment as life insurance entirely, and all income from the contract becomes subject to ordinary income tax under Section 7702(g). Note that this is different from Modified Endowment Contract (MEC) status, which occurs when a policy passes Section 7702 tests but exceeds premium limits under the separate 7-pay test — MECs retain some tax advantages but lose others. In practice, insurance companies design their products to comply with these tests, so most policyholders don’t need to worry about these technical requirements.

7702-compliant policies offer several potential tax advantages but also come with significant risks that consumers should understand.

There’s nothing wrong with opening a cash-value life insurance policy, but it won’t perform the same as a 401(k) or an IRA, so it isn’t a substitute. Here’s how 7702-compliant policies compare to traditional retirement plans:

7702 plan | 401(k) | IRA | |

|---|---|---|---|

Are investments tax-deductible? | No, premiums are not tax-deductible. | No, but the contributions are made with pre-tax dollars. | Yes |

Will I pay a penalty if I withdraw early? | Yes, but you can withdraw cash up to your basis. | Yes | Yes |

Does the FDIC cover this contract? | No | Yes (limited) | Yes (limited) |

Will my retirement income be taxed? | No | Yes | Yes |

The key differences between 7702-compliant policies and retirement plans extend beyond tax treatment. Life insurance premiums are considered personal expenses and are not tax-deductible, while retirement plan contributions often provide immediate tax benefits.

Regarding penalties, retirement accounts typically impose a 10 percent penalty plus taxes for early withdrawals before age 59 and a half. With cash-value life insurance, you can withdraw up to your basis (the amount of premiums paid) without penalty, but withdrawals beyond basis are taxable and may trigger additional consequences if the policy lapses.

Retirement accounts held at banks may have FDIC protection for cash deposits up to $250,000, while investment accounts typically have SIPC protection. Cash-value life insurance policies aren’t FDIC-protected since they’re insurance contracts, not bank deposits. Instead, they’re backed by the insurance company’s financial strength and, in case of insurer insolvency, by state guaranty associations that provide limited coverage (typically $100,000-$300,000 depending on the state).

There are cost considerations as well. “Unlike traditional retirement accounts like 401(k)s or IRAs, [7702 plans] come with higher fees and unpredictable policy costs,” said Alex Schlesinger, founder and CEO of the insurance firm Active Mutual.

Section 7702 is a tax code provision that defines what qualifies as life insurance for tax purposes — it’s not an actual insurance plan, product type or IRS-designated retirement plan. The term “7702 plan” is purely a marketing creation used by insurance agents and companies to promote cash-value life insurance policies by making them sound like official government-sanctioned retirement vehicles.

This marketing terminology is intentionally misleading. By using the technical-sounding “7702 plan” instead of saying “whole life insurance” or “universal life insurance,” agents create the impression that they’re offering a special, little-known financial product rather than traditional life insurance. The numeric designation mimics legitimate retirement plan names like “401(k)” or “403(b),” leading consumers to believe they’re getting access to a similar type of qualified retirement plan with IRS backing.

“7702 plans are primarily a life insurance product, so while they are touted as providing retirement planning benefits, that is not their original intent,” explained Crystal Stranger, CEO of Optic Tax.

Beware of agents who refer to these policies as “tax-free retirement accounts” or “private pensions,” or use phrases like “the IRS doesn’t want you to know about this.” These are red flags that the salesperson is deliberately obscuring the fact that you’re purchasing life insurance, not a retirement plan. The 7702 code was written because many people were using life insurance policies as investments to get generous tax breaks, but these policies are designed to serve as death benefits to replace your income for beneficiaries — not as retirement funds. If an insurance agent tries to tell you differently or avoids clearly stating that you’re buying life insurance, approach their pitch with significant skepticism.

Section 7702 underwent significant legislative changes through the SECURE Act of 2019, which took effect in 2021, to address prolonged low-interest-rate environments. The changes introduced a new “Insurance Interest Rate” system that dynamically adjusts the interest rate assumptions used in Section 7702 calculations based on applicable federal interest rates rather than static minimums.

For contracts issued in 2021, the Insurance Interest Rate was set at 2 percent, significantly lower than the previous Section 7702 valuation interest rate of approximately 4 percent that was in effect for 2020. This change allows insurance companies to use lower interest rate assumptions when designing policies, which means policyholders may need to pay higher premiums for the same death benefit, but policies can accommodate larger premium payments without violating Section 7702 tests.

The new system operates on “Adjustment Years” — years following changes in the valuation interest rate. Once set in an Adjustment Year, the Insurance Interest Rate remains fixed and typically stays in effect for several years, providing stability for insurers and policyholders. The legislative changes were designed to help consumers maintain access to permanent life insurance and help insurance companies operate sustainably in low-interest-rate environments.

Understanding the distinction between Section 7702 as a tax code and the marketed “7702 plans” is crucial for informed decision-making. Many people are misled into believing they’re purchasing a retirement plan when they’re actually buying life insurance with cash value features. This confusion can lead to inappropriate financial planning decisions and unrealistic expectations about policy performance.

The regulatory changes implemented in 2021 further underscore the importance of understanding these policies’ complexity. With changing interest rate assumptions and evolving tax implications, you should work with qualified financial professionals who can explain both the benefits and limitations of cash-value life insurance in the context of your overall financial strategy.

Danielle Fallon-O’Leary and Sean Peek contributed to this article. Source interviews were conducted for a previous version of this article.