Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Your customers need the convenience of multiple payment options.

A surprising number of small businesses still operate on a cash-only basis. Although cash-only businesses save money on credit card processing fees, the benefits of accepting multiple payment forms far outweigh the disadvantages.

If your business accepts cash payments only, you may alienate consumers, reduce sales revenue and create a poor customer experience. When customers’ needs aren’t met, they will become dissatisfied and go to a competitor — perhaps for good. We’ll explain why the cash-only model doesn’t work for small businesses and share alternative payment acceptance options that can help fuel business growth

An estimated 84 percent of payments made in the U.S. are cashless, according to the Federal Reserve’s 2024 Diary of Consumer Payment Choice. Consumers between the ages of 25 and 54 use cash for only 12 percent of transactions, 18- to 24-year-olds opt for cash 14 percent of the time, and those 55 and older use cash 22 percent of the time.

Clearly, U.S. shoppers are increasingly choosing cashless options, including debit and credit cards, mobile payment apps and Automated Clearing House (ACH) transactions. If your business accepts only cash, you’re limiting your reach.

Here are eight reasons why cash-only isn’t a good formula for growth.

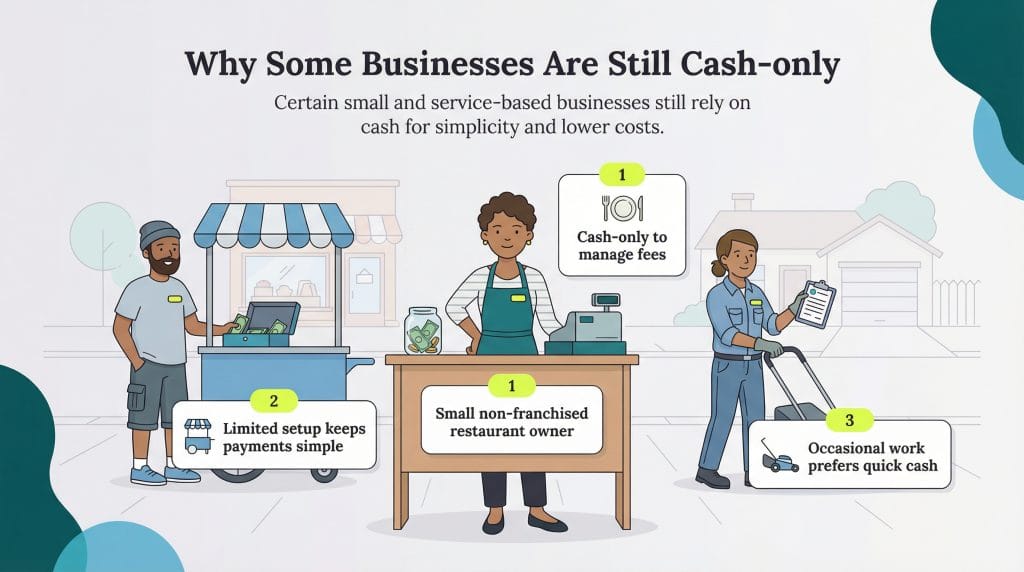

Say Beth owns a boutique, and shoppers fill her store every day. But time and again, when they get to the cash register and see her “cash only” sign, they sigh, put their items back and walk out of the store. She’s missing out on untold sales opportunities.

Cash is no longer king. There’s a distinct preference for using digital payment methods, which increases with income. Whether your customers don’t carry much cash or prefer not to use it, accepting credit cards and other digital payment forms will help you increase sales and accommodate customers’ payment preferences.

For years, New York City-based Joe Coffee prided itself on being cash-only; it was part of the shop’s old-school charm. However, the establishment started seeing negative reviews on Yelp, with customers commenting about the inconvenience of not being able to use credit cards. The brand changed its tune and began accepting card and digital payments, and its positive customer reviews soon skyrocketed. The coffee shop learned that it could preserve its old-fashioned charm without sticking to old-fashioned business practices.

In addition to credit cards and NFC mobile payments, many customers have adopted mobile wallets, such as Apple Pay, and expect multiple payment options. If you’re still using a cash register and accepting only cash, your customers will likely move on to your more modern competitors. [Read related article: Cash Register Buying Guide: POS vs. Cash Registers vs. Tablet mPOS]

Research shows that consumers spend more when using a card to pay for a purchase than when using cash, including studies from the University of Adelaide and the MIT Sloan School of Management.

If your customers can only spend the cash they carry, their purchasing power is severely limited. In contrast, opening up your payment options helps support more significant transactions and impulse purchases.

Many of us have become frustrated when the customer ahead of us in the checkout line is painstakingly counting out bills and coins to pay for their transaction. There’s no denying that credit cards and mobile payments are fast and easy. With just a swipe, scan or tap, you’re finished, so the salesperson is freed up to help the next customer.

Cash-only businesses have less of a paper trail than businesses that accept credit cards and electronic payments. Because there isn’t much paperwork to back up expenses and income, the IRS may think a cash-only business is skirting tax obligations. This makes cash-only businesses more likely to undergo an audit to prove their claims.

If you’re in the service industry and wait for clients to mail you checks for payment, you’ll wait much longer than you would if you accepted credit cards online. Customers like payments they can make with a few clicks of a mouse. You’ll receive your payments more quickly via an online system than you would by creating invoices, waiting for checks, following up on payments and possibly re-invoicing.

Customers feel some assurance when using cards because most debit and credit cards have built-in consumer protections. If customers trust their transactions, they are more willing to spend money. However, cash doesn’t provide that comfort.

Additionally, unscrupulous employees may be tempted to steal from your cash register or pocket some cash transactions. And thieves who know you’re a cash-only business may target you.

For many consumers, reward points are reason enough to make significant purchases using credit cards. No matter what kind of customer loyalty program or promotion you offer, you can’t compete with credit cards’ cash-back programs and rewards points. Your customers will likely go somewhere else to earn their rewards.

Although a cash-only payment model isn’t ideal for most businesses, some still use this method. These types of businesses are the most likely to use a cash-only model:

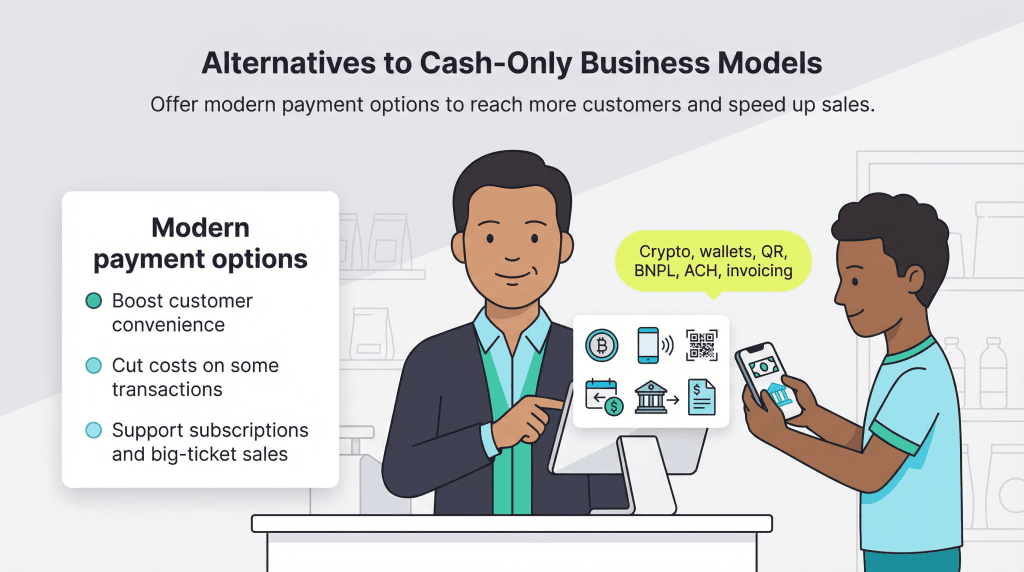

In addition to credit and debit cards, businesses may consider the following alternatives to cash-only models.

Cryptocurrencies such as Bitcoin and Ether are electronic monetary tokens. Transactions in these cryptocurrencies are recorded and held on decentralized servers called blockchains. A small but enthusiastic user base believes cryptocurrencies will eventually replace traditional currencies. The transaction fees are lower, there’s no need for Payment Card Industry compliance, and customers can’t initiate charge-backs.

Although cryptocurrency transactions can take time to process, this issue is improving. According to Ian Major, co-founder of Bitcoin infrastructure company Joltz, some processors now facilitate near-instant payments through technologies like the Lightning Network. [Read related article: Should Your Restaurant Accept Bitcoin?]

Major supports businesses offering crypto as a payment option. He cited research from Bakkt, a crypto platform that’s part of the same group that owns the New York Stock Exchange. That study found that people who use crypto tend to be younger and have higher-than-average incomes.

“These consumers are also highly motivated and willing to change behavior for businesses that embrace Bitcoin and crypto,” Major said. “For example, according to our analysis, over 90 percent of these consumers would be ‘very likely’ to switch allegiance to a business offering Bitcoin or cryptocurrency loyalty rewards, which could serve as a powerful new way for SMBs [small and midsize businesses] to steal share from bigger competitors.”

Many business owners worry about the volatility of cryptocurrency’s value. However, these concerns are being addressed. “There are services now that automatically convert crypto payments into the fiat currency of the business’s choosing,” Major noted. “We will soon see an increasing number of payment solutions for stablecoins, which provide the benefits of cryptocurrencies while tracking the value of a familiar unit of account, such as the USD.”

Digital wallets are a digital payment method that consumers embrace for their convenience and ease of use. These smartphone and smartwatch apps store credit and debit card numbers, membership and loyalty cards, event tickets, discount coupons and more. Popular digital wallets include Google Pay, Apple Pay and Samsung Pay.

Digital wallets use contactless payments; the consumer holds their smartphone or smartwatch to the terminal to initiate the payment process. According to CapitalOne Shopping, 4.3 billion people use digital wallets worldwide.

Smartphone-based QR code payments are another easy and convenient payment method for businesses and customers. A payment app creates a QR code based on a customer’s order. When the customer is ready to pay, they scan the QR code and enter the payment details.

Buy now, pay later (BNPL) services allow customers to pay for goods and services in interest-free installments. The business receives the total amount for the transaction instantly, minus the BNPL provider’s fee. BNPL started online, but many payment gateways now allow customers to select this option in physical stores.

The ACH network allows funds to be transferred from one person or business to another via the banking system. Many businesses pay their employees via direct deposit through this network.

ACH payments offer lower transaction fees for businesses and a reduced risk of bounced checks. The ACH system also allows for recurring payments, making it ideal for subscription-based services or regular invoice payments. Downsides include slower processing times and a limit on the amount that can be sent through the system.

For decades, auto dealers and furniture stores have provided consumers and business decision-makers with access to financing. Without it, many of these big-ticket transactions wouldn’t be possible.

With in-store financing, you must submit each customer’s application to a lender; there’s no guarantee it will be accepted. If it is, the customer may take out an interest-bearing loan on your products or services. In this arrangement, the retailer often receives the total price of the goods or services plus a commission from the lender.

Businesses can also offer interest-free credit to customers. In these cases, the retailer usually receives less than the original product or service price because the lender absorbs the interest cost. Instead of earning a commission, the retailer might receive a discounted payout from the lender.

Many of the best accounting software packages now include links at the bottom of their invoices that take customers to a payment gateway.

You may not be able to take credit or debit cards in person, but your accounting platform will process your clients’ remittance for you, often by working with a third-party gateway. Digital invoicing is a great way to speed up customer payments, particularly for business-to-business transactions.

John Gidla, head of global regulatory research & analysis at Vixio, noted that more businesses are transitioning from cash-only models to digital payment options. “Interest in innovative payment options is rising,” Gidla said. “Alternative payment methods, like open banking and account-to-account transfers, will potentially provide new ways to accept payments, which could provide another solution in addition to the typical merchant process.”

Accepting various payment options has numerous upsides, including enhancing business transparency and transaction traceability. “Unlike cash, which can be harder to monitor, electronic payments provide a clear record, making financial management more efficient,” Gidla noted. Additionally, customer convenience is a huge selling point. “As society continues to embrace cashless transactions, small businesses will find it easier to attract and retain customers who prefer seamless, digital payment experiences,” Gidla added.

Still, transitioning out of a cash-only model does present some challenges. “Regulators remain cautious about eliminating cash entirely, recognizing that certain populations, particularly in rural areas, still rely on it,” Gidla said. “Additionally, small businesses transitioning to cashless systems may face merchant acquirer fees, but these costs are often offset by the increased customer engagement and convenience that digital payment methods provide.”

Many small businesses pride themselves on their cash-only model. However, what worked in the past doesn’t necessarily work now that technology has all but obliterated cash. It’s challenging to grow your business if you operate on a cash-only basis. Credit card processing boosts your bottom line, and the additional revenue more than pays for the upgrade cost.

Jennifer Dublino contributed to the reporting and writing in this article. Source interviews were conducted for a previous version of this article.