Hiring your first employee is one of the most significant milestones in the life of a small business. It’s also one of the most consequential from an insurance perspective. The moment you have someone on your payroll, your legal obligations expand, your liability exposure increases and your insurance program needs to reflect a fundamentally different risk profile than what a solo operation requires.

Some of the insurance changes triggered by hiring an employee are legally mandated — you’re required by law to carry certain coverages once you have workers. Others aren’t legally required but are practically essential because the financial exposure of operating without them is too significant to absorb. And some become increasingly important as your team grows beyond the first few hires.

This guide walks through every insurance consideration that comes with hiring, from the non-negotiable legal requirements to the coverages that become important as your team expands. Whether you’re making your first hire or your 15th, understanding these insurance obligations and exposures before they become problems is far less expensive than discovering them after the fact.

Insurance requirements and considerations when hiring employees

Below are the insurance requirements for hiring employees, along with other policies you should consider as your team expands.

Workers’ compensation insurance

Workers’ compensation is the most immediate and most important employer insurance requirement triggered by hiring employees. It is legally required in nearly every state, and the penalties for non-compliance — fines, criminal charges, personal liability for the business owner — are severe enough that this should be at the top of your insurance to-do list before your first employee starts work.

Workers’ compensation covers medical expenses, rehabilitation costs, and a portion of lost wages for employees who are injured or become ill as a direct result of their job. If an employee breaks their arm falling from a ladder at work, develops carpal tunnel syndrome from repetitive tasks or is exposed to a harmful substance in the course of their duties, workers’ comp covers their treatment and compensates them for the income they lose during recovery. In the most tragic cases, it also provides death benefits to the families of employees killed in workplace accidents.

The coverage protects employers as well. In most states, workers’ compensation operates as the exclusive remedy for workplace injuries. This means an employee who receives workers’ comp benefits generally cannot sue the employer for the same injury. Without this protection, a single workplace injury lawsuit could threaten a small business’s financial viability.

The specific rules regarding workers’ comp insurance vary by state. Some states require coverage with your very first hire. Others set the threshold at two, three, four or five employees. Certain industries face stricter requirements regardless of headcount — construction is the most common example, where many states require workers’ compensation coverage even for sole proprietors and business owners with no employees. A small number of states (Ohio, North Dakota, Washington and Wyoming) operate monopolistic state funds where coverage must be purchased from the state rather than a private insurer.

Check your state’s requirements through your state’s department of labor or workers’ compensation board before your first employee’s start date, and have coverage in place before they begin working. Not after their first week. Not after the first payroll runs. Before.

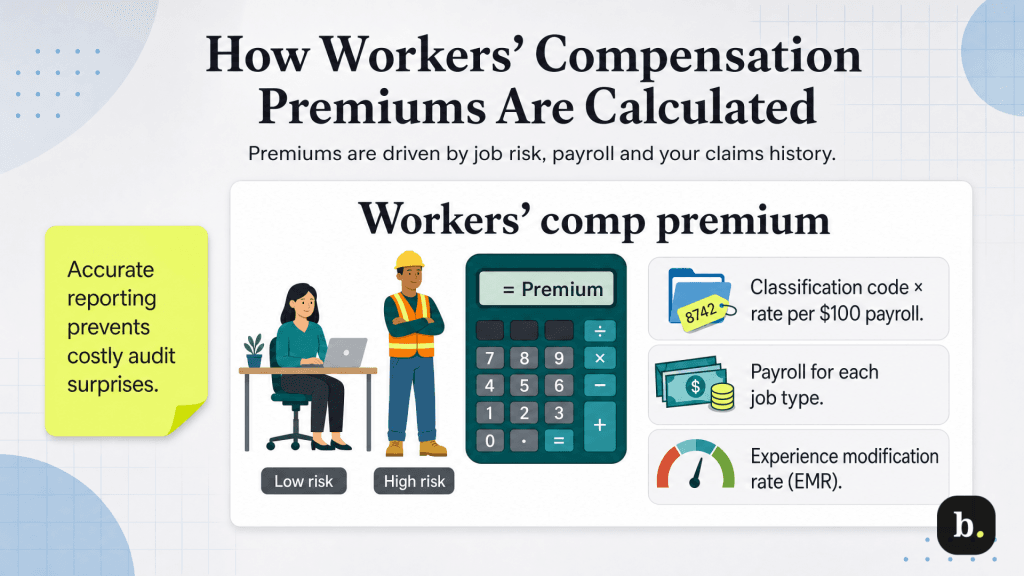

How workers’ compensation premiums are calculated

Understanding how workers’ comp premiums are calculated helps you budget accurately and identify opportunities to reduce costs over time. The premium is determined by three primary factors: employee classification codes, payroll and your experience modification rate.

- Classification codes categorize employees by the type of work they perform. Each classification carries a specific rate per $100 of payroll, reflecting the relative risk of the work. An office employee classified under a clerical code might carry a rate of $0.20 per $100 of payroll, while a construction laborer might carry a rate of $15.00 or more per $100 of payroll. The difference reflects the dramatically different injury risk between sitting at a desk and working at a construction site.

- Payroll is the base exposure measure. Your premium for each classification is calculated by multiplying the rate by the payroll for employees in that classification, then dividing by 100. If you have $200,000 in payroll for employees classified at a rate of $2.50 per $100, the base premium for that classification is $5,000.

- The experience modification rate (EMR) is a multiplier that adjusts your base premium based on your business’s claims history relative to other businesses in your industry and state. An EMR of 1.0 means your claims history is average for your industry. Below 1.0 means better than average — your premium is reduced. Above 1.0 means worse than average — your premium is increased. New businesses without claims history typically start at or near 1.0 and see their EMR adjust as they develop their own track record over a rolling three-year period.

Accurate employee classification and payroll reporting are essential. Workers’ comp policies are audited at the end of the policy period, and discrepancies between what you reported and what actually occurred — underreported payroll, misclassified employees — result in audit adjustments that can produce significant additional charges. If you’re unsure how to classify an employee, your insurance agent or your state’s workers’ compensation board can help.

>> Read Related Article: How Do Workers’ Compensation Rates Work?

Unemployment insurance

Federal and state unemployment insurance obligations are triggered when you hire employees. Unlike workers’ compensation, unemployment insurance isn’t a policy you purchase from an insurance carrier. It’s a payroll tax obligation that funds the unemployment benefits system, providing temporary income to workers who lose their jobs through no fault of their own.

At the federal level, the Federal Unemployment Tax Act (FUTA) imposes a tax of 6.0 percent on the first $7,000 of each employee’s annual wages. However, employers who pay their state unemployment taxes on time receive a credit of up to 5.4 percent, reducing the effective FUTA rate to 0.6 percent in most cases. At the state level, the State Unemployment Tax Act (SUTA) governs each state’s unemployment tax program, with its own rates and taxable wage bases. State rates are experience-rated, meaning your rate is adjusted over time based on the number of former employees who file unemployment claims against your account — more claims lead to higher rates.

You’ll need to register with your state’s unemployment agency when you hire your first employee. High-quality payroll providers typically handle the ongoing tax calculation, deposits and quarterly reporting automatically as part of their service.

State-mandated disability insurance

If you operate in California, Hawaii, New Jersey, New York, Rhode Island or Puerto Rico, you are required to provide short-term disability insurance to your employees. This coverage provides partial wage replacement for employees who are unable to work due to a non-work-related illness or injury — a condition that workers’ compensation wouldn’t cover because it didn’t arise from the job.

The funding mechanism varies by state. Some states fund disability insurance entirely through employee payroll deductions. Others require employer contributions. And some allow flexibility in the arrangement. If you operate in one of these states, confirm your specific obligations through the state’s disability insurance program or your payroll provider.

Additionally, several states have implemented or are implementing paid family and medical leave (PFML) programs that may impose additional employer obligations beyond short-term disability. These programs are expanding across the country, with requirements varying significantly from state to state. Stay current on developments in every state where you have employees.

Health insurance

Under the Affordable Care Act, applicable large employers — defined as businesses with 50 or more full-time equivalent employees — are required to offer health insurance to full-time employees or face potential penalties under the employer shared responsibility provisions. Businesses with fewer than 50 full-time equivalents are not federally required to offer health insurance.

However, many small businesses below the 50-employee threshold choose to offer health insurance as a competitive employee benefit. In a tight labor market, health coverage can be a decisive factor in attracting and retaining qualified employees. Small businesses with fewer than 25 full-time equivalent employees may qualify for the Small Business Health Care Tax Credit, which can cover up to 50 percent of premium contributions — though eligibility requirements are specific and the credit is limited to two consecutive tax years. Employers should consult a tax advisor to determine whether they qualify.

Health insurance for small groups is purchased through the small group market, either through an insurance broker, directly from a carrier or through the Small Business Health Options Program (SHOP) marketplace. It’s subject to different rules and rating factors than the individual health insurance market. While health insurance is technically a benefits decision rather than a traditional business insurance decision, it becomes a relevant and often unavoidable consideration as soon as you begin hiring and competing for talent.

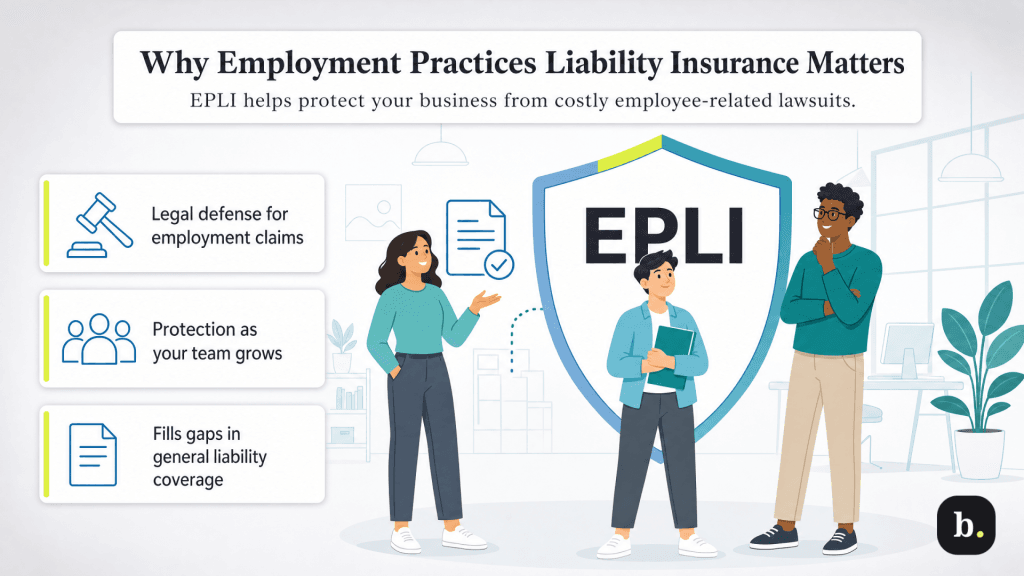

Employment practices liability insurance (EPLI)

Employment practices liability insurance (EPLI) covers claims made by employees, former employees and job applicants alleging wrongful termination, discrimination, harassment, retaliation, wage and hour violations, and other employment-related grievances. These claims are specifically excluded from general liability policies, so having general liability coverage provides no protection whatsoever against employment practices claims.

The risk of employment practices claims increases with each additional employee you hire. Even a small team creates the conditions for employment disputes — performance disagreements, termination decisions, workplace dynamics, hiring and promotion controversies. A single wrongful termination lawsuit can easily generate six-figure costs, even when the employer did nothing wrong and the claim is ultimately dismissed. The cost isn’t just the settlement or judgment — it’s the legal defense, which the employer must fund regardless of the outcome.

EPLI becomes particularly important as your business crosses certain employee thresholds where federal anti-discrimination laws take effect. Title VII of the Civil Rights Act and the Americans with Disabilities Act (ADA) apply to employers with 15 or more employees. The Age Discrimination in Employment Act (ADEA) applies to employers with 20 or more employees. State and local anti-discrimination laws may apply at even lower thresholds. Each of these laws creates additional avenues for bringing employment practices claims.

EPLI is not legally required, but it’s increasingly considered essential for any business with employees. The practical question isn’t whether you can afford the premium — it’s whether you can afford to defend an employment practices lawsuit without it. For most small businesses, the answer is no. Consider EPLI as soon as you begin hiring, even if your team is small.

Hired and non-owned auto coverage (HNOA)

If any of your employees use their personal vehicles for business purposes — driving to client meetings, making deliveries, picking up supplies, traveling between job sites, etc. — your business has an auto liability exposure that your general liability policy doesn’t cover. If an employee causes an accident while driving for work, the injured party can and likely will sue both the employee and the business.

The employee’s personal auto insurance is the first line of defense, but personal policies often have limits that are insufficient for a serious accident, and some personal policies exclude or limit coverage for business use. If the employee’s personal policy doesn’t fully cover the claim, your business is next in line — and without hired and non-owned auto (HNOA) coverage, you’d have to pay out of pocket.

Hired and non-owned auto coverage fills this gap. It provides liability protection when employees drive their personal vehicles for business purposes (non-owned auto) and when your business rents or borrows vehicles (hired auto). This coverage is relatively inexpensive and can typically be added as an insurance endorsement to your general liability policy or, if you have one, to your commercial auto policy.

Note that HNOA is a liability-only coverage — it doesn’t cover physical damage to the employee’s personal vehicle. If your business owns vehicles, you need a full commercial auto policy, which is separate from HNOA.

Key person insurance

As your team grows, you may hire individuals whose skills, client relationships, institutional knowledge or revenue contribution are critical to the business’s operations. A head of sales who manages your largest accounts. A technical lead whose expertise is central to your product. A practice director who is the face of the business to your most important clients. If one of these people were suddenly unavailable — due to death, disability or departure — the financial impact on your business could be severe.

Key person insurance is a life insurance or disability insurance policy taken out by the business on a critical employee, with the business named as the beneficiary. If the covered employee dies or becomes disabled, the policy pays the business a benefit that helps cover the financial impact: lost revenue, the cost of recruiting and training a replacement, debt obligations that may be at risk or the cost of restructuring operations to compensate for the loss.

Key person insurance is not a day-one-of-hiring consideration for most businesses. It becomes relevant when you’ve hired someone whose sudden absence would create a genuine financial hardship — not just an inconvenience, but a material threat to the business’s revenue or operational viability. The business owns the policy and pays the premiums, and the payout goes to the business, not to the employee’s family. The employee’s personal life insurance and disability insurance serve the separate purpose of protecting their family.

General liability considerations

Your general liability policy was underwritten based on your business’s risk profile at the time it was issued. Adding employees changes that profile in ways that your insurer needs to know about. More employees means more people interacting with customers, vendors and the public on your behalf, which increases the probability of a third-party bodily injury or property damage claim.

General liability is often rated in part on employee count or payroll in addition to revenue, so adding employees may affect your premium calculation. More importantly, failing to notify your insurer about material changes to your workforce could create coverage issues if a claim is filed and the insurer determines the policy was based on outdated information.

If your employees will be visiting client sites, performing work at locations you don’t control, making deliveries or operating in any capacity beyond your own premises, discuss these activities with your insurance agent. Your general liability coverage may need to be extended or supplemented to cover off-premises operations and the additional liability exposure they create.

Cyber liability considerations

Hiring employees typically means collecting and storing a significant amount of sensitive personal data. To run payroll and comply with tax obligations, you need each employee’s Social Security number, bank account information for direct deposit, home address, date of birth and tax withholding elections. If you offer health benefits, you’re handling health plan enrollment data as well. This employee data sits alongside whatever customer data your business already collects.

This data is subject to the same breach risks as any other sensitive information — hacking, ransomware, phishing attacks, accidental exposure and insider theft. If a data breach exposes your employees’ Social Security numbers or bank account details, you may face state-mandated breach notification requirements, credit monitoring obligations for affected individuals, regulatory investigations and potential lawsuits from the affected employees.

Cyber liability insurance covers these costs. It pays for breach notification, credit monitoring, forensic investigation, legal defense, regulatory fines and penalties, and public relations expenses associated with a data breach. If you’re already handling customer data, adding employee data increases the volume and sensitivity of what you’re protecting. If your business didn’t handle much sensitive data before hiring, the employee data you’re now required to collect may be the trigger that makes cyber liability coverage worth carrying.

Insurance considerations for independent contractors vs. employees

The distinction between employees and independent contractors carries significant insurance implications. Workers’ compensation, unemployment insurance and state disability requirements apply to employees, not to independent contractors. But calling a worker a contractor doesn’t make them one. If a worker you’ve classified as a contractor is later reclassified as an employee — by a state labor agency, the IRS or through litigation — you may face back taxes, penalties and retroactive insurance obligations.

Misclassification risk is particularly acute in certain industries. Many states’ workers’ compensation laws are aggressive about contractor classification in high-risk industries, especially construction. In these states, subcontractors who don’t carry their own workers’ compensation coverage may be presumed to be employees of the hiring contractor, making the hiring contractor responsible for their workers’ comp coverage. If one of those uninsured subcontractors is injured on your job site, you may be liable for their medical expenses and lost wages as if they were your own employee.

To protect your business, require certificates of insurance from every independent contractor before they begin work. This verifies that they carry their own general liability and workers’ compensation coverage and establishes the independence of the working relationship. Discuss your use of contractors with your insurance agent to ensure your policies appropriately account for contractor-related exposure.