Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Deciding whether to lease or buy office space starts with a close look at your finances, growth plans and the current commercial real estate market.

If you’ve noticed your office getting a bit more crowded, it’s probably time to look for a new space. And while square footage and amenities matter, the bigger decision — leasing or buying — can shape how your business allocates resources and plans for profitable growth. For companies with strong cash reserves, purchasing property may offer long-term stability. However, tying up capital in commercial real estate doesn’t always deliver the same return as reinvesting in your operations.

Before you take this big step, it’s important to weigh the benefits and drawbacks of buying versus leasing. Here’s a look at what to consider as you compare both options.

Before deciding whether to lease or buy, it helps to step back and ask a few practical questions about your business’s goals, finances, long-term plans and office space needs. Consider the following:

You may hear commercial real estate professionals talk about a “seven-year rule” as a rough guideline when deciding whether it makes sense to buy: If you don’t plan to stay in one location for at least seven years, the upfront costs of buying may ultimately outweigh the benefits. This is why leasing is often the more practical choice for shorter timelines. But if you expect to establish a long-term headquarters — think a decade or more — ownership may become the more financially attractive option over time.

If your business is growing quickly and you anticipate opening a new location or otherwise expanding in the next few years, leasing can offer greater flexibility. That same flexibility can help if your team shrinks or more employees work offsite, since you’re not locked into a long-term ownership commitment.

Buying may reduce that flexibility, since you could end up locked into a layout that no longer fits your team or paying for square footage you don’t fully use, especially if more employees shift to remote work plans or hybrid arrangements.

Local office markets can look wildly different, even when national headlines sound the same. Before you commit to a long lease or a purchase, look at what’s happening in your specific submarket:

If there’s strong demand for buildings in desirable locations in your area, buying may start to make more sense, especially if you expect to stay put for the long haul. But if vacancy is elevated and building owners are competing hard to fill space, you may find leasing offers more flexibility and access to concessions without taking on long-term value risk.

CBRE Research expects commercial real estate leasing activity to continue recovering through 2026, with investment activity projected to increase as larger occupiers return to the market — trends that may influence how aggressively landlords negotiate depending on local demand.

Beyond overall market conditions, take a close look at local rent levels and how quickly they’re changing. If your business is located in a large urban area like New York City, where rents are high, it may make more sense to buy, since your mortgage payments may be equivalent — or even lower than — what you would pay to lease comparable space.

Madison Sutton, a commercial and residential real estate expert, pointed out that instead of paying $10,000 or more each month for rent, business owners could be building equity while protecting themselves from future market disruptions and rent hikes.

Sutton also has seen a trend of business owners investing in mixed-use properties. “Buyers are taking a hybrid approach — operating their businesses in the retail space while utilizing residential units for either personal use or rental income to offset costs,” she explained.

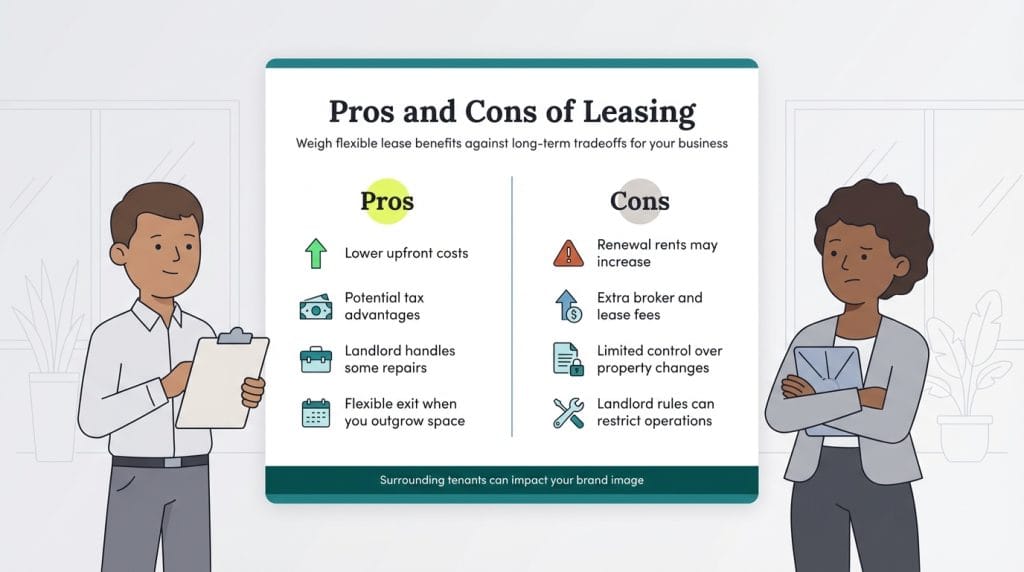

Leasing comes with a mix of tradeoffs. Here’s a closer look at where it tends to work well and where it may fall short.

“Leases allow flexibility for more types of businesses, and some companies can benefit from the prior occupants’ build-out and furnishings,” explained Kristina Chervenka, co-founder and chief operating officer of Five Buffalo Capital.

Owning your office space can change how your business manages growth, cash flow and day-to-day operations. Like any major investment, it comes with advantages and potential risks to weigh carefully.

Chervenka noted that there may be additional risks. “Property tax and interest rate increases can negatively impact the company’s cash flow, and property values may lower when it is time to move the company [or sell],” she said.

As noted above, the longer your commitment is to a location, the more cost-effective it may be to purchase rather than lease your office space. However, before you commit, run some numbers or hire an accountant to analyze the costs over time. Here are some financial factors to compare side by side.

There’s no single answer to whether you should purchase or lease your next property. It depends on how your business is performing, whether preserving cash flow matters more than building equity right now, and how much control you want over your space versus the convenience of someone else managing it. Taking the time to run the numbers now can help you avoid surprises later.

Jennifer Dublino contributed to this article. Source interviews were conducted for a previous version of this article.