Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Specialty Insurance Basics

Businesses need specialty insurance for items not covered by ordinary homeowners or automobile insurance.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

There’s no shortage of insurers or insurance policies for small businesses. However, most policies are designed to provide coverage for companies in general and not for the specific risks your business might face. For example, without the right policy, you won’t be covered for a potentially significant event like a product recall or a professional error that costs your clients money.

For these situations, consider taking out specialty insurance. The good news is that it can be much more competitively priced than standard insurance policies. In this article we’ll dive into the costs, coverage and types of different specialty insurance policies.

What is specialty insurance?

Specialty insurance plans are for businesses that have specific, and often unusual, coverage needs.

You might have expensive, specialized equipment you want to protect, or perhaps you work in a sector where employee fraud is a real and present risk. A standard business policy, like a business owner’s policy, is only available to low-risk industries. Other businesses, such as gun stores and antiques outlets, require specialty insurance for adequate protection.

There is also a market for specialty insurance called excess and surplus (E&S) insurance. E&S insurance are often nonstandard policies, or non-admitted carriers, that offer insurance for high-risk industries or companies that are having trouble finding a provider to cover them.

Tip

If you manufacture or sell products to consumers or businesses, consider taking out product liability insurance. Under U.S. law, manufacturers and retailers are held responsible for any harm caused by a defect in a product, even if they’re not at fault.

Who needs specialty insurance?

Any business that serves clients who engage in high-risk behavior will need to take out a specialty insurance policy.

For example, there are significant risks associated with skydiving, so if you offer it to the public, standard insurance won’t cover you. That’s because your insurer would be subject to a much higher potential exposure to liability claims. Another example is construction businesses; many builders and contractors take out builders’ risk insurance to protect against loss and damage on a project.

Some insurance providers offer specialty insurance plans to businesses in certain industries. For instance, Liberty Mutual has specialty options for the healthcare, environmental, real estate and energy industries. [Read related article: Cyber Liability vs. Data Breach Insurance]

For healthcare providers, for example, standard insurance policies don’t cover sector-specific risks, like specialized equipment failures, patient data breaches and malpractice claims. Healthcare insurance underwriters design policies to ensure that the businesses paying them premiums are sufficiently protected against liabilities related to the sector.

Myles Bancroft, COO of Legacy National Audit Bureau LLC, noted that as the economy evolves, new industries emerge that should consider specialty insurance, such as e-commerce. “A company that imports products from overseas is at risk of coverage gaps,” he explained. “The product liability that undergirds merchandise you purchase from a domestic manufacturer will likely not be adequate on the same product purchased from Asia … specialty insurance can be a useful tool in filling these coverage gaps.”

Does specialty insurance protect against lawsuits?

Like other types of insurance plans, specialty insurance offers protection against lawsuits. If a business is sued and a judgment is made against it, insurers provide defense costs and help with any settlements.

For example, many businesses take out a specialty policy called errors and omissions (E&O) insurance, which protects against negligence lawsuits. The policy has limits, but clients are generally compensated for charges related to judgments such as court and legal fees.

How much does specialty insurance cost?

A common misconception among business owners is that specialty insurance is not affordable. In reality, many rates are surprisingly competitive, depending on your specific needs. Here are some examples of costs associated with specialty insurance:

In every state except for Texas and South Dakota, businesses are required to take out workers’ compensation insurance, which covers both your business and the affected employee for the costs associated with an accident at work.

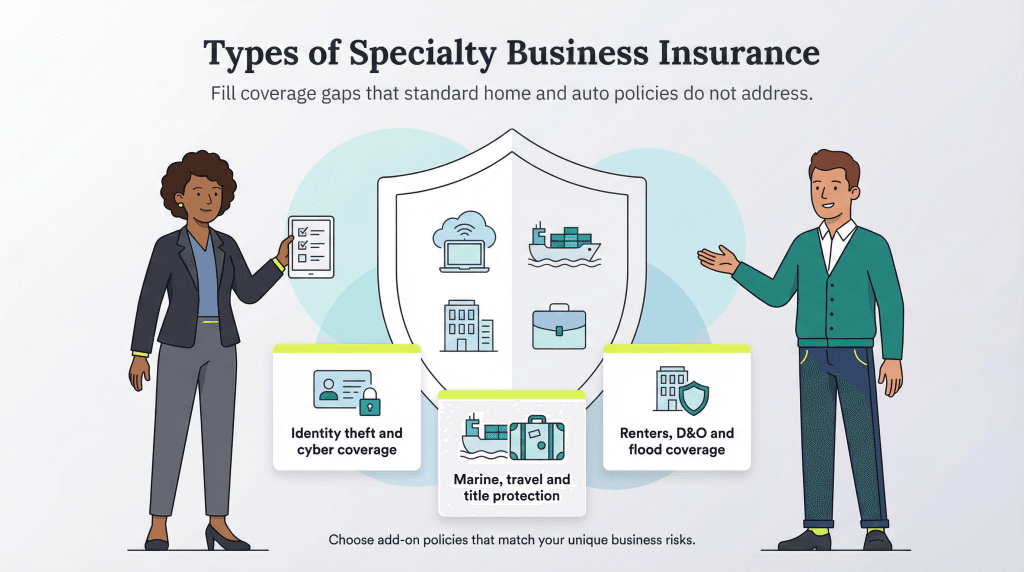

Examples of specialty insurance policies

Homeowner and auto policies are limited in the scope of their coverage and so specialty insurance is necessary. The following types of specialty insurance can help fill in the gaps:

Identity theft insurance: Identity theft can be costly, especially if your company’s bank accounts are compromised. Identity theft insurance can help you cover those costs.

Motorcycle insurance: Standard auto policies that you may take out for your company’s vehicle fleet won’t cover motorcycles. To make up for this, you’ll need commercial motorcycle insurance.

Boat insurance: If your business involves boats — for example, you run a boat touring business or a mini-cruise line — you’ll need boat insurance to cover most of your risks.

Travel insurance: When you plan to travel for work, there’s always the risk that you ultimately won’t be able to get on the plane. In this case, travel insurance covers the amount you spend on your trip, as well as lost baggage or overseas medical emergencies.

Title insurance: If you buy commercial real estate and there’s a defect in your title, you could face substantial financial losses. Title insurance covers these losses.

Commercial renters insurance: Whereas commercial property insurance covers buildings you own, commercial renters insurance offers coverage for business property you rent.

Ocean marine insurance: This specialty insurance category is mandatory if your business owns or operates sea vessels that dock or offload in American ports. It should cover any claims that fall under the Longshore and Harbor Workers’ Compensation Act and the Jones Act.

Directors and officers (D&O) insurance:D&O insurance protects you if you face lawsuits alleging wrongdoings in the management of your business.

Other cases of specialty insurance include insurance for unique considerations, such as for actors who insure their body parts that are considered their best assets and moneymakers. Other types of specialty insurance for businesses include coverage for the loss of your entire inventory in case of a fire or theft.

Did You Know?

Flood damage is not covered by a standard policy. To cover flood damage, you’ll need to purchase flood insurance, which is available through the federal flood insurance program or private insurance carriers.

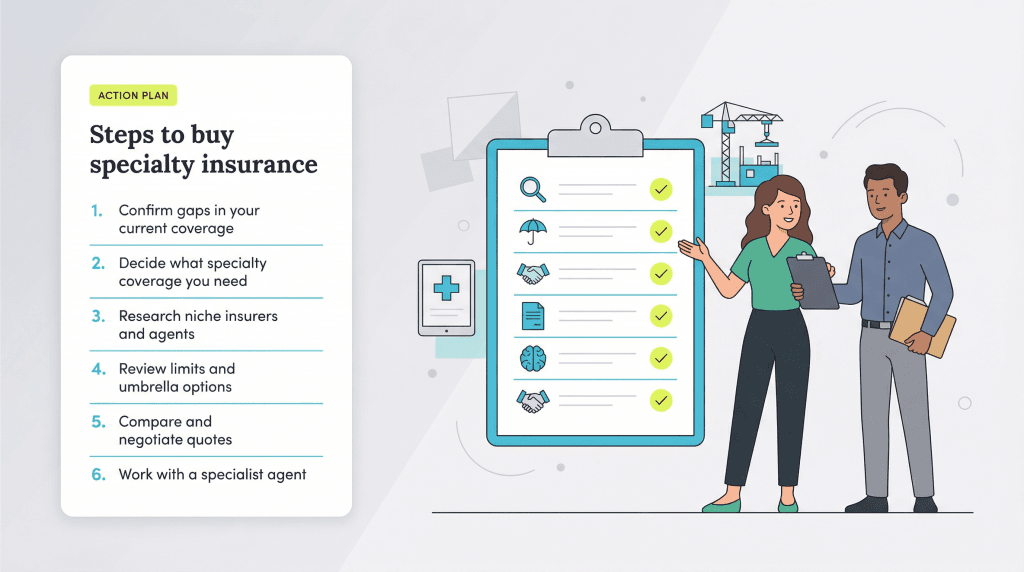

How to buy specialty insurance

Take these steps to ensure you take out the most suitable specialty insurance policy for your business.

1. Understand the different types of specialty insurance.

Specialty insurance isn’t intended to be a one-size-fits-all policy; the underwriting will be specific to your company’s industry and needs. For instance, construction and healthcare businesses both need specialty insurance but will have very different coverage inclusions.

2. Start with basic information on insurance for special needs.

A key step is to confirm that the policies you already have don’t cover your specialty needs. Even if they don’t, though, you may not need an entirely new policy. In some cases, the insurer may be able to add special inclusions to your standard policy.

3. Check out various specialty insurance companies.

Research multiple specialty insurance providers to get an idea of the scope of policies offered. Seek out a specialty insurance company that answers your questions thoroughly. Review their experience in the industry and their records with rating agencies such as the Better Business Bureau.

As you search for specialty insurance plans, consider working only with agents who will vet insurers for you and collect quotes from them. Remember that many agents collect commissions from insurance providers and, therefore, won’t charge you fees.

Check out how much your policy covers in the worst case, and calculate whether it is adequate protection for your assets against judgments. Speak to insurance providers about the option of an umbrella policy, which has minimal annual cost and pays out claims when you’ve exhausted your initial coverage.

Tip

Quotes for specialty insurance depend on your industry and your company’s risk of being sued. You can add an umbrella policy to increase the maximum payouts of your plan.

4. Look at the latest specialty insurance coverage and industry news.

Stay up to date with business insurance information, especially news that’s pertinent to your particular needs. Find out what specialty insurance other providers are offering and what trends are affecting the industry. With this information on hand, you can bargain with service providers to get the best deal for your budget.

5. Compare quotes from different companies (and use them against each other).

Get as many comparable quotes as you can from different specialty insurance providers. Use these quotes to encourage a bidding war between insurers to see if you can negotiate a lower premium.

6. Use an agent to help you purchase the right policy.

When you’re ready to purchase your insurance, make sure you are working with a knowledgeable agent. “One of the most important relationships a business owner can have is with a highly competent, well-connected insurance agent,” Bancroft said. “In order to understand your coverage needs, your agent must thoroughly understand your business. This requires a willingness to share information and ask probing questions … In this day and age, there are very few ‘one size fits all’ solutions for properly insuring your business.”

What to consider when choosing specialty insurance

When you’re choosing the best specialty insurance policy for your business, consider these factors:

Scope of coverage: Make sure you’re covered for all of the risks your business is exposed to, including both industry-specific liabilities and general risks, like cybersecurity threats and professional errors.

Limits and deductibles: The limit is the amount your insurer will pay you for a covered loss, and the deductibles are your out-of-pocket expenses before the insurance kicks in. Make certain that these numbers fulfill your needs.

Claims process: Insurers aren’t particularly keen on paying out and often make the claims process as hard as possible. Check online reviews to see other businesses’ experience in getting the money owed to them.

Unique risks: Your business may face unique risks that aren’t covered by standard types of specialty insurance policies. Work with the insurers that offer the most flexibility with the specific details of your policy.

Renewal policies: Some insurers increase their charges every year. If they don’t, they might gradually reduce the risk they cover. Ask questions and look at reviews to get an idea of how a potential insurer behaves when it’s time to renew a policy.

Industry expertise: Find insurers with deep knowledge of and proven expertise in your sector. They’re more likely to know the insurance companies that target and cater to businesses like yours.

Nathan Weller and Max Freedman contributed to this article.

Mark Fairlie brings decades of expertise in telecommunications and telemarketing to the forefront as the former business owner of a direct marketing company. Also well-versed in a variety of other B2B topics, such as taxation, investments and cybersecurity, he now advises fellow entrepreneurs on the best business practices.

At business.com, Fairlie covers a range of technology solutions, including CRM software, email and text message marketing services, fleet management services, call center software and more.

With a background in advertising and sales, Fairlie made his mark as the former co-owner of Meridian Delta, which saw a successful transition of ownership in 2015. Through this journey, Fairlie gained invaluable hands-on experience in everything from founding a business to expanding and selling it. Since then, Fairlie has embarked on new ventures, launching a second marketing company and establishing a thriving sole proprietorship.