The business credit card you opened when you were starting a business may not be the best fit for the company you run today. As a business grows, spending patterns change, credit needs evolve and new card options become available. A card that once made sense may no longer offer the rewards, credit limits or features your business needs most.

Recognizing when it’s time to upgrade can help you get more value from your spending and avoid paying for features that no longer fit the way your business operates. This guide explains the signs you’ve outgrown your current card, how business credit card upgrades work, what to look for in a replacement card and how to time the transition.

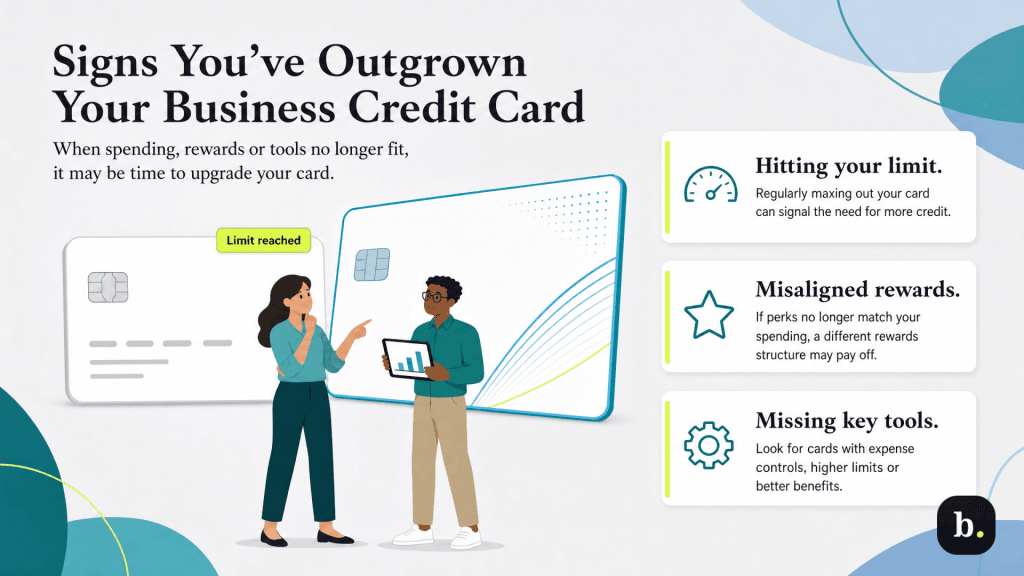

Signs you’ve outgrown your current card

Growth changes more than revenue. It can also affect how your business spends money, manages cash flow and uses credit. If your current card no longer fits the way the business operates, an upgrade may be worth considering. Here are some signs to watch for:

- You’re regularly hitting your credit limit. If spending routinely bumps against your card’s ceiling, a higher credit limit can provide more flexibility and help keep credit utilization in check.

- Your rewards no longer match how your business spends money. As spending patterns change, so does the value of your rewards program. Maybe you travel less than you once did and would now benefit more from cash back. Or perhaps advertising, software subscriptions or other operating expenses have become major spending categories that another card rewards more generously.

- Your credit profile has improved. As your operation grows and your business credit history strengthens, you may qualify for cards with better terms, higher limits or more valuable rewards than were available when you first applied.

- The annual fee no longer makes sense. Paying an annual fee can be worthwhile when you’re using the card’s benefits. If you’re no longer taking advantage of those perks, a different card — or even a no-fee option — may deliver better overall value.

- You need tools your current card doesn’t offer. Growing businesses often need features such as expense management tools, employee cards with spending controls, higher credit limits or expanded travel benefits. If your current card can’t keep up with the way your business operates, it may be time to look elsewhere.

How to upgrade a business credit card

There are two main ways to upgrade a business credit card: request a product change with your current issuer or apply for a new card. The better path depends on whether you want to preserve your current account history, qualify for a welcome offer or move to a card with different features.

Option 1: Request a product change with your current issuer.

A product change lets you swap one card for another, staying within the same business credit card issuer. This is often the easiest way to upgrade your business credit card because it typically keeps your account history intact and usually doesn’t require a hard credit inquiry.

Start by reviewing the cards your issuer allows you to switch to. Product changes are typically limited to cards within the same issuer family, and not every card will be eligible. Then compare the annual fee, rewards structure, credit limit, employee card options and business credit card fees before deciding whether the new card is a better fit.

A product change isn’t always the best deal, though. Some issuers keep their largest welcome bonuses and promotional APR offers for new applicants, not existing cardholders switching products. You may also have fewer upgrade options if the account is less than a year old.

Option 2: Apply for a new business credit card.

Applying for a new card can give you more flexibility, especially if your current issuer doesn’t offer a strong upgrade option. This path may also make sense if you want a welcome bonus, a promotional APR offer, better rewards or features your current card family doesn’t provide.

Before applying, compare the new card’s rewards and benefits against its costs. You should also consider how the new application could affect your credit profile and business credit score. A new application will likely trigger a hard inquiry, while a product change may not.

If you move spending to a new card, think carefully before closing the old one. Closing a card can reduce your total available credit and may affect your utilization ratio. In some cases, keeping the original account open — especially if it has no annual fee — can help preserve your credit history while you use the new card for future business spending.

What to look for in an upgraded card

Not every upgrade is worth making. The best business credit card for your company depends on how you spend, borrow and manage cash flow today — not how the business operated when you first opened a card. As you compare options, focus on features that will deliver meaningful value rather than simply choosing the card with the largest welcome offer. Consider the following:

- Rewards that match your current spending: Review where your business spends the most money and look for a card that rewards those categories. For some companies, that may mean travel, advertising or software subscriptions. Others may benefit more from a straightforward flat-rate cash back card.

- A higher credit limit: If your business has grown, a larger credit line can provide additional flexibility for inventory purchases, seasonal expenses or increased overhead costs. It can also help keep credit utilization lower.

- Travel benefits you’ll actually use: Premium cards often include perks such as airport lounge access, travel credits, travel insurance and no foreign transaction fees. Those benefits can offset a higher annual fee, but only if business travel is a regular part of your operations or you’re planning a global expansion.

- Tools that support a growing business: As transaction volume increases and additional employees need access to company spending, features such as employee cards, spending controls, receipt tracking, integrations with the best accounting software and automated reporting can save time and improve oversight.

Before upgrading, review the last three to six months of card statements. Understanding where your business spends the most money can help you

get the most out of your business credit cards and identify rewards, benefits and features that will deliver the most value.

Will upgrading hurt your credit?

Usually not, especially if you’re upgrading through a product change with your current issuer. A product change that doesn’t involve a hard inquiry typically has little to no effect on your credit because the existing account remains open and its history stays intact. In some cases, an upgrade may even come with a higher credit limit. If spending remains the same, that additional available credit can lower your utilization ratio.

Applying for a new card can have a greater short-term impact. New applications generally trigger a hard inquiry and create a separate account, which can affect factors such as account age and credit utilization. For most businesses, any impact is modest and tends to fade over time. However, it’s something to keep in mind if you expect to apply for a business loan, line of credit or other financing in the near future.

Timing your upgrade strategically

Choosing the right card matters, but timing the upgrade can matter just as much. A little patience — or waiting until after a major financing application — can help you avoid unnecessary headaches and get more value from the move. Here are some tips:

- Use a strong track record to your advantage: If you’ve built a history of on-time payments and responsible card use, your current issuer may be more willing to approve a product change or a new card application.

- Be aware of first-year restrictions: If your account is less than a year old, certain product changes may not be available yet, particularly when the new card carries a different annual fee.

- Consider upcoming financing needs: If you’re planning to apply for a business loan or line of credit in the near future, it may make sense to wait before submitting a new credit card application.

- Redeem rewards before closing an account: Depending on the issuer, points, miles or cash-back rewards may be forfeited when an account closes. Review your rewards balance before making any changes.

- Pay attention to changes from your issuer: Card benefits don’t stay the same forever. Sometimes the changes are gradual, such as new fees or adjustments to a rewards program. Other times they’re tied to bigger industry moves. After Capital One acquired Brex in early 2026, for example, some businesses took a fresh look at whether their existing card setup still made sense.

Credit card rewards aren't always permanent. Some issuers may forfeit unused rewards when an account is closed, so check the program rules before making changes to your card portfolio.

Match your card to the business you’ve become

The business credit card that made sense when you were starting out may not be the best fit today. As spending patterns change, credit needs evolve and new features become available, it’s worth periodically taking a fresh look at whether your current card still delivers value.

An upgrade doesn’t have to be dramatic. Sometimes it’s a simple product change with your existing issuer. Other times, it’s adding a new card that better aligns with the way your business operates. Many growing companies ultimately use multiple business credit cards to maximize rewards, separate spending categories or give employees access to dedicated cards. The goal isn’t to chase the flashiest offer — it’s to make sure your card supports the business you’ve become.