Your business insurance coverage limits represent the maximum amount your insurer will pay for a covered loss. When those limits are set correctly, they provide a financial safety net that protects your business from losses that could otherwise threaten its survival. When they’re set too low — which is far more common than most business owners realize — the gap between your coverage and your actual exposure comes directly out of your business’s assets.

Underinsurance is one of the most prevalent and costly mistakes in small business risk management, and it’s almost always unintentional. Business owners set appropriate limits when they first purchase their policies, and then their business grows while their coverage stays the same. Revenue increases, employees are hired, property is acquired, contracts impose new requirements, and the limits that were perfectly adequate a few years ago quietly become inadequate without anyone noticing — until a claim exceeds them.

This guide explains how coverage limits work, identifies the most common triggers that signal it’s time to increase them and provides a practical framework for evaluating whether your current limits are sufficient.

What coverage limits are and how they work

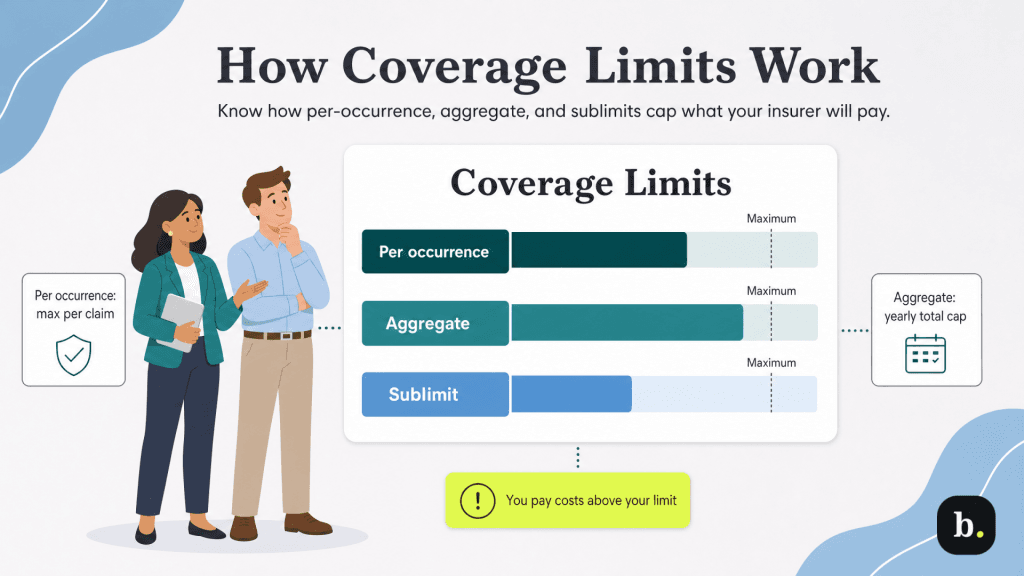

Every insurance policy has defined coverage limits that cap the insurer’s maximum payout. Understanding the different types of business insurance limits is essential to evaluating whether yours are adequate.

- Per-occurrence limits set the maximum amount the insurer will pay for any single claim or event. If you have a general liability policy with a $1 million per-occurrence limit and a single claim results in a $1.3 million judgment, your insurer pays $1 million and you’re responsible for the remaining $300,000.

- Aggregate limits set the maximum total payout across all claims during the policy period, which is typically one year. A general liability policy with a $1 million per-occurrence limit and a $2 million aggregate will pay up to $1 million for any individual claim, but no more than $2 million total for all claims combined during the year. If you experience multiple claims in a single policy period, you can exhaust your aggregate limit even if no individual claim reaches the per-occurrence cap.

- Sublimits are lower limits that apply to specific categories within a broader policy. For example, a commercial property policy with a $500,000 overall limit might include a $50,000 sublimit for electronic data restoration or a $25,000 sublimit for outdoor signage. Sublimits are easy to overlook because they’re buried in the policy details, but they can create significant gaps if a loss falls into a sublimited category.

The fundamental principle to remember is that once any limit is exhausted, the insurer’s obligation ends. Any costs beyond the limit are your responsibility. This is why setting limits correctly and revisiting them regularly matters so much.

The terms of your policies, including the business coverage limits, are typically set during the

insurance underwriting process. Make sure you read the fine print and understand your coverage amounts before signing any policy documents.

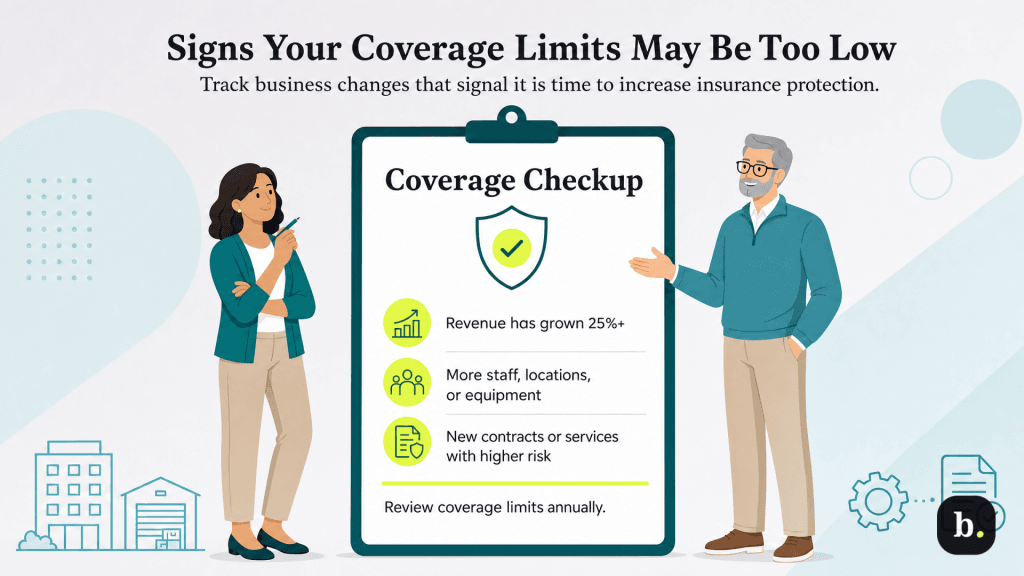

Signs your coverage limits may be too low

Several common business changes are reliable signs that your coverage limits need to be reevaluated. If any of the following apply to your company since your business insurance limits were set, it’s time for a review — and it might be time to increase insurance coverage.

Your revenue has grown significantly.

Revenue is closely tied to exposure for liability coverage. Higher revenue means more customer interactions, more transactions, more deliveries, more service engagements and more opportunities for incidents that result in claims. General liability limits that were appropriate when your business generated $500,000 in annual revenue may not adequately protect a business now generating $1.5 million or $2 million.

A useful rule of thumb: If revenue has grown 25 percent or more since your limits were last reviewed, it’s time for a fresh look. Note that the relationship between revenue and appropriate limits isn’t strictly proportional — a business doesn’t necessarily need to double its limits when it doubles its revenue — but the growth is a clear signal that the exposure profile has changed and the limits need to be tested against current conditions.

You’ve added employees.

Every employee you add expands your exposure in multiple directions. More employees interacting with customers and the public increases general liability exposure. More workers performing job duties increases workers’ compensation exposure. A larger team increases the potential for employment practices claims. Wrongful termination, discrimination, harassment and wage disputes all become more likely as headcount grows.

For workers’ compensation, the limit structure is typically governed by state law, but your payroll reporting and employee classifications must be accurate and up to date. Underreporting payroll during the policy period results in premium audit adjustments at the end of the term. Beyond workers’ comp, if your team has grown meaningfully, evaluate whether your general liability limits still reflect the scale of your operation and whether you need employment practices liability insurance if you don’t already carry it.

You’ve acquired new property or equipment.

Commercial property coverage should reflect the current replacement cost of everything it insures: the building (if you own it), equipment, inventory, furniture, fixtures, technology, signage and tenant improvements. Businesses accumulate property value incrementally over time — a new espresso machine here, a technology upgrade there, an expanded inventory for the holiday season — without updating their insurance policy. Each addition widens the gap between what you own and what your policy covers.

Ask yourself: If a fire destroyed everything in your business tomorrow, would your property coverage be sufficient to replace it all at current prices? If the answer isn’t a confident yes, your limits need to be adjusted. This question is particularly important given the coinsurance clause in many commercial property policies. Coinsurance requires you to insure your property to at least a specified percentage of its actual replacement value. If your insured amount falls below that threshold, the insurer reduces your payout proportionally, even on partial losses.

For example, if your property is worth $500,000 but you’re insuring it for only $300,000 under a policy with an 80 percent coinsurance requirement, you’re insured for 75 percent of the required amount ($300,000 divided by $400,000). A $100,000 loss would only pay $75,000 — even though $100,000 is well within your $300,000 policy limit. The coinsurance penalty makes underinsurance more expensive than many business owners realize.

You’ve signed contracts with higher insurance requirements.

Enterprise clients, government agencies, commercial landlords and lenders frequently specify minimum insurance limits as a condition of doing business. These requirements can vary significantly. One client may require $1 million in general liability coverage; another may require $2 million per occurrence and $5 million in umbrella coverage. Landlords often require specific property and liability limits as conditions of the lease.

If you’ve signed contracts in the past year with insurance requirements that exceed your current limits, you need to increase your coverage to remain in compliance. Failing to maintain the coverage levels specified in a contract is a breach of that contract, which can expose you to additional liability beyond just the insurance gap itself.

You’ve expanded your physical footprint.

Opening a new location, moving to a larger space, or leasing additional warehouse or storage capacity increases both your property and liability exposures. Each location must be reflected in your insurance policy with appropriate coverage limits. A policy written for a single 1,200-square-foot retail shop doesn’t automatically extend to cover a second location or a warehouse you’ve added.

Business interruption coverage is particularly sensitive to physical expansion. Your monthly operating expenses — rent, payroll, loan payments, utilities — have almost certainly increased along with your footprint. If your business interruption limit is based on the overhead from your original, smaller operation, it won’t come close to sustaining your current operation through an extended closure. Recalculate your monthly fixed costs at their current level and ensure your business interruption limit provides adequate coverage for a realistic recovery period.

You’ve launched new products or services.

New products introduce new product liability exposure. New services may introduce new professional liability exposure. If your general liability or professional liability policy was underwritten based on your original business activities, it may not adequately cover claims arising from offerings that didn’t exist at the time the policy was written.

In some cases, new activities require not just higher limits but entirely new coverage types. Adding an e-commerce channel to a brick-and-mortar business may warrant cyber liability coverage. Adding a consulting service to a product business may require professional liability coverage for the first time. Launching a food product introduces product liability considerations that a service business may never have faced before. Each new offering should prompt a conversation with your agent about both limits and coverage scope.

Your industry has experienced increased claims activity.

Some industries go through periods of elevated claims frequency or rising average settlement amounts. Healthcare, construction, technology and professional services have all experienced periods where the claims environment became more aggressive. If your industry’s claims landscape has shifted since your limits were last set, limits that were adequate a few years ago may no longer provide sufficient protection against today’s claim values.

Your insurance broker, industry trade association or industry publications are good sources for staying current on claims trends in your sector. If average claim settlements in your industry have risen meaningfully, that’s a direct signal that your limits may need to rise as well.

Understanding umbrella and excess liability policies

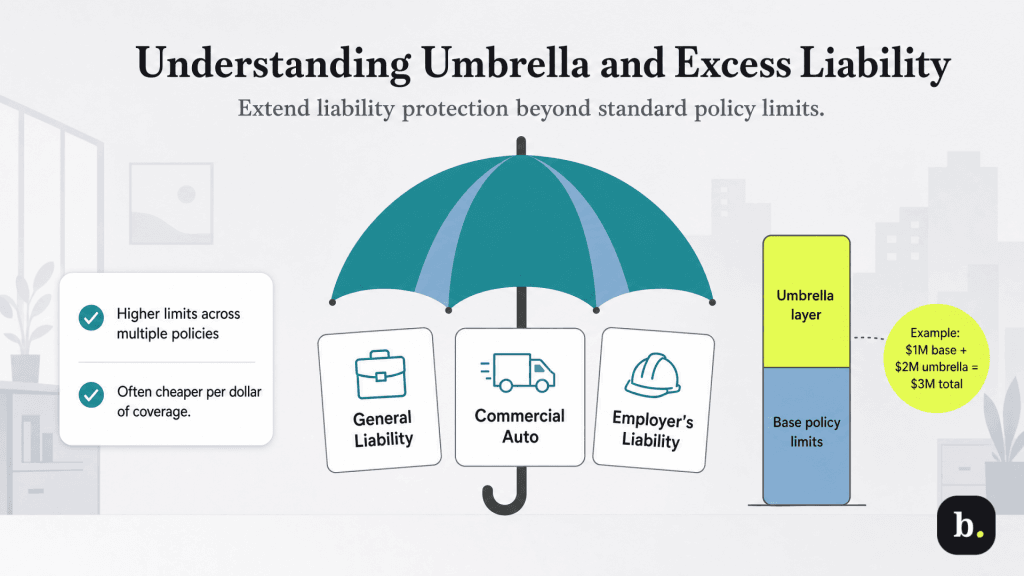

When your liability limits need to increase, you have two options: raise the limits on your underlying policies or add umbrella insurance or an excess liability policy that provides additional coverage above the underlying limits. For many businesses, an umbrella policy is the more cost-effective choice.

An umbrella policy provides an additional layer of liability coverage above the limits of your underlying policies — typically general liability, commercial auto and employer’s liability. If your general liability policy has a $1 million per-occurrence limit and your umbrella provides $2 million in additional coverage, your total protection for a covered liability claim is $3 million. The umbrella only pays after the underlying policy’s limit is exhausted, which is why it’s often described as “sitting on top of” your other policies.

The cost advantage of umbrella coverage is significant. Because umbrella policies only respond to losses that exceed the underlying limits — which are statistically less frequent — the premium per dollar of coverage is much lower than the premium on your base policies. For a low-risk small business, $1 million in umbrella coverage might cost roughly $500 to $1,000 per year, making it one of the most affordable ways to increase your total liability protection significantly.

Some umbrella policies also provide slightly broader coverage than the underlying policies, picking up certain claims that might not be covered by the base policy. However, this varies by insurer and policy form, so don’t assume broader coverage without confirming the specific terms with your insurance agent.

Umbrella policies typically require minimum underlying limits before they’ll attach. Common requirements include $1 million per occurrence on general liability and $1 million combined single limit on commercial auto liability. Your insurance agent can confirm the specific requirements for the umbrella policies available to your business.

How to evaluate whether your business insurance limits are adequate

The most practical way to evaluate your coverage limits is to work through a realistic worst-case scenario analysis for each major coverage type. This isn’t about imagining the most catastrophic event conceivable. Rather, it’s about estimating the most expensive plausible loss your business could realistically experience and comparing it to your current limit. Here’s how to do that for the most common insurance policies.

- General liability: Consider the most serious plausible incident involving a third party: a customer seriously injured on your premises, a product defect that injures multiple people or a significant property damage event caused by your operations. Factor in not just the direct injury or damage costs but also legal defense expenses and the potential for a larger-than-expected jury verdict. If the realistic worst-case scenario exceeds your per-occurrence limit, you need more coverage.

- Commercial property: Calculate the full replacement cost of all insured property at current market prices. This means what it would cost to replace everything today, not what you originally paid. Include equipment, inventory at peak levels, furniture and fixtures, technology, tenant improvements and any building ownership. Compare that total to your policy limit and check it against any coinsurance requirements.

- Business interruption: Estimate how long it would realistically take to resume full operations after a catastrophic property loss — not just the time to repair the physical space, but the time to replace equipment, restock inventory, rehire and retrain staff if necessary, and rebuild customer flow. Calculate your total monthly fixed expenses (rent, payroll, loan payments, utilities, insurance premiums, and other obligations that continue whether or not you’re generating revenue) and multiply by that recovery period. If the result exceeds your business interruption limit, you’re underinsured for this scenario.

- Professional liability: Consider the value of the largest engagement or project you work on, and the potential financial impact of an error on it. Professional liability claims often include not only the cost of correcting the error but also the downstream financial consequences to the client — lost revenue, additional costs and consequential damages. If your largest engagement could result in a claim exceeding your current limit, your coverage needs to be reviewed.

For each coverage type, if your realistic worst-case estimate exceeds your current limit, the gap is your uninsured exposure. That exposure is the amount that would come directly out of your business’s assets in the event of a maximum-severity loss. Such exposure means your coverage limits aren’t adequate.

The cost of increasing coverage limits

One of the most common reasons business owners don’t increase their limits is the misguided assumption that doing so is prohibitively expensive. In reality, the cost of higher limits is often far more modest than expected, because insurance pricing is not linear.

The first dollar of coverage is the most expensive because it covers the most likely, most frequent losses. Higher layers of coverage cost progressively less per dollar because they only pay out in less frequent, more severe scenarios. Doubling your general liability limit from $1 million to $2 million per occurrence does not double your premium — it typically adds somewhere between 15 percent and 30 percent to the premium, depending on your industry and risk profile. Umbrella policies are the most dramatic example of this principle. Because they only respond after your underlying limits are exhausted, the per-dollar cost of umbrella coverage is a fraction of the per-dollar cost of your base policies.

When evaluating the cost of increasing limits, frame it in terms of the alternative. The premium increase is a known, budgetable, annual expense. The cost of being underinsured is an unknown, potentially catastrophic event that could consume years of profits or threaten the business’s existence. For most businesses, the premium increase required to close coverage gaps is a straightforward and easily justifiable investment.

Ensuring you’re not an underinsured business

Business insurance coverage limits are not a set-it-and-forget-it decision. They need to evolve alongside your business. Underinsurance is a silent risk. Everything appears fine — you have insurance, you’re paying premiums, you have a policy document in your files — until a claim exceeds your limits and the gap comes directly out of your business’s assets. The cost of discovering that gap through an actual loss is orders of magnitude higher than the cost of preventing it through regular limit reviews.

Review your limits annually as part of your broader insurance review, and trigger an off-cycle review any time a significant business change occurs. Work with your insurance agent to run worst-case scenarios for each major coverage type, evaluate your exposure against your current limits and identify the most cost-effective way to close any gaps — whether that’s increasing your underlying policy limits, adding an umbrella policy or both. The premium cost of adequate limits is almost always a fraction of the potential cost of being underinsured.