Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

You might need insurance coverage for workers’ compensation. Here’s when you should consider a ghost policy option.

As a small business owner, you may be considering business insurance for workers’ compensation. But what if you don’t have any employees? In that case, there are a number of alternative options for workers’ comp. If you need to provide an affordable certificate of insurance upon request quickly, a workers’ compensation ghost policy may be a good option.

Before you decide if a workers’ comp ghost policy is the right fit for your small business, you’ll need to understand what a ghost policy is. This information will help you determine whether you meet the requirements for a ghost policy and whether it exposes your business to additional risk.

A workers’ compensation ghost policy is sold in the marketplace just like standard workers’ compensation insurance, but there are important differences between these policies. A ghost policy, when used on its own, does not cover the business owner or employees. It doesn’t cover anyone or anything.

A ghost policy is simply used to do business with a vendor or place of business or to meet state requirements. In some states, a ghost policy can be used as a certificate to meet the insurance requirements of the vendor, client or contractors. Again, the ghost policy doesn’t offer any actual or tangible coverage, although some insurers bundle this policy with an accident-only plan to create a low-cost insurance coverage package.

“[Ghost policies’ lack of actual coverage] needs to be emphasized,” said Paul Koenigsberg, attorney at Koenigsberg & Associates. “It is not unheard of for businesses to get a false sense of security once they have a ghost policy. If the business owner or their contractors require coverage, a traditional workers’ comp policy or another form of insurance is still necessary.”

To purchase a workers’ comp ghost policy, you need to be a business owner with no employees and no payroll (besides the owner). For example, your business can be a one-person S corporation, a sole proprietorship or a single-member limited liability company with no employees or contractors working for the business or plans to hire them. In addition, the policyholder must be between the ages of 18 and 65 and must have a valid Social Security number.

However, a ghost policy shouldn’t cover the policyholder. “Since a ghost policy is only there to satisfy requirements, be sure that the contract you’re trying to satisfy doesn’t require the owner to be included in the coverage,” said Mordechai Kamenetsky, co-founder at Kickstand Insurance. “I’ve seen this happen often, especially with truckers — they get a ghost policy and then they realize that the carrier requires the owner to be included.”

A workers’ compensation ghost policy is best for self-employed individuals who have no employees and work in low-risk jobs. If you need to show proof of workers’ comp but don’t have any employees, a ghost policy may be a good choice.

However, not everyone who is self-employed needs a ghost policy. You’ll benefit from it the most in these situations:

Kamenetsky said that ghost policies offer especially strong benefits for contractors and subcontractors. “The subcontractor can’t file a workers’ comp claim against the contractor or their workers’ comp insurance policy,” he said. “The contractor doesn’t have to pay workers’ comp premiums on the subcontractor’s wages.”

Although ghost policies can be written for businesses that need specialty insurance, your risk will be higher in this case. Consult an insurance agent to determine whether a ghost policy is the best choice for your situation. [Related article: The Best Commercial Insurance for Entrepreneurs]

Workers’ comp laws vary from state to state, so be aware of how these differences might affect your business. In North Carolina, for example, if someone hires a contractor with a ghost insurance policy and that worker is injured on your property, you could be held responsible for all medical costs.

In most states, workers’ compensation insurance is required by law. However, there is a patchwork of laws across the country. Ghost workers’ compensation policies aren’t available, for example, in some states like California and Colorado.

Currently, Texas is the only state that does not require employers to have workers’ compensation coverage. Electing workers’ compensation insurance limits the amount and type of compensation that an injured employee may receive and those limits are set in the law in Texas.

In Alabama, you can legally opt for a ghost workers’ compensation policy if you employ five or fewer full-time or part-time employees regularly. Employers of domestic employees, farm laborers or casual employees and municipalities with populations of fewer than 2,000 are not required to provide coverage but can elect to be covered by the provisions of the Alabama Workers’ Compensation Law.

In California, the law requires that employers carry workers’ compensation insurance, even if they have only one employee. According to the state, you cannot file for a workers’ compensation exemption if any of the following conditions exist:

There is an exemption for out-of-state contractors who are licensed in California but do not hire employees who reside in California. However, if you have out-of-state employees who work in California, you must also provide a certificate of insurance from your workers’ compensation insurance carrier in your state.

Kamenetsky also noted that some ghost policyholders may need to obtain formal exemption. “Some carriers that offer ghost policies require that the insured sign documents to be exempted from workers’ comp,” he said. “This involves completing the workers’ comp exemption process specific to their state. They want to ensure the policy is legitimate and complies with state requirements.”

>> Learn more: How Much Workers’ Compensation Do You Need?

The cost of workers’ comp policies is based on payroll. Because there is no payroll when a business doesn’t have employees, the cost of a ghost policy is typically lower than that of a traditional workers’ comp policy. “A ghost policy is audited at expiration to determine if there was any payroll,” Kamenetsky said. “If payroll to others is discovered, the ghost policy becomes null and void. If the owner of a ghost policy decides to hire workers at any time during the policy term, the policy must be changed to a standard workers’ comp policy.”

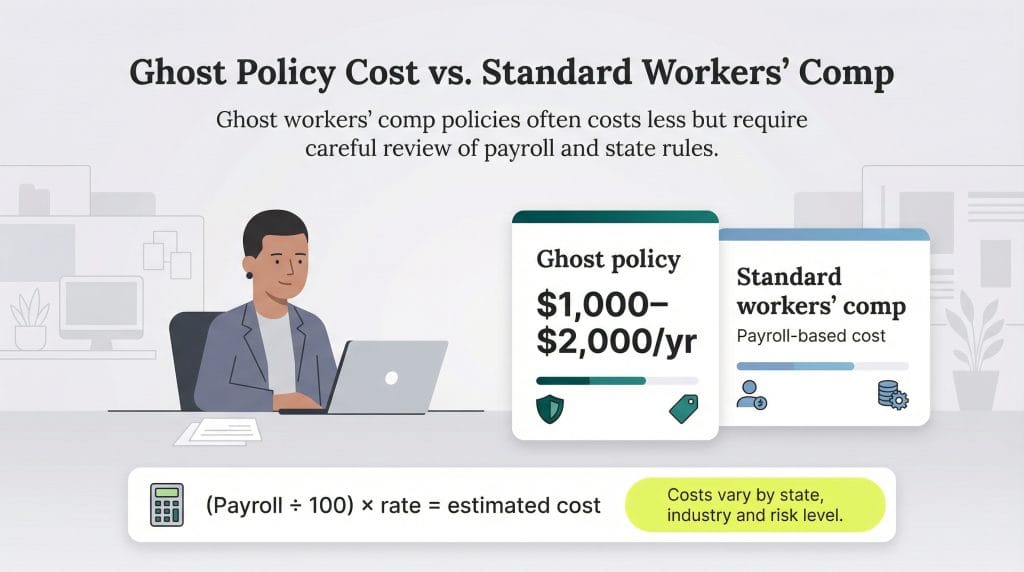

The savings on ghost insurance premiums can be noteworthy, especially in contract bidding wars. In some cases, a contractor can offer a lower bid on a project since many ghost insurance policies cost less than a full policy. You can expect to pay $1,000 to $2,000 per year for a ghost policy, though this may vary by region, industry and other factors. You can compare the cost with a standard workers’ compensation policy by using the following formula:

(Annual employee payroll / 100) x workers’ comp insurance rate = estimated workers’ compensation cost

Note that this formula relies on variables and because workers’ compensation laws vary by state, you will need to review state laws to get an accurate calculation of your workers’ compensation insurance cost. Comp codes or class codes are assigned to different types of work an employee does and the risk of injury associated with the job. This risk is another factor that determines the cost of premiums. Kamenetsky also noted that many ghost policy providers require payment of the entire annual premium upfront, with no options for payment plans.

Some ghost policies are underwritten through the state-assigned risk pool, but some insurers have access to a workers’ comp ghost policy that is substantially less expensive than the pool in most states. Be sure to ask your insurance agent about this to find the most affordable option for you.

Although ghost policies can save you money, sometimes, it’s better to opt for a traditional policy if the cost difference is minimal based on your business’s class code and if there is a moderate liability risk. Be sure to compare the numbers and consider that traditional workers’ compensation coverage pays for medical expenses and replaces a portion of missing wages when a covered person is unable to work. This coverage can be vital to cash flow and peace of mind, especially if you are the sole business owner.

Max Freedman and Jamie Johnson contributed to this article.