Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Many businesses are adding the cost of payment processing to customers' purchases. Learn the pros and cons of this tactic and some alternatives.

Credit card processing fees are inescapable when your business accepts credit card payments. Many businesses cover these costs by passing them on to the customers who use credit cards — a practice called “surcharging.” Is surcharging a smart way to cover processing fees or does it run the risk of frustrating your customers? Read on to learn more about the practice and if it’s right for your business.

Credit card surcharges are extra charges added onto customer purchases by a business in order to offset credit card processing fees. These surcharges only apply to credit card transactions, not debit card or cash payments.

“As consumers move further away from using cash and debit cards, credit card volume and higher processing fees have followed,” said Eric Cohen, founder and CEO of Merchant Advocate. “Faced with rising business costs, more and more merchants are adopting surcharging programs.”

Credit card surcharging can benefit a business’s bottom line in the following ways.

Credit card surcharges cover the cost of processing fees, cutting costs and improving profitability. For businesses with thin margins, these small savings can make a difference.

“If a business makes a 20 percent margin on a product sale, [a] 3 percent [fee] can start to eat into that profit margin,” said Lou Haverty, owner of online retailer Skid Retailer.

Surcharging may make it possible for businesses that otherwise wouldn’t be able to absorb processing fees to accept credit card payments. According to a Federal Reserve report, nearly 40 percent of consumers prefer using a credit card for in-person payments; offering this payment method is increasingly part of providing a great customer experience.

Credit card surcharges may incentivize customers to pay with a debit card or cash, rather than a credit card. Credit card payments generally take one to three business days to process and settle, whereas debit card payments are processed instantly and cash payments are immediately available in your register.

While offsetting credit card fees is a huge advantage for businesses, surcharging has some distinct downsides.

Customers may dislike surcharges so much that they choose to patronize other businesses instead. A 2024 PYMNTS study found 56 percent of credit card users would likely switch to another merchant if asked to pay a surcharge.

“While it makes sense from a business perspective, customers don’t always see it that way,” said Alicia Collins, founder and CEO of K9 Activity Club. “Some won’t care, some will complain and others will walk away.”

If most of your customers pay with a credit card, surcharges effectively increase your prices and put your business at a competitive disadvantage. It’s especially important to consider customer alternatives if you’re competing against online retailers that offer free shipping and fast delivery.

“[It’s] very easy for consumers to compare prices online,” Haverty said. “My strategy is to make up for the credit card surcharge cost in sales volume rather than directly passing the cost on to the buyer.”

Credit card surcharging is prohibited in several states and restricted in others. If you do business in one of these areas, you could face legal trouble for adding a surcharge or doing so improperly, which may result in fines and negative publicity.

Moreover, all states prohibit merchants from profiting from a credit card surcharge. Merchants are also prohibited from adding a surcharge to debit card purchases.

“The merchant must have payment systems that distinguish between credit and debit cards,” Cohen explained. “However, many current point-of-sale systems lack this functionality, creating further challenges.”

If you decide to surcharge credit cards, consider the following steps:

You must meet all surcharging requirements, including the following:

“Failure to comply can result in penalties, including fines or suspension of payment processing privileges,” Cohen cautioned. “Staying informed by doing your own research or seeking assistance from an independent third party like Merchant Advocate is critical to avoid costly mistakes.”

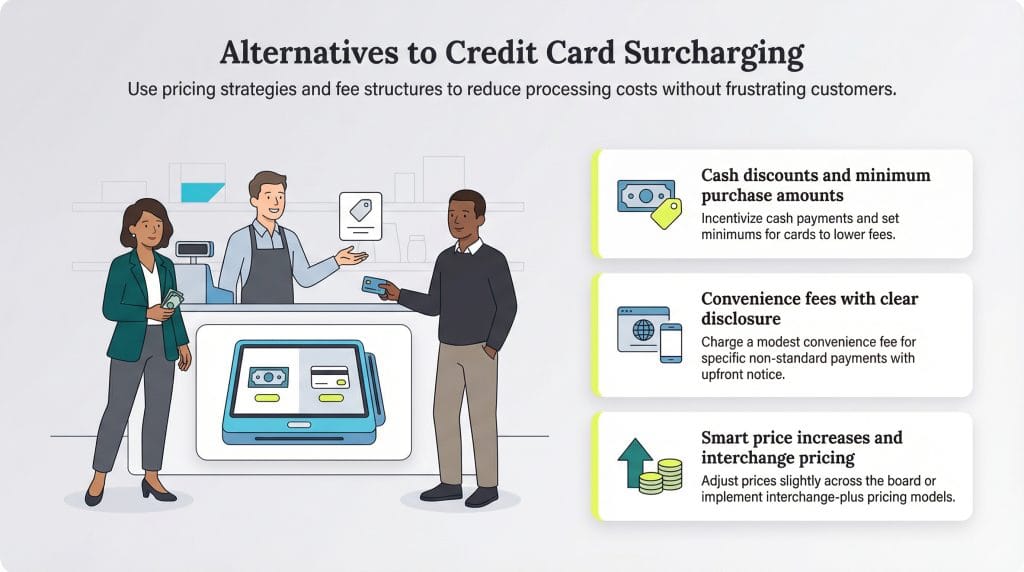

Surcharging isn’t the only way to reduce credit card processing fees. Consider the following alternatives.

Price your goods or services as if everyone will pay with a credit card. Then, offer a cash discount for customers who choose not to pay with plastic, instead of adding a surcharge for those who use credit cards.

Businesses that pay their processor a percentage plus a flat fee for each transaction may lose money on small sales paid for by credit card. Excluding small purchases from credit card payments with a minimum purchase amount can reduce overall processing fees.

Businesses can charge a convenience fee when customers use a nonstandard payment method, such as paying with a credit card by phone or online.

Convenience fees typically range from 1.3 percent and 3.5 percent and may have a minimum amount. The rules regarding convenience fees vary by card type.

Visa’s rules regarding convenience fees include the following:

Mastercard’s rules for convenience fees include the following:

American Express’s rules for convenience fees include the following:

These rules can change at any time. Check with each card brand for the most current information.

Although raising prices across the board can result in slightly higher credit card fees, it can also increase your profit margin and help you avoid backlash from card-paying customers who may feel penalized. Before raising prices, consider the competitive landscape and whether raising prices may lead to lost business.

Lowering your credit card processing costs benefits both you and your customers. Not all processors charge the same way. While all credit card processors charge the interchange rate — the amount set by card brands like Visa, Mastercard, American Express and Discover — some make their money by charging a flat monthly fee instead of adding a markup on top of the interchange rate.

Sally Herigstad contributed to this article.