Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Learn when to consider a cash advance and when it’s a bad idea.

If you’ve ever needed cash quickly, you know the pressure and stress it can cause. Nobody likes having bills they can’t cover, so many businesses turn to a type of financing known as a cash advance. These short-term loans don’t usually require a lengthy application or credit check. They may seem like a quick fix, but cash advances aren’t always a wise choice. In many cases, they can make an already difficult financial situation worse.

So how do you know when a cash advance makes sense and when it’s better to look for another option? We’ll break down how cash advances work, along with their pros and cons, to help you make an informed financing decision for your business.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

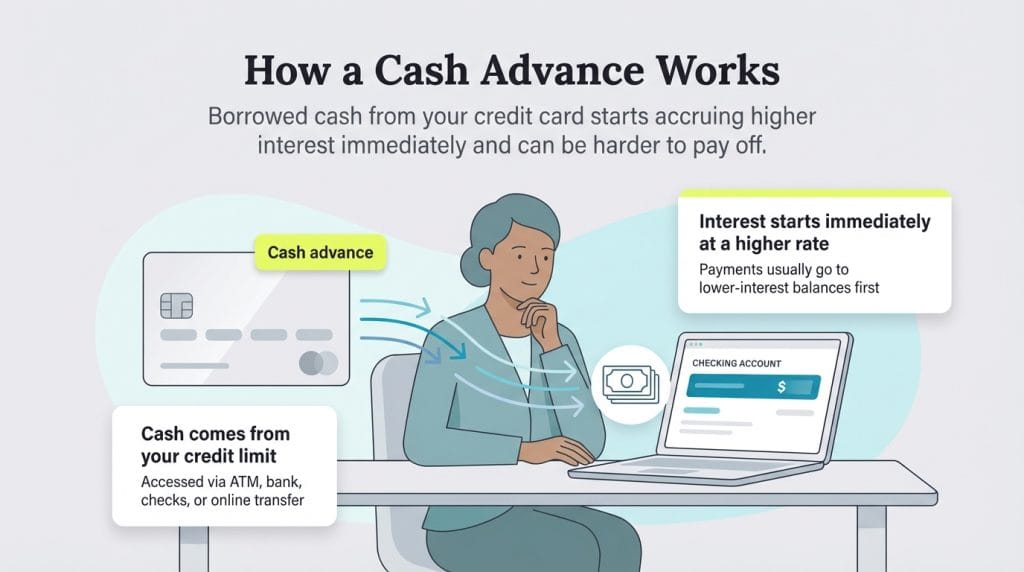

A cash advance is a short-term loan that lets you borrow against your credit card’s available limit. You can get the cash at an ATM, through a bank branch or via an online transfer. Not all business credit cards allow cash advances, but many small business owners use them to cover payroll or handle financial emergencies.

“A cash advance is basically where you borrow money from your credit card and pay a pretty exorbitant interest rate upon repayment,” explained Andrew Schrage, co-founder and CEO of Money Crashers.

Cash advances are one of the most expensive ways to borrow. They typically carry higher interest rates than standard credit card purchases — often 25 percent or more — plus additional fees. Because of these costs, a cash advance should only be used in emergencies and when you can pay the balance back quickly.

While credit card cash advances let you borrow against your card’s limit, a merchant cash advance (MCA) works differently. With an MCA, your business gets a lump-sum payment in exchange for a percentage of future sales.

Unlike credit card cash advances, which charge fixed interest rates, MCAs use a factor rate system. For example, if you receive a $10,000 advance with a factor rate of 1.4, you’ll owe $14,000 in total. Repayment is usually automated, with the MCA provider deducting a set percentage of your daily credit card sales (often 5 to 20 percent) until the balance is paid off.

A cash advance works by letting you borrow cash against your credit card limit. You can access this cash in several ways:

Like any loan, you must repay your cash advance. However, repayment works differently from regular credit card purchases. There’s no grace period — interest starts the moment you take the cash, usually at a higher APR than your standard rate. The advance simply appears on your next credit card statement and is due with your regular monthly payment. But here’s the catch: card issuers usually apply your payment to lower-interest purchases first, so the cash advance balance (with its higher rate) can stick around longer and cost you more.

Fees also apply, either as a flat amount per transaction or as a percentage of what you borrow. Some issuers deduct the fee upfront, while others add it to your bill later.

Cash advances are easy to get, but that convenience comes with steep costs. On top of higher interest rates than regular purchases, you’ll likely face extra fees every time you use this feature.

Here are the most common ones:

To put that into perspective, if you take a $300 cash advance with a 28.99 percent APR, a $15 fee and a $3.50 ATM charge, your one-month cost would be about $25. And if you don’t pay it off right away, interest keeps adding up each month.

Cash advances have upsides and downsides. Here’s a closer look:

Because cash advances come with high costs and risks, it’s smart to explore other financing options first. The Small Business Administration suggests comparing different types of loans and credit to see what makes sense for your situation.

Here’s a quick look at some common alternatives:

Financing type | Interest rate | Approval time | Qualification requirements | Repayment terms |

|---|---|---|---|---|

Cash advance | 25-30 percent-plus APR | Same day | Credit card required | Immediate, high fees |

SBA loans | Typically 10-12 percent APR | 30-90 days | Good credit (670+), 2+ years in business | 5-25 years |

Term loans | 6-36 percent APR | 2-30 days | Good credit, business history | 1-7 years |

Business line of credit | 8-25 percent APR | 1-7 days | Established revenue | Revolving |

Invoice factoring | 1-5 percent per month | About 1 week | Outstanding invoices | 30-90 days |

While these financing options are typical alternatives to cash advances, don’t forget about simpler options too:

Credit card cash advances from your issuer have clearly disclosed terms, but other types of cash advances — especially some merchant cash advances — have drawn scrutiny for unfair practices. The Consumer Financial Protection Bureau has established rules requiring clear disclosure of terms for business credit products, and the Federal Trade Commission has taken action against companies that use deceptive practices in merchant cash advance marketing.

Here are a few red flags to watch for in any lending situation:

And here are a few signs that you’re dealing with a reputable provider:

Cash advances are expensive, so they should only be a last resort. Here are a few things to think about before you decide:

Ask yourself:

A cash advance should be reserved for true emergencies, such as repairing essential equipment, buying critical inventory or covering payroll in a pinch. It’s not a smart solution for long-term projects, paying down other debt or discretionary spending.

Cash advances are costly and can quickly lead to a cycle of high-interest debt. In most cases, avoiding them is the smartest move. But if you’re facing a true emergency and don’t have another fast option, a cash advance can bridge the gap — as long as you’re confident you can repay it quickly.

Remember, debt should be a tool you use strategically, not something you rely on to stay afloat. If you find yourself depending on high-interest financing just to keep the lights on, it may be worth stepping back to reassess your business model and explore more sustainable ways to move forward.