Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

There’s a Fee for That: Pros and Cons of Surcharging Credit Cards

Many businesses are adding the cost of payment processing to customers' purchases. Learn the pros and cons of this tactic and some alternatives.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Credit card processing fees are inescapable when your business accepts credit card payments. Many businesses cover these costs by passing them on to the customers who use credit cards — a practice called “surcharging.” Is surcharging a smart way to cover processing fees or does it run the risk of frustrating your customers? Read on to learn more about the practice and if it’s right for your business.

What are credit card surcharges?

Credit card surcharges are extra charges added onto customer purchases by a business in order to offset credit card processing fees. These surcharges only apply to credit card transactions, not debit card or cash payments.

“As consumers move further away from using cash and debit cards, credit card volume and higher processing fees have followed,” said Eric Cohen, founder and CEO of Merchant Advocate. “Faced with rising business costs, more and more merchants are adopting surcharging programs.”

Tip

If a consumer pays with Apple Pay or another digital wallet using a linked credit card, a credit card surcharge should apply.

What are the pros of credit card surcharging?

Credit card surcharging can benefit a business’s bottom line in the following ways.

Credit card surcharging improves profit margins.

Credit card surcharges cover the cost of processing fees, cutting costs and improving profitability. For businesses with thin margins, these small savings can make a difference.

“If a business makes a 20 percent margin on a product sale, [a] 3 percent [fee] can start to eat into that profit margin,” said Lou Haverty, owner of online retailer Skid Retailer.

Surcharges may make accepting credit cards worthwhile.

Surcharging may make it possible for businesses that otherwise wouldn’t be able to absorb processing fees to accept credit card payments. According to a Federal Reserve report, nearly 40 percent of consumers prefer using a credit card for in-person payments; offering this payment method is increasingly part of providing a great customer experience.

Credit card surcharges may improve cash flow.

Credit card surcharges may incentivize customers to pay with a debit card or cash, rather than a credit card. Credit card payments generally take one to three business days to process and settle, whereas debit card payments are processed instantly and cash payments are immediately available in your register.

Did You Know?

Credit card surcharges must appear on the customer's printed or digital receipt as a separate line item, in addition to being disclosed at the point of sale.

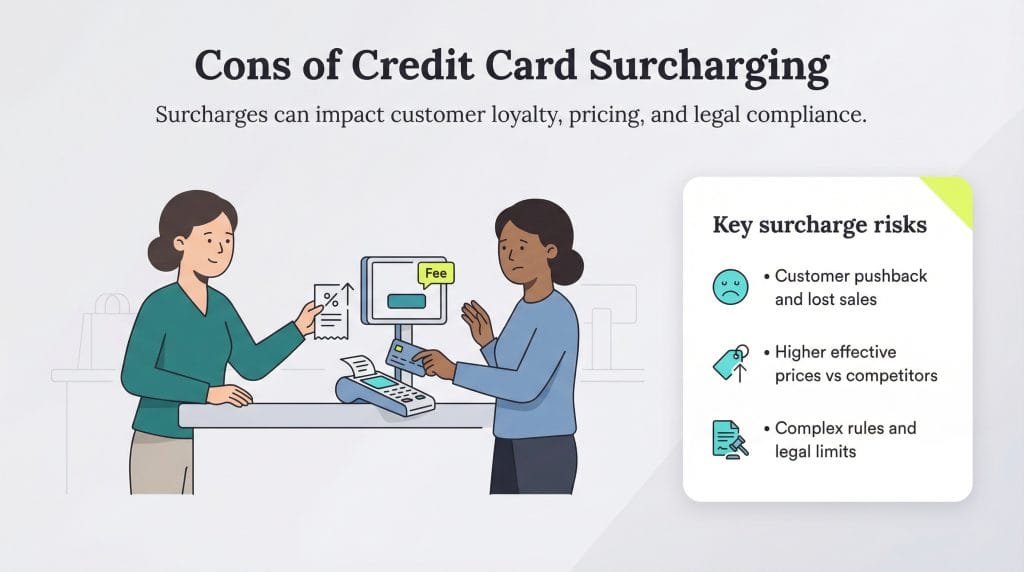

What are the cons of credit card surcharging?

While offsetting credit card fees is a huge advantage for businesses, surcharging has some distinct downsides.

You may lose customers over surcharges.

Customers may dislike surcharges so much that they choose to patronize other businesses instead. A 2024 PYMNTS study found 56 percent of credit card users would likely switch to another merchant if asked to pay a surcharge.

“While it makes sense from a business perspective, customers don’t always see it that way,” said Alicia Collins, founder and CEO of K9 Activity Club. “Some won’t care, some will complain and others will walk away.”

Surcharging raises your effective prices.

If most of your customers pay with a credit card, surcharges effectively increase your prices and put your business at a competitive disadvantage. It’s especially important to consider customer alternatives if you’re competing against online retailers that offer free shipping and fast delivery.

“[It’s] very easy for consumers to compare prices online,” Haverty said. “My strategy is to make up for the credit card surcharge cost in sales volume rather than directly passing the cost on to the buyer.”

In some states, credit card surcharging is illegal or restricted.

Credit card surcharging is prohibited in several states and restricted in others. If you do business in one of these areas, you could face legal trouble for adding a surcharge or doing so improperly, which may result in fines and negative publicity.

Moreover, all states prohibit merchants from profiting from a credit card surcharge. Merchants are also prohibited from adding a surcharge to debit card purchases.

“The merchant must have payment systems that distinguish between credit and debit cards,” Cohen explained. “However, many current point-of-sale systems lack this functionality, creating further challenges.”

FYI

Other credit card processing rules and laws retailers must be aware of include the Payment Card Industry Data Security Standard and the Payment Application Data Security Standard, both of which aim to reduce credit card fraud.

What are the steps to start credit card surcharging?

If you decide to surcharge credit cards, consider the following steps:

Contact your credit card processor: Inform the payment processor of your intent to surcharge. The company may impose specific requirements and restrictions that you must follow.

Reprogram your credit card terminal: Surcharges should appear as a separate line item on customer receipts. This may require the payment processor’s support to alter the terminal’s settings.

Notify the credit card networks: Get in touch with the card networks, such as Visa and Mastercard, at least 30 days before implementing surcharging and follow their rules.

You must meet all surcharging requirements, including the following:

Surcharges may be applied to credit card transactions only.

The surcharge cannot exceed 4 percent of the transaction total (3 percent for Visa) or your actual card processing cost, whichever is lower.

You must inform Visa and Mastercard of your intent to surcharge at least 30 days before doing so.

You must post signage informing customers about the surcharge and stating that it applies only to credit card purchases, not debit card purchases.

Signage must be posted at store entrances and at the point of sale, including online checkout pages.

Surcharges must be displayed as a separate line item on receipts.

“Failure to comply can result in penalties, including fines or suspension of payment processing privileges,” Cohen cautioned. “Staying informed by doing your own research or seeking assistance from an independent third party like Merchant Advocate is critical to avoid costly mistakes.”

Tip

The best credit card processors make surcharging easier by offering transparent pricing, low rates and built-in compliance tools to help you follow surcharge rules without extra hassle.

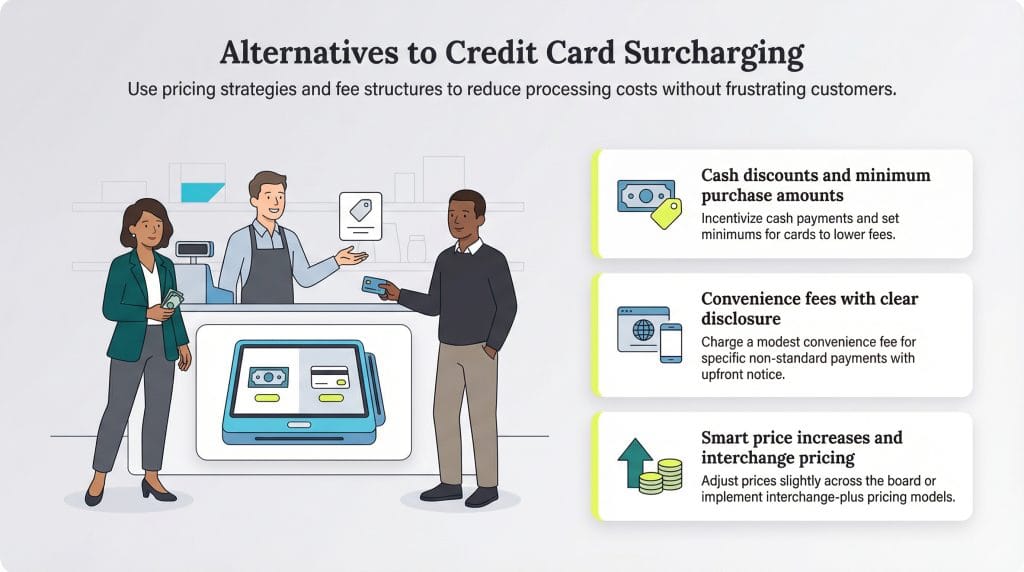

What are alternatives to surcharging?

Surcharging isn’t the only way to reduce credit card processing fees. Consider the following alternatives.

Offer cash discounts.

Price your goods or services as if everyone will pay with a credit card. Then, offer a cash discount for customers who choose not to pay with plastic, instead of adding a surcharge for those who use credit cards.

Establish minimum purchase amounts.

Businesses that pay their processor a percentage plus a flat fee for each transaction may lose money on small sales paid for by credit card. Excluding small purchases from credit card payments with a minimum purchase amount can reduce overall processing fees.

Charge convenience fees.

Businesses can charge a convenience fee when customers use a nonstandard payment method, such as paying with a credit card by phone or online.

Convenience fees typically range from 1.3 percent and 3.5 percent and may have a minimum amount. The rules regarding convenience fees vary by card type.

Visa’s rules regarding convenience fees include the following:

Convenience fees can’t be charged for in-person transactions.

Convenience fees can’t be charged for the general acceptance of Visa cards. Convenience fees must be disclosed before purchase completion.

Convenience fees must be a flat or fixed fee, not a percentage.

Convenience fees cannot be charged on recurring transactions.

You may charge a convenience fee or a credit card surcharge, but not both.

Mastercard’s rules for convenience fees include the following:

Convenience fees must be disclosed as a separate fee for using the payment channel.

Convenience fees may be used for in-person, phone, online, kiosk or mail payments.

Convenience fees can’t be higher than those for other card-based payments.

Convenience fees may be a flat fee or a percentage.

You may charge a convenience fee or a credit card surcharge, but not both.

American Express’s rules for convenience fees include the following:

Convenience fees must be disclosed to the customer.

Convenience fees must be the same for all forms of payment within the same channel (such as phone, online or mail).

Convenience fees may be a flat fee or a percentage.

Convenience fees may be used for in-person, recurring and installment payments.

These rules can change at any time. Check with each card brand for the most current information.

Raise prices.

Although raising prices across the board can result in slightly higher credit card fees, it can also increase your profit margin and help you avoid backlash from card-paying customers who may feel penalized. Before raising prices, consider the competitive landscape and whether raising prices may lead to lost business.

Use a credit card processor with interchange pricing.

Lowering your credit card processing costs benefits both you and your customers. Not all processors charge the same way. While all credit card processors charge the interchange rate — the amount set by card brands like Visa, Mastercard, American Express and Discover — some make their money by charging a flat monthly fee instead of adding a markup on top of the interchange rate.

Tip

If your credit card volume is high, using a processor with interchange pricing can be an effective way to minimize costs. Check out our review of Payment Depot and our Stax review to learn about two credit card processors that use the interchange pricing method.

Credit card surcharge FAQs

To accurately assess the impact of surcharging on your business, compare sales totals before and after implementing the surcharge. If sales drop considerably, the surcharge may be affecting your business.

If you begin surcharging and experience adverse effects, you can reverse the decision and stop surcharging. However, it may be difficult to repair your brand reputation and win back lost customers.

Five states currently prohibit credit card surcharges: California, Maine, Massachusetts, New York and Connecticut. Puerto Rico also bans credit card surcharges.

In addition, some states have limited or complex anti-surcharging laws that may restrict how fees are disclosed or applied. Surcharging regulations change frequently, so always check with your state or legal advisor before adding surcharges to customer transactions.

Surcharges specifically apply to credit card transactions. Convenience fees generally apply to alternative payment methods like keying in a card number over the phone or accepting online payments.

Jennifer Dublino is an experienced entrepreneur and astute marketing strategist. With over three decades of industry experience, she has been a guiding force for many businesses, offering invaluable expertise in market research, strategic planning, budget allocation, lead generation and beyond. Earlier in her career, Dublino established, nurtured and successfully sold her own marketing firm.

At business.com, Dublino covers customer retention and relationships, pricing strategies and business growth.

Dublino, who has a bachelor's degree in business administration and an MBA in marketing and finance, also served as the chief operating officer of the Scent Marketing Institute, showcasing her ability to navigate diverse sectors within the marketing landscape. Over the years, Dublino has amassed a comprehensive understanding of business operations across a wide array of areas, ranging from credit card processing to compensation management. Her insights and expertise have earned her recognition, with her contributions quoted in reputable publications such as Reuters, Adweek, AdAge and others.