Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is a Cyber Insurance Risk Assessment?

Determine your systems' weak points and security gaps when seeking cyber insurance.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Keeping up with the latest security threats can be a full-time job. Bad actors constantly find new ways to infiltrate company servers, databases and websites. The result is lost data, locked systems and ransoms. Cyber insurance is essential to fighting these threats.

However, before getting cyber insurance, you may need to conduct a cyber insurance risk assessment to determine your systems’ weak points. Here’s a look at cyber insurance risk assessments, how to conduct one and more.

What is a cyber insurance risk assessment?

Before you get cyber insurance, your insurance carrier will likely conduct a cyber insurance risk assessment on your company. This assessment aims to identify the risk areas and security gaps your company faces. A cyber insurance risk assessment considers your technology, company protocols and daily employee procedures that may create security risks. “A cyber risk assessment is an objective evaluation of an organization’s cybersecurity posture,” explained Mario Paez, national cyber risk leader at the Marsh McLennan Agency.

Why do you need a cyber insurance risk assessment?

The risk assessment benefits both the insurance carrier and the company it’s assessing. Insurance carriers gain the knowledge needed to underwrite the risk appropriately. A business with many areas that are vulnerable to security breaches will be at higher risk — and incur a higher premium — than a company with fewer issues.

The assessment also benefits the company because the insurer provides a checklist to help label vulnerable areas. With this information, the company can take measures to reduce or eliminate risks. Shoring up exposed systems and processes may prevent hacks and breaches while reducing the premiums the business must pay the insurer.

“Being prepared is essential to minimizing the impact of a potential cyber-related event,” said Rishi Baviskar, global head of cyber risk consulting at Allianz Commercial. “An insurer will conduct a risk analysis to determine the likelihood of events like data breaches as well as a potential for cyberbusiness interruptions.”

How do you conduct a cyber insurance risk assessment?

While an insurance carrier performs the cybersecurity risk assessment, businesses can help the process go smoothly by understanding what the carrier must examine and what systems it must access. “We recommend working with an objective third-party partner to conduct a holistic assessment based on a globally accepted cybersecurity framework, such as NIST CSF and ideally an industry-specific cybersecurity framework that establishes a baseline from which your organization can rank and prioritize next steps for what tools and services to invest in,” said Paez.

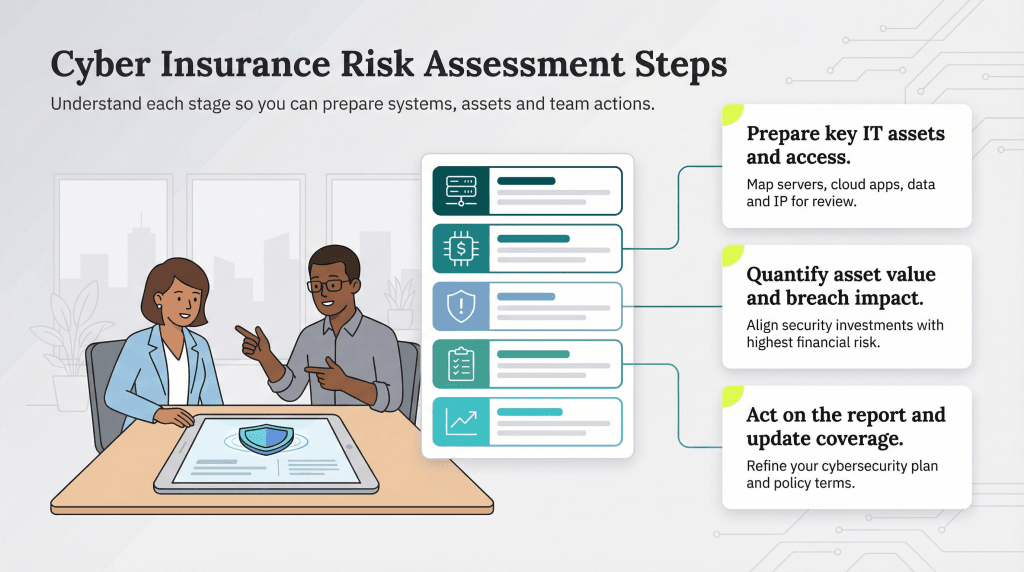

While the sequence of events during a risk assessment may vary by insurer, it will generally follow these five steps:

Initial preparation: Your insurer will start identifying your crucial information technology (IT) and data assets, including servers, cloud-based operations, customer information and intellectual property (IP). This preparation helps the carrier understand the scope of what you’re protecting. [Related article: What Is Intellectual Property Insurance?]

Asset valuation: Your insurance carrier will assign a monetary value to each business asset to quantify the financial impact of a breach or loss. The carrier will consider data recovery fees, IP infringement fees and possible loss of revenue.

Risk analysis: Your insurer will conduct a risk analysis to determine the likelihood of events like data breaches. At this stage, it will consider your current security measures and assess their effectiveness.

Assessment report: When the risk analysis is complete, the insurer will send a risk assessment report detailing each physical and nonphysical asset and highlighting the areas of greatest concern.

Business review: The business will study the assessment report and the insurer’s proposed strategies to protect your company against identified risks. The company may develop or update its cybersecurity plan and inform the insurer of planned actions. During this step, the business and the insurer can discuss potential amendments to their proposed cybersecurity insurance coverage.

“It’s important to set expectations ahead of starting the assessment — the goal should not simply be to conduct the assessment but also to be prepared to act on the baseline review and results from the assessment, which can be one of the more difficult challenges for organizations,” said Paez.

Tip

To protect your business from a data breach, consider physical security measures, such as key cards and improve password security with password-management solutions that help create and store complex passwords.

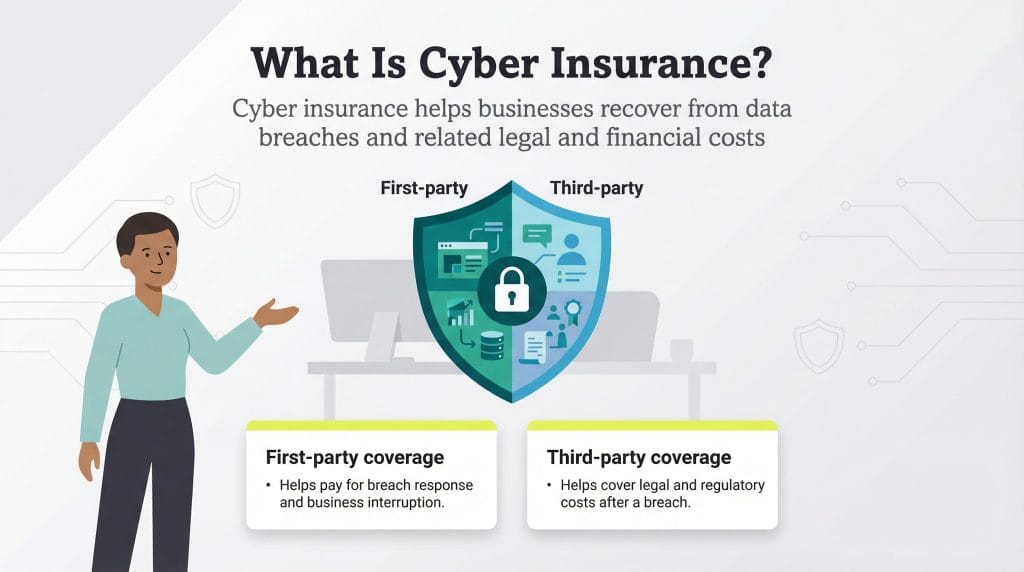

What is cyber insurance?

A cyberpolicy is business insurance that includes first-party and third-party claims. You’d file a first-party claim if your business had hard costs associated with a breach. Other people could file a third-party claim against you, alleging that your company didn’t adequately safeguard personal and private data.

First-party cyber insurance covers the destruction of your property, including the following:

Investigation costs

Repairs to damaged equipment

Lost revenue

Consumer notification costs

Consumer credit monitoring costs

Ransom paid to a hacker to restore files

Third-party cyber insurance covers consumer data liability, including the following:

Legal fees

Settlements and court judgments

Regulatory fines

Picking the right business insurance policy is crucial. Many of the best business insurance providers will provide both first-party and third-party coverage associated with cyberincidents as well as other associated business needs.

What is cyber liability insurance?

Cyber liability insurance is part of a cyber insurance policy. It protects against third-party claims that the business didn’t adequately or effectively secure personal and private data. Employee error and failure to implement safeguards could be listed as the cause of the data breach.

FYI

Cyber insurance provides first-party and third-party claims coverage. In contrast, data breach insurance covers costs such as lost revenue and credit monitoring but not attorney's fees and regulatory fines.

How does cyber insurance help companies mitigate risk?

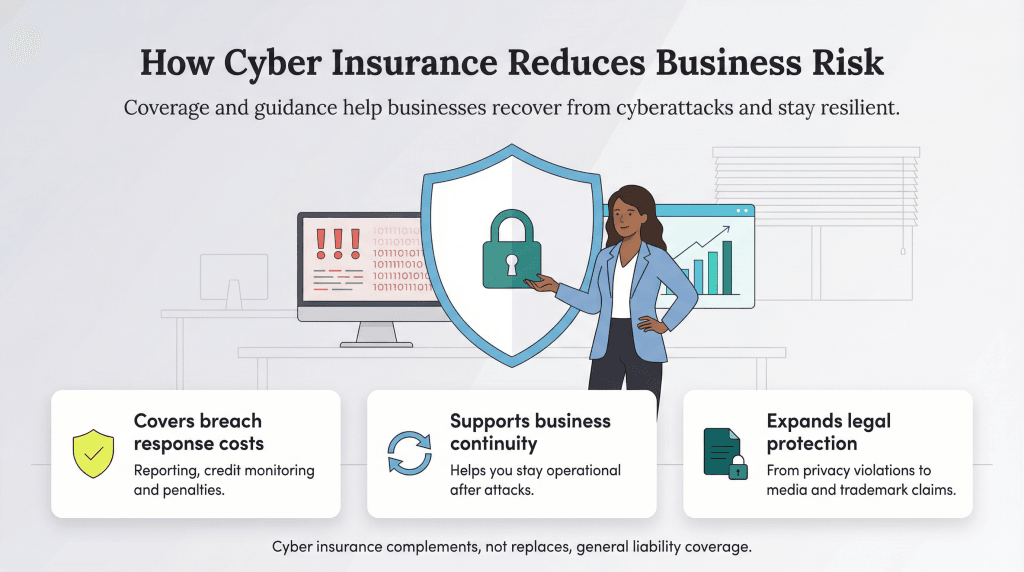

Cyber insurance won’t remove the risk you face from bad actors or employee errors; systems can still be vulnerable and you could experience a loss. However, starting with the cyber insurance risk assessment, you can get a better handle on your most significant risk areas to avoid common business scams or mitigate an incident’s damage.

In addition to providing insight, cyber insurance helps pay for the damages resulting from a data breach. Many businesses wouldn’t be able to handle a security incident’s out-of-pocket costs, such as reporting, credit monitoring and regulatory penalties, or pay a hefty ransom to get their business back up and running. Without cyber insurance, a company would have a challenging time surviving the damages associated with a cyberattack.

Depending upon the policy, noted Paez, cyber insurance can also help:

Businesses remain operational and resilient after an incident

Provide peace of mind

Provide wide-ranging protections for items like privacy right violations, media liability, trademark infringement and more.

Tip

Cyber insurance doesn't replace general liability insurance, which you'll need if your company faces claims of bodily injury or property damage.

FAQs

You have many options when shopping for a cyber insurance policy. Consider the insurance company as a partner in protecting your business from cybercrime. It's wise to work with a company that will provide a cyber insurance risk assessment to help you understand your risk factors. The best liability insurance providers will help you identify your biggest problems and offer solutions to help shore up vulnerabilities. Your carrier is also your partner if and when you must file an insurance claim. Good insurance carriers have expert teams to mitigate losses during a crisis. For example, in a ransomware attack, your carrier may provide a negotiator or offer technology experts to help shut down your systems or restore them when possible. As you would when choosing any business insurance policy, inquire about exclusions and understand how policy limits work. You may be able to set a retroactive date on a cyber insurance policy. Some policies allow this because insurance carriers understand that you may not be aware of a breach for some time. You'll pay an additional premium for a retroactive date, but this could be well worth it if you haven't previously protected your company from cyber risks.

Your cyber insurance risk assessment should help determine how much cyber insurance you'll need to insure your business adequately. Most small companies start with a baseline policy ranging between $500,000 and $5 million in coverage for each occurrence. The baseline policy usually has a $1,000 deductible, though this varies based on coverage limit. Increase the coverage if you have an extensive database. The more data you keep, the more you become a target and the more exposure you have to higher fines, fees and costs. Businesses with multiple servers or employees who work remotely may also want to consider higher limits.

Consider your reliance on technology to store data, process orders and conduct business. If you'd be unable to operate if your computer systems were hacked or can't afford the costs associated with a data breach, you need cyber insurance. Ransomware attacks are rampant and hackers target companies of all sizes. It's often easier for hackers to breach smaller companies and hold their operations hostage. Don't wait for a problem before you consider getting a policy and shoring up your defenses with a cyber insurance risk assessment.

Risks: In cybersecurity, a risk refers to the likelihood and impact of a successful breach of your IT systems that could result in damage or loss of business data or assets. For example, how likely is it that someone could gain unauthorized access to your network?

Threats: A threat is an action that can lead to a breach, such as a phishing attempt from an external attacker.

Vulnerabilities: A vulnerability refers to a weakness in your cyberdefenses that a cybercriminal could exploit. For example, a team member may not be well-trained enough to spot a phishing email. If they received an email purporting to be from a member of the IT team asking for their security credentials to log in to your network, they may not realize they should investigate the request further before complying. Vulnerabilities can also be technical, such as poor network configuration or unpatched software.

Liabilities: In cybersecurity insurance, a liability describes the costs you might be responsible for meeting to cover expenses that third parties, such as customers, have incurred due to a data breach. Liabilities can include regulatory fines, legal fees and other related expenses.

Jeremy Bender and Mark Fairlie contributed to this article.

Kimberlee Leonard is an insurance expert who guides business owners through the complicated world of business insurance. A former State Farm agency owner herself, Leonard started her decades-long career as a financial consultant advising on investment strategies before switching her focus to insurance and risk mitigation for businesses.

At business.com, Leonard covers topics related to business insurance, such as workers' compensation rates, professional negligence, insurance riders, hold harmless agreements and more.

Leonard has developed insurance primers on everything from small business insurance costs to specific policies, such as excess liability insurance. She has also reviewed business software tools, analyzed employee retirement plan providers and continues to share insights on financial topics as they relate to business. Leonard's work has been published in Forbes, U.S. News and World Report, Fortune, Newsweek and other respected outlets.