Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Everything You Need to Know About Cash Flow Statements

This financial document provides insight into your business's cash flow and financial health.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Cash flow is, understandably, one of a company’s most significant concerns. To stay on top of this vital financial metric, business owners rely on accurate, consistent cash flow statements. These documents provide a comprehensive understanding of how money moves in and out of a business, highlighting income sources and areas of expenditure. By reviewing cash flow statements regularly, business owners can better manage finances, anticipate cash shortages and make informed decisions for growth. We’ll explain more about cash flow statements and how organizations can best use this essential accounting report.

What is a cash flow statement?

Editor’s note: Looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

A cash flow statement – also called a statement of cash flows – is a core financial report that tracks the inflows and outflows of cash within a business over a specific period. Unlike other financial statements that rely on accrual accounting, the cash flow statement reveals actual cash transactions, showing the current business liquidity. Common financial activities, such as applying for a business loan or presenting an idea to business investors, often require cash flow statements and other financial reports.

According to Robert Reynolds, chief financial officer and chief operating officer of Tersa, the cash flow statement is a critical tool for small businesses. “It represents the financial ‘oxygen’ a business needs to survive,” Reynolds told us. “As a startup executive, I find our cash flow statement to be the most important report, as cash is vital for navigating daily operations and growth.”

Bottom Line

Preparing a cash flow statement is a crucial way to evaluate a business's financial health and provide a comprehensive picture of how the company spends and invests its money.

Why it’s vital for financial health

More than 80 percent of small business failures are due to cash flow problems, making the cash flow statement an essential tool for financial survival. In the short term, insufficient cash flow can prevent a business from paying its bills. In the long run, it can stop your business from achieving profitable growth. Investors and lenders carefully scrutinize cash flow statements before doing business with you and many financial activities and analyses rely on accurate cash flow reporting.

The cash flow statement provides critical insights into three key areas of financial health:

Liquidity: The cash flow statement helps determine whether a company can cover its short-term obligations and maintain day-to-day operations. Positive operating cash flow indicates the business has enough liquidity to pay expenses, suppliers and employees without relying on external financing.

Solvency: It provides insight into the company’s long-term financial stability by showing how much cash is available to repay debts and fund essential investments. Strong, consistent cash inflows from operations enhance solvency and reduce dependence on borrowing or asset sales.

Trend analysis: Reviewing cash flow patterns over multiple periods allows businesses to identify trends in cash generation and consumption. Recognizing these patterns helps management forecast future needs, adjust spending and develop sustainable strategies for maintaining cash balance and growth.

Consider the following critical ways cash flow statements are used.

Cash flow statements help you predict incoming revenue.

A proper cash flow statement accurately reflects the timing of expected revenue. For companies that receive immediate payment, such as e-commerce or retail stores, this involves using sales forecasts to estimate cash inflows. For companies that extend credit to clients or provide services, such as consulting firms, it requires estimating both when a sale will be made and when payment will be received. These forecasts should be updated continually as new data becomes available to maintain accuracy.

Aileen Wigotow, certified public accountant (CPA) and owner of Friday Financials, offered the following example: “Let’s say a business’s profit and loss (P&L) statement reports $50,000 in revenue from clients for a given period. The cash flow statement might show that only $25,000 of that revenue was actually received, putting the business in a negative cash flow position for that period.”

Wigotow explained that business owners can use this information to plan for the following month or consider offering a small discount to clients for early payment to help collect more revenue in the same period it was earned.

Cash flow statements can help you decide when to ramp up sales and marketing.

If the cash flow statement shows a dip in forecasted revenue, the company can take action to increase revenue. For example, it could announce additional employee bonuses to salespeople who hit short-term sales targets or run a promotion to unload excess inventory.

The cash flow statement will inform management about what marketing or sales-boosting tactics are best at the time. Here are some examples:

Low cash outlook: In a very low cash outlook, the company might focus on performance-based methods, such as affiliate marketing, sales commission bumps or bonuses to be paid later.

Forecasted low cash flow: If the cash situation is OK now but is expected to get worse, the company might opt to spend some money on digital marketing strategies to generate sales leads that will close when needed.

Cash flow statements let you know when to focus on collections.

When many accounts receivable (AR) are late and causing a cash flow problem, you’ll know it’s time to focus on collection strategies. Depending on your situation, you may do one or all of the following to improve cash flow:

Turn to collection agencies or attorneys for help.

Cash flow statements help you decide when to pay larger bills.

When the company has cash in hand, it can decide when to pay larger bills to vendors with credit lines or payment terms. When the company is flush with cash, payments can be made immediately to ensure products or raw materials continue to flow. Conversely, payment can be delayed or the company could even renegotiate its terms during a slow period.

Cash flow statements can indicate when a loan is needed.

If your business is profitable on paper but short on cash flow, your cash flow statement will help determine if you need short-term financing, such as a bridge loan. In this situation, your business may be a strong candidate for a lender and the funding can help you cover expenses until revenue from sales starts flowing in. The cash flow statement also indicates how much to borrow so you avoid paying interest on funds you don’t need.

Tip

The best business loans can help you cover temporary cash flow difficulties and keep operations running smoothly until revenue picks up.

Cash flow statements can help indicate if your startup needs an investor.

Startup businesses should create cash flow statements as part of their pro forma financial documents. These statements outline the business’s startup costs, the founders’ investments and any shortfalls. If a shortfall is identified, you may consider seeking funding from an angel investor or venture capitalist to bridge the gap.

Understanding the three sections

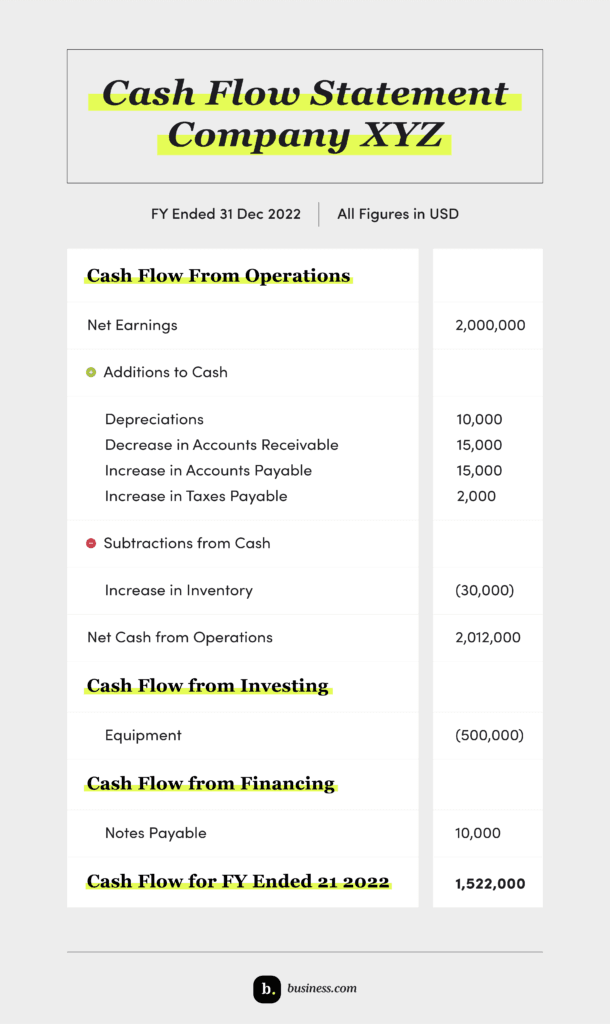

The statement of cash flows is broken down into three key sections that collectively provide a comprehensive view of a company’s cash flow status.

Operating activities: Often referred to as “cash from operating activities,” this section is typically first. It covers the incoming cash from sales or contracts and the outgoing payments for operational expenses, such as overhead costs, taxes, staff or manufacturing costs.

Investing activities: The investing section records capital expenditures, acquisitions and divestments. Expenditures and acquisitions are both cash outflows while divestments are cash inflows. It’s not unusual for this section to primarily consist of cash outflows, as many thriving businesses spend more money investing than cashing out investments.

Financing activities: This section details how your company is funded and distributes its funds. Data in this portion may include debt transactions (incoming loan proceeds and outgoing loan payments) and equity. If your company pays dividends to shareholders, you would capture that here.

FYI

You may experience low or negative cash flow when opening another business location or otherwise growing your company. Consider investments or loans to cover expenses until your revenue catches up.

Direct vs. indirect method – what’s the difference?

To calculate your business’s cash flow, start by adjusting your net income using information from your balance sheet and P&L statement. Adjustments are made to account for noncash items included in net income, such as revenue, expenses and credit transactions. Both methods (direct and indirect) yield the same net cash flow but they differ in presentation, the information required and transparency.

Consider the following methods and adjustments used to calculate cash flow.

The Financial Accounting Standards Board prefers this method because it shows the actual flow of cash in and out of a business. The direct method uses real-time figures and considers only cash flow to show actual payments and receipts. Instead of starting with net income, it lists cash inflows and outflows to core business operations. To calculate, start by analyzing all cash payments and receipts using your accounts’ beginning and ending balances.

Cash transactions are grouped by type:

Operating cash flow: Cash received from customers, cash paid to suppliers and other operating expenses, such as salaries, rent and raw materials:

Cash received from customers = Sales + decrease or – increase in AR

Cash paid to suppliers = Cost of goods sold + increase or – decrease in inventory + decrease or – increase in accounts payable (AP)

Cash paid for operations = Operating expenses + increase or – decrease in prepaid expenses + decrease or – increase in accrued liabilities

Financing cash flow: Interest payments received and interest paid

Cash interest = Interest expense – increase or + decrease in interest payable + amortization of bond premium or – discount

Taxes cash flow: Income tax refund received and income tax paid (sales tax received and paid should be equivalent)

Cash for income taxes = Income taxes + decrease or – increase in income tax payable – income tax refund

Other cash flow: Any other cash received, such as investment capital

The direct method provides clearer visibility of cash movements and is preferred under International Financial Reporting Standards (IFRS), though it is rarely used in practice. This is because it is more complex and requires detailed cash tracking. The direct method is most appropriate for small businesses without significant cash transactions or cash-heavy industries when IFRS compliance is required.

Indirect cash flow method

This method starts with net income from your income statement. It only accounts for revenue earned, then adjusts net income for noncash items and changes in working capital that impact cash flow. Transactions that do not affect cash flow, such as depreciation, are added back.

The formulas for the indirect method are:

Cash flow from operations = Net income + depreciation and amortization + AR + inventory + AP

Net change in cash balance = Operating cash flow + investing cash flow + financing cash flow

Cash balance at the end of the period = Net change in cash balance + cash balance at the start of the period

The indirect method is easier to prepare with minimal effort because most organizations keep their records on an accrual basis. It uses existing financial statements and is accepted by both IFRS and Generally Accepted Accounting Principles (GAAP), making it widely used by companies, especially large corporations. However, the indirect method is less transparent than the direct method as it requires accrual accounting adjustments.

Preparing and analyzing a cash flow statement requires systematic steps to ensure accuracy and meaningful insights. Here’s a step-by-step approach:

Gather the data.

Start by collecting all necessary financial documents, including the income statement, balance sheet and transaction records. These documents provide the foundation for calculating cash flows across all three sections. For companies using accrual accounting, ensure accounts receivable, accounts payable, inventory levels and prepaid expenses are current.

The basic formula is: Cash Received – Cash Paid Out = Ending Cash Balance.

Select the method.

Choose between the direct or indirect method based on business needs and complexity. Small businesses with straightforward transactions may benefit from the direct method’s transparency, while larger organizations typically use the indirect method due to its compatibility with existing accrual-based accounting systems.

Analyze the results.

Once the cash flow statement is prepared, analyze the results to understand the business’s liquidity position and cash generation capability. Look for patterns across the three sections to identify whether the business generates sufficient cash from operations or relies heavily on financing.

Cash flow statement vs. income statement & balance sheet

While the statement of cash flows shows how much money is moving in and out of the business during a specified period, it’s the critical link between the income statement and balance sheet.

Cash flow statements: Cash flow statements show how and when cash flows into and out of a business. The amount of cash you have on hand determines your ability to invest, pay bills and assess whether you need to focus on generating additional revenue.

Income statement: Income statements reveal a company’s profit (or loss) in a given period. They include AR on the income side, even if that money has not yet been collected and AP on the expense side, even if it hasn’t yet been paid. The income statement also includes depreciation expense, which is not an actual cash expense but rather a portion of the original cost of a business asset, such as equipment, that is deducted over time as it becomes older and less valuable.

Jackie Rockwell, co-founder of Brass Jacks, an online bookkeeping academy, explained that while cash flow statements allow companies to see actual cash changes over a given period, income statements don’t reveal the same information. “If the company is using credit cards, loans or sends invoices that get paid in a later period, the numbers on the income statement may not represent the actual money that has changed hands,” Rockwell noted.

Balance sheets: Balance sheets show the company’s financial position by representing its overall value. Value is determined by subtracting liabilities (what the company owes) from assets (what the company owns). The result or value of the company is the shareholders’ equity. Cash on hand and AR are counted among the assets, while AP is one of the liabilities. Other assets include real estate, vehicles and equipment that are already paid for and, therefore, do not have an associated ongoing cash payment.

Quick reference table – cash flow at a glance

Section

Purpose

Key Components

Operating Activities

Shows cash generated or used in day-to-day business operations

Cash from customers, payments to suppliers, salaries, rent, taxes

Investing Activities

Records capital expenditures and long-term investments

Purchase/sale of property, equipment, securities; acquisitions and divestments

Financing Activities

Details how the company is funded and distributes funds

A cash flow statement is a financial document that shows how cash moves in and out of a business over a specific period, tracking actual cash transactions from operating, investing and financing activities to provide a clear view of liquidity and financial health.

Use the cash flow statement to monitor whether the business generates sufficient cash from operations to cover expenses, assess liquidity for meeting obligations and identify trends by comparing statements over time to anticipate future cash needs and make informed financial decisions.

Net income is the bottom line on the income statement showing profit after expenses during a period, while cash flow shows only the changes in cash balances from one period to the next; net income includes noncash items like accounts receivable and depreciation, whereas cash flow reflects actual cash transactions.

Jennifer Dublino is an experienced entrepreneur and astute marketing strategist. With over three decades of industry experience, she has been a guiding force for many businesses, offering invaluable expertise in market research, strategic planning, budget allocation, lead generation and beyond. Earlier in her career, Dublino established, nurtured and successfully sold her own marketing firm.

At business.com, Dublino covers customer retention and relationships, pricing strategies and business growth.

Dublino, who has a bachelor's degree in business administration and an MBA in marketing and finance, also served as the chief operating officer of the Scent Marketing Institute, showcasing her ability to navigate diverse sectors within the marketing landscape. Over the years, Dublino has amassed a comprehensive understanding of business operations across a wide array of areas, ranging from credit card processing to compensation management. Her insights and expertise have earned her recognition, with her contributions quoted in reputable publications such as Reuters, Adweek, AdAge and others.