Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is General Ledger Accounting?

Learn how general ledger accounting can help you gauge your business's overall financial health.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

As a busy business owner, you may not have much interest in basic accounting principles, such as maintaining a general ledger. While most accounting activities are best left to your accountant, understanding what a general ledger is and how it works can be beneficial.

Maintaining a general ledger is one of the best ways to gauge your business’s overall financial health. It also helps ensure you’re not making any typical accounting mistakes that could cost you time and money down the road.

Editor’s note: Looking for the right accounting software for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

What is a general ledger?

A general ledger is a record of a company’s financial transactions. General ledger accounting summarizes and sorts a company’s financial information. Most businesses track this financial accounting data with accounting software.

“A general ledger is a master record that contains all the accounts used by a company or organization,” explained Max Avery, co-author of Wealth in Numbers and chief business development officer at Digital Family Office. “These accounts include assets, liabilities, equity, revenue and expenses.”

A general ledger includes the following:

Revenue: Revenue is the money earned from the sale of a company’s products or services. In accrual accounting, unlike cash accounting, companies must record revenue when it’s earned, not when it’s received.

Expenses: Expenses are anything your business spends money on, including payroll, rent and marketing. A combination of fixed and variable expenses determines your business’s overall profitability.

Assets: Business assets are anything of value your business owns. Asset ledgers typically have subaccounts. The larger the company, the more complex the asset ledger will be.

Liabilities: An accounting liability is anything your company owes. The liability account is where your company records things like debt, customer prepayments and deferred income taxes.

Equity: Equity is the owner’s interest in a company’s assets. Calculate your equity by subtracting your company’s liabilities from its assets.

Avery explained that a general ledger outlines all transactions and sorts them by type. “For instance, if a company purchases a new piece of equipment, that transaction will be recorded in the general ledger under the asset account for equipment,” Avery noted. “If the company takes out a loan, it will be recorded in the liability account.”

Companies use general ledger data to compile their financial statements and track business performance.

Tip

Payroll journal entries are a crucial part of general ledger accounting, ensuring that wages, taxes and deductions are accurately recorded.

How is a general ledger used in accounting?

Businesses use general ledgers as part of the accounting process. Without a detailed general ledger, your accounting can quickly become disorganized and inaccurate. Inaccurate financial records cause significant problems down the road.

A general ledger provides the information necessary to create a balance sheet or cash flow statement and gives a quick overview of your organization’s financial health. A general ledger also creates a comprehensive audit trail, which will be helpful if you ever face a tax audit.

“The general ledger is essentially the backbone of any accounting system,” explained Dana Ronald, president of the Tax Crisis Institute. “It’s where all the financial transactions of a business are compiled — think of it as the master file that records everything. Every expense, every sale and every transfer is logged in the general ledger, forming the basis for the business’s financial reports. It provides a clear, organized record that keeps you aware of your income, expenses, assets and liabilities.”

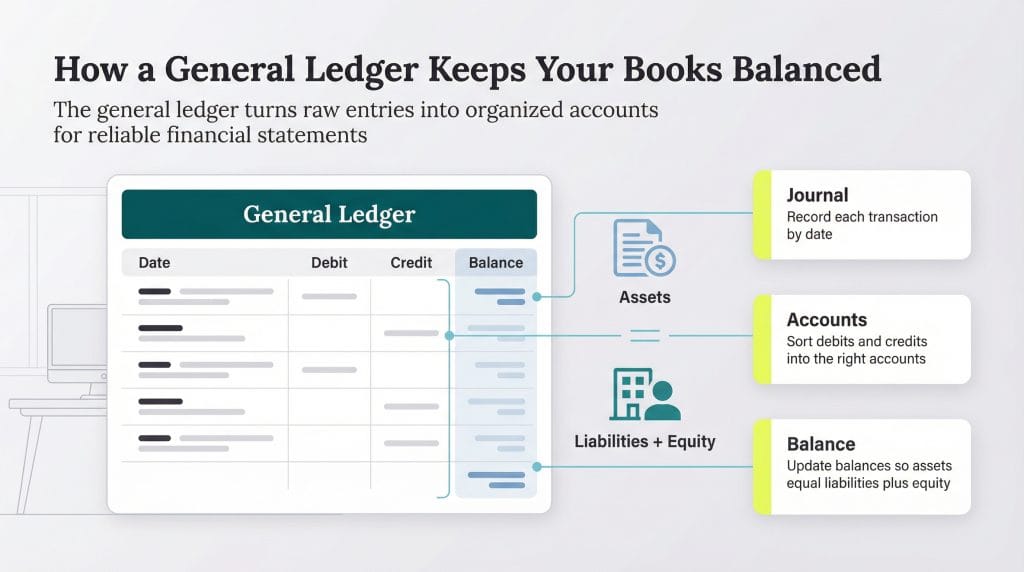

General ledger components

There are four primary components of a general ledger:

Journal: The journal contains raw accounting entries, recorded sequentially by date.

Description: Each transaction includes a brief description.

Debit and credit columns: Every transaction in the general ledger is classified as either a debit or credit.

Balance: The balance must be updated each time a new debit or credit is posted. This practice ensures financial records remain accurate and current.

Using a general ledger

To get started, create a journal and record each business transaction as it occurs. Ensure each transaction is assigned to the correct account. Once your journal is complete, transfer the data to the general ledger.

A general ledger takes information from the journal and categorizes it into the appropriate accounts. Each entry may also include subaccounts to provide further transaction details.

For instance:

If recording an asset, subaccounts may include savings, inventory or accounts receivable.

If recording revenue, subaccounts could include product sales or miscellaneous income.

Did You Know?

If you hire a bookkeeper for your business, maintaining a general ledger will be one of their primary duties, along with balancing the books, creating invoices and handling payroll.

General ledgers and double-entry bookkeeping

Double-entry bookkeeping states that every financial transaction affects a company’s finances in two ways. The following equation summarizes this concept:

Liabilities + Equity = Assets

In a double-entry system, a company’s total assets must equal the sum of its liabilities and the owner’s equity. This ensures that the balance sheet stays balanced every time and that each debit has a corresponding credit.

“Double-entry bookkeeping is a system built for accuracy,” Ronald said. “Every transaction has at least two entries: a debit in one account and a credit in another, ensuring everything balances — what comes in equals what goes out. For example, buying business equipment means debiting the equipment account (asset) and crediting the cash account. This balance adds consistency and reliability to your financial records.”

The key principle of double-entry bookkeeping is that every transaction affects at least two accounts. For example:

If a business takes out a $500,000 loan, that loan is recorded as a liability but also increases total assets.

If a business purchases inventory, that inventory increases assets while reducing cash.

Double-entry bookkeeping ensures the business maintains accurate records with a corresponding relationship between each liability and asset.

What do general ledgers tell you?

General ledgers help generate financial statements for financial institutions or stakeholders. They can also help you understand and track your business’s finances. Here are a few ways they do this:

General ledgers prepare a trial balance. Preparing a trial balance means adding debits and credits to ensure both columns match. This practice ensures your books are accurate and free from mathematical errors. Most companies prepare a trial balance at the end of each reporting period. “General ledgers are powerful tools for analysis,” Ronald noted. “They help you prepare a trial balance to ensure your debits and credits match. They offer a clear view of your business’s financial health — monitoring cash flow, spotting trends and identifying discrepancies.”

General ledgers provide an overview of your business finances. A general ledger gives an overview of your business’s financial activity over a specific period. You can analyze financial trends over the past year or focus on a shorter period, such as the past 90 days. “It provides an overview of a business’s finances by showing the current balances of each account,” Avery explained. “This allows business owners and managers to see where their money is coming from and going, helping them make informed decisions about their operations.”

General ledgers make it easier to spot problems. One of the most significant benefits of using a general ledger is that it becomes easier to spot financial problems in your business. For instance, if your expenses have been significantly higher over the past year, reviewing your general ledger can help you uncover the cause.

FYI

Posting transactions to your general ledger is part of the accounting cycle. The accounting cycle is a set of steps used to identify and maintain your business's transaction records.

Example of a general ledger entry

A general ledger is used to record your business’s financial transactions. Here are some examples of common general ledger entries:

Deposits to a checking or savings account

Incoming revenue from product sales

Recent inventory purchases

Office supply orders

Payroll checks

Estimated quarterly state and federal tax payments

Business insurance payments

Here is an example of what a general ledger entry would look like:

Date

Transaction number

Transaction

Debit

Credit

1/15/26

1001

Office Supplies

$350

BLANK

1/15/26

1001

Cash

BLANK

$350

2/1/26

1002

Accounts Receivable

$5,500

BLANK

2/1/26

1002

Sales Revenue

BLANK

$5,500

2/28/26

1003

Salaries Expense

$8,200

BLANK

2/28/26

1003

Cash

BLANK

$8,200

3/10/26

1004

Cash

$5,500

BLANK

3/10/26

1004

Accounts Receivable

BLANK

$5,500

3/22/26

1005

Equipment

$12,000

BLANK

3/22/26

1005

Accounts Payable

BLANK

$12,000

4/5/26

1006

Rent Expense

$2,400

BLANK

4/5/26

1006

Cash

BLANK

$2,400

As shown in this example, purchasing inventory impacts both the debit and credit columns. The inventory purchase increases assets (debit), while cash decreases (credit) to reflect the transaction.

How accounting software can help manage your general ledger

“Using accounting software to manage a general ledger boosts efficiency and accuracy,” Ronald noted. “It automates tasks, reduces errors and ensures compliance with standards. Advanced tools also generate real-time reports, perform analytics and integrate with other systems for smooth financial management.”

When choosing accounting software, ensure the solution supports general ledger accounting. Here are some excellent options:

QuickBooks Online: QuickBooks Online is a popular all-in-one accounting solution that supports general ledger reports. The software also simplifies payroll automation, batch transactions and running trial balances. Read our QuickBooks Online review for more information about its features and pricing.

FreshBooks: With FreshBooks, you can track revenue and expenses and create a trial balance to ensure everything adds up. The reports you generate may not be as detailed as with other software, but FreshBooks will create a basic general ledger report. Learn more in our FreshBooks review.

Xero: Xero’s accounting software makes sending invoices, receiving payments and managing your cash flow easy. Xero lets you run multiple reports, including a general ledger report. You can create a general summary of your account’s activity and balances or run a General Ledger Detail Report, which shows each transaction within those accounts. Our detailed Xero review explains more about this solution’s functionality.

“Accounting software automates the double-entry bookkeeping process, making it easier and less time-consuming to record transactions,” Avery explained. “Accounting software also allows you to generate financial reports instantly, giving you a real-time view of your business’s financial performance. [Many] programs offer features such as budgeting and forecasting, helping you make strategic decisions based on your financial data.”

Tip

Check out our detailed reviews of the best accounting software to find a financial solution that fits your business's needs and budget.

FAQs

The following transactions are commonly recorded in a general ledger:

Income from product sales

Cash spent on office equipment

Quarterly tax payments

Recent payroll expenses

A general ledger helps you maintain financial transparency by keeping detailed records of all your business's financial transactions. It ensures all expenses, revenues and adjustments are accurately documented. Financial transparency is essential for compliance, stakeholder trust and tax audits.

A general ledger and a balance sheet track similar information but serve different purposes.

A general ledger records every financial transaction from the first day you go into business. It maintains a complete, detailed history of all transactions.

A balance sheet does not provide transaction-level details. Instead, it offers a snapshot of a company's financial health over a specific period.

The primary purpose of a balance sheet is to provide an overview of a company's assets and liabilities. Because of this, balance sheets are often used to determine whether a company gets approved for a small business loan.

A general ledger tracks business transactions and relevant accounts. Most companies use a general ledger to create their financial statements. It is responsible for tracking the business's expenses, liabilities, revenue, assets and capital.

In contrast, a general journal records a company's business transactions. It often includes detailed information about each transaction and is used as a temporary record.

Jamie Johnson has spent more than five years providing invaluable financial guidance to business owners, leading them through the financial intricacies of entrepreneurship. From offering investment lessons to recommending funding options, business loans and insurance, Johnson distills complex financial matters into easily understandable and actionable advice, empowering entrepreneurs to make informed decisions for their companies. As a business owner herself, she continually tests and refines her business strategies and services.

At business.com, Johnson covers accounting practices, budgeting, loan forgiveness and more.

Johnson's expertise is also evident in her contributions to various finance publications, including Rocket Mortgage, InvestorPlace, Insurify and Credit Karma. Moreover, she has showcased her command of other B2B topics, ranging from sales and payroll to marketing and social media, with insights featured in esteemed outlets such as the U.S. Chamber of Commerce, CNN, USA Today, U.S. News & World Report and Business Insider.