Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Insurance Considerations When Buying Another Business

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Buying another business is one of the most complex transactions a small business owner can undertake. The due diligence process spans financial records, legal obligations, employee matters, customer contracts and operational systems. Insurance is a critical part of that due diligence, but it’s one of the areas often addressed too late in the process — or not thoroughly enough until a problem surfaces after closing.

When you buy a business, you’re not just acquiring its assets, customers and revenue streams. Depending on how the deal is structured, you may also be acquiring its liabilities, including latent claims from events that occurred before you took ownership. Gaps in insurance coverage during the ownership transition can leave you exposed at the worst possible moment, and inherited risks that weren’t identified before closing can generate costs you never anticipated.

This guide walks through the insurance considerations that apply at every stage of a business acquisition: pre-closing due diligence, the closing itself and post-acquisition integration. Whether you’re buying a competitor, opening a new location or buying a business in a new market, these considerations should be part of your acquisition planning from the beginning.

Why insurance matters in a business acquisition

Insurance matters in an acquisition for three fundamental reasons:

The deal structure determines which historical liabilities transfer to you and which remain with the seller. Getting this wrong can mean inheriting claims and costs you didn’t know existed.

Coverage gaps during the ownership transition can leave you operating an unfamiliar business with inadequate protection during the period when your risk is highest.

The seller’s insurance history — their claims record, experience modification rate and current coverage adequacy — directly affects your insurance costs and options after closing.

Insurance due diligence should begin at the same time as financial and legal due diligence, not as an afterthought once the deal terms are set. Issues discovered late in the process can affect the deal’s valuation, alter the negotiation dynamics or reveal risks that fundamentally alter the acquisition’s economics.

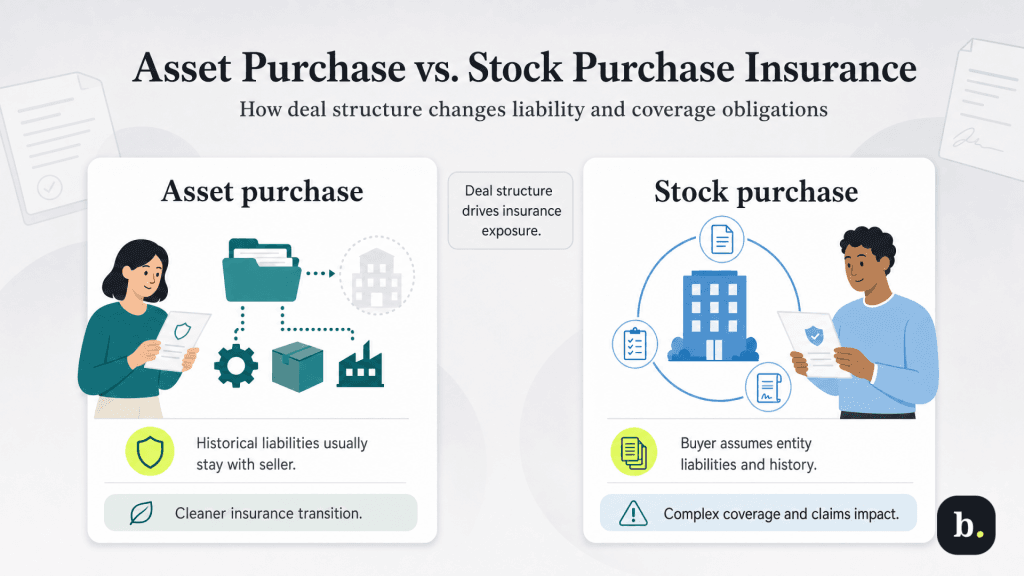

Asset purchase vs. stock purchase: insurance implications

The structure of the acquisition — whether it’s an asset purchase or a stock (entity) purchase — is the single most important factor in determining your insurance exposure. The two structures create fundamentally different liability profiles for the buyer.

Asset purchases

In an asset purchase, the buyer acquires specific assets of the business — equipment, inventory, customer lists, intellectual property, the lease and other named assets — but doesn’t acquire the legal entity that owns them. The seller’s company continues to exist as a separate legal entity, and, generally, the seller’s historical liabilities remain with that entity rather than being transferred to the buyer.

From an insurance perspective, asset purchases are usually cleaner for the buyer. The seller’s existing insurance policies don’t transfer to you — they remain with the seller’s entity and are typically canceled after the sale. You set up new insurance policies in your own name, covering the acquired assets and operations from the closing date forward. Claims arising from events that occurred before the sale are the seller’s responsibility under their own policies, not yours.

However, there is an important exception to be aware of. In some jurisdictions and circumstances, successor liability doctrines can hold the buyer responsible for certain pre-acquisition liabilities even in an asset purchase. Product liability is the most common area where successor liability applies. If the acquired business manufactured or sold a defective product before the acquisition, the buyer may face claims related to that product after closing. Environmental liability is another area where successor liability risk exists, particularly when the acquired business operated on potentially contaminated land. Discuss successor liability exposure with your attorney as part of the acquisition planning process.

Did You Know?

Environmental liability is one type of insurance risk that may not always be top of mind. Others include leadership risks and third-party risks.

Stock or entity purchases

In a stock or entity purchase, the buyer acquires the entire legal entity — the company itself, with all its assets, contracts, obligations and liabilities. The entity continues to exist under new ownership. From the outside world’s perspective, nothing has changed except who owns the company.

The insurance implications of a stock purchase are significantly more complex than those of an asset purchase. Historical liabilities are transferred with the entity, meaning you inherit potential claims arising from events that occurred before you took ownership. The seller’s existing insurance policies may remain in force since the entity that owns them still exists, but many policies contain change-of-ownership provisions that may trigger cancellation, require insurer notification and consent, or void coverage if the ownership change isn’t properly disclosed.

You also inherit the entity’s claims history, which directly affects your future premiums and underwriting. For workers’ compensation, the entity’s experience modification rate (EMR) transfers with it. If the seller had a poor safety record and an elevated EMR, that elevated rate becomes your rate after closing, increasing your workers’ comp costs immediately.

The following table summarizes the key insurance differences between the two deal structures.

Consideration

Asset Purchase

Stock/Entity Purchase

Historical liabilities

Generally remain with seller’s entity (exceptions for successor liability)

Transfer to buyer with the entity

Seller’s policies

Do not transfer; buyer sets up new policies

May continue but require insurer notification; change-of-ownership provisions may apply

Claims history

Stays with seller’s entity

Transfers with the entity; affects buyer’s future premiums

Workers’ comp EMR

Does not transfer (buyer starts with own EMR)

Transfers with the entity

Due diligence depth

Standard; focused on coverage for acquired assets going forward

More extensive; must evaluate all historical liabilities and existing coverage

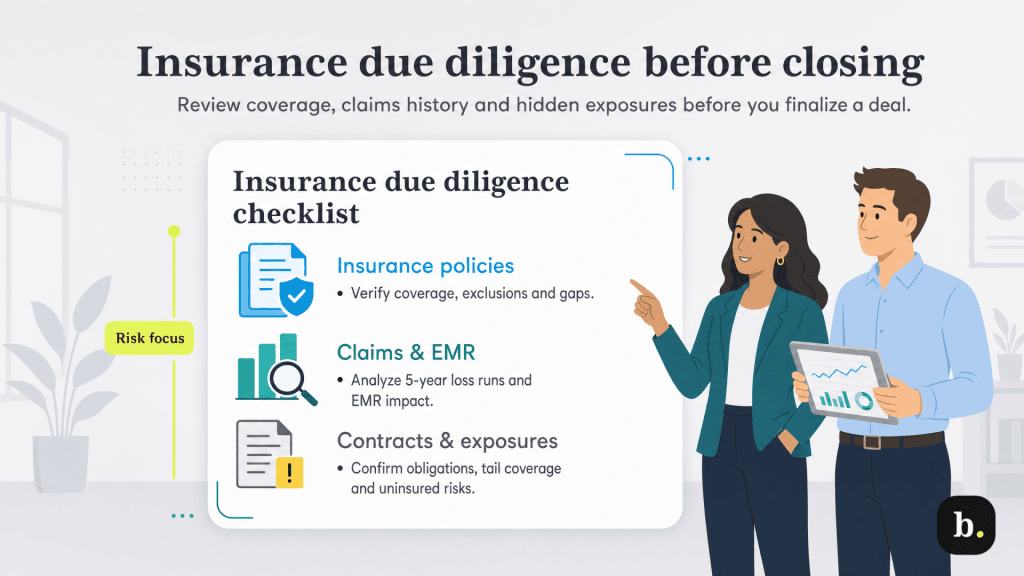

Insurance due diligence before closing

Thorough insurance due diligence before closing an acquisition protects you from inheriting undisclosed liabilities, operating with inadequate coverage and encountering costs you didn’t anticipate. The following actions should be part of every acquisition due diligence process.

Review the seller’s current insurance policies.

Request copies of all active insurance policies the seller carries, such as:

For each policy, review the coverage type, carrier, policy period, limits, deductibles, named insureds, and any insurance endorsements or exclusions. Look for gaps in the seller’s current coverage that would need to be addressed immediately upon acquisition. If the seller doesn’t carry cyber liability insurance despite handling customer data, or lacks employment practices liability insurance (EPLI) despite having employees, those are exposures you’ll inherit the moment you take ownership. Also check for any endorsements, exclusions or conditions that could limit coverage for known risks — an exclusion for a specific type of claim or operation may indicate a past issue the seller hasn’t fully disclosed.

Review the seller’s claims history.

Request loss runs from each of the seller’s insurance carriers covering the past five years. Loss runs are the insurance equivalent of a credit report — they detail every claim filed against the business, including dates, descriptions, amounts paid and amounts held in reserve for open claims.

A pattern of frequent or severe claims is a red flag. It may signal underlying operational problems that increase risk, affect your future premiums as the new owner and indicate potential underwriting difficulty when you apply for new coverage. Open claims are particularly important to identify because they represent unresolved liabilities that may transfer to you, especially in a stock purchase.

For workers’ compensation specifically, request the business’s EMR history. An EMR significantly above 1.0 will directly increase your workers’ comp premiums after closing and may reflect safety culture issues that need to be addressed during the transition. Factor the EMR impact into your financial projections for the acquisition.

Assess contractual insurance obligations.

Review the seller’s contracts, leases and loan agreements for insurance requirements that will carry over to you as the new owner. Commercial leases almost always specify insurance requirements — coverage types, minimum limits and additional insured designations — that the tenant must maintain. Client contracts may require specific professional liability or general liability limits. Loan and equipment lease agreements may condition the financing on maintaining specific property or liability coverage.

These obligations become your obligations at closing. Identify them during due diligence so you can ensure your post-acquisition insurance program meets every requirement from day one.

Evaluate environmental and product liability exposure.

Two categories of historical liability deserve special attention because they can surface years or even decades after the originating event.

Environmental liability can arise from past manufacturing activities, chemical handling, fuel storage, waste disposal practices or operations on contaminated land. Cleanup costs for environmental contamination can be enormous, and liability can attach to current property owners regardless of whether they caused the contamination. If the business you’re acquiring has any history of activities that could produce environmental contamination, a Phase I Environmental Site Assessment is a standard due diligence step, and environmental liability insurance should be part of the conversation with your insurance advisor.

Product liability exposure persists as long as products sold by the business remain in use. A product manufactured or sold years before the acquisition can generate a liability claim years after you take ownership. In a stock purchase, this historical product liability is automatically transferred to you. Even in an asset purchase, successor liability doctrines may apply. If the business you’re acquiring manufactures or has manufactured products with injury potential, assess this exposure carefully and discuss product liability tail coverage with your insurance advisor. See more about tail coverage below.

Identify exposures not currently insured.

The seller may have operated without coverage for risks that you would normally insure. For example, no hired and non-owned auto coverage despite employees driving personal vehicles for work. No umbrella insurance policy despite significant liability exposure.

These uninsured exposures become your exposures the moment you take ownership. Document them during due diligence and include them in your post-acquisition insurance plan. In some cases, significant uninsured exposures may also be relevant to deal negotiations — the cost of addressing them should be factored into the acquisition price or handled through purchase agreement provisions.

Representations and warranties insurance

In larger or more complex acquisitions, representations and warranties (R&W) insurance is an increasingly common tool that protects the buyer against financial losses arising from breaches of the seller’s representations and warranties in the purchase agreement.

In a typical purchase agreement, the seller makes representations about the condition of the business — that financial statements are accurate, there are no undisclosed liabilities, the business is in compliance with applicable laws, there are no pending or threatened lawsuits, and so on. If any of these representations prove false after closing and the buyer suffers financial losses as a result, R&W insurance pays the buyer for those losses.

R&W insurance is most common in middle-market transactions and may not be cost-effective for very small acquisitions. However, it’s worth discussing with your attorney and insurance advisor, particularly in situations where the seller is unwilling to provide a significant indemnification holdback or escrow, where the seller is an individual who may not have the personal assets to back an indemnification claim or where the complexity of the business makes it difficult to fully verify all representations during due diligence.

Insurance at closing

Here’s what you need to know about business insurance when you reach the closing stage of your acquisition.

Binding new coverage

Your insurance coverage must be bound and effective at or before the moment the transaction closes. There should be zero gap between when you take ownership of the business and when your coverage begins. Operating an acquired business without insurance — even for a single day — exposes you to the full range of liabilities the business generates through its daily operations.

For asset purchases, you’ll typically need new policies in your name or endorsements added to your existing policies covering all acquired assets, operations and employees from the closing date forward. For stock purchases, the entity’s existing policies may continue with insurer consent, or you may need to replace them with new policies under the new ownership structure. Coordinate closely with both the seller’s insurance broker and your own agent to ensure continuity and prevent gaps.

Have certificates of insurance ready to issue at closing to landlords, clients, lenders and any other parties that require proof of coverage. These parties may need updated certificates reflecting the new ownership, and delays in providing them can create problems with lease compliance, contract performance and loan covenants.

Workers’ compensation continuity

If the acquired business has employees, workers’ compensation coverage must be in place at closing with absolutely no gap. In an asset purchase where you’re rehiring the seller’s employees as your own, you need a new workers’ comp policy or an endorsement adding the new operation and its payroll to your existing policy, effective at closing. In a stock purchase, the entity’s existing workers’ comp policy may continue, but the carrier must be notified of the change in ownership.

As discussed earlier, the seller’s EMR may transfer to you depending on the deal structure and your state’s rules. If the seller’s EMR is elevated, the impact on your workers’ comp premium can be significant and should be factored into your acquisition cost projections. Discuss the EMR implications with your insurance agent well before closing so you can budget accurately and, if appropriate, develop a plan to improve the EMR through safety investments after the acquisition.

FYI

If buying another business or opening a new location means your staff will expand, make sure you're up to date on all your insurance needs when hiring employees — beyond workers' comp and EPLI obligations.

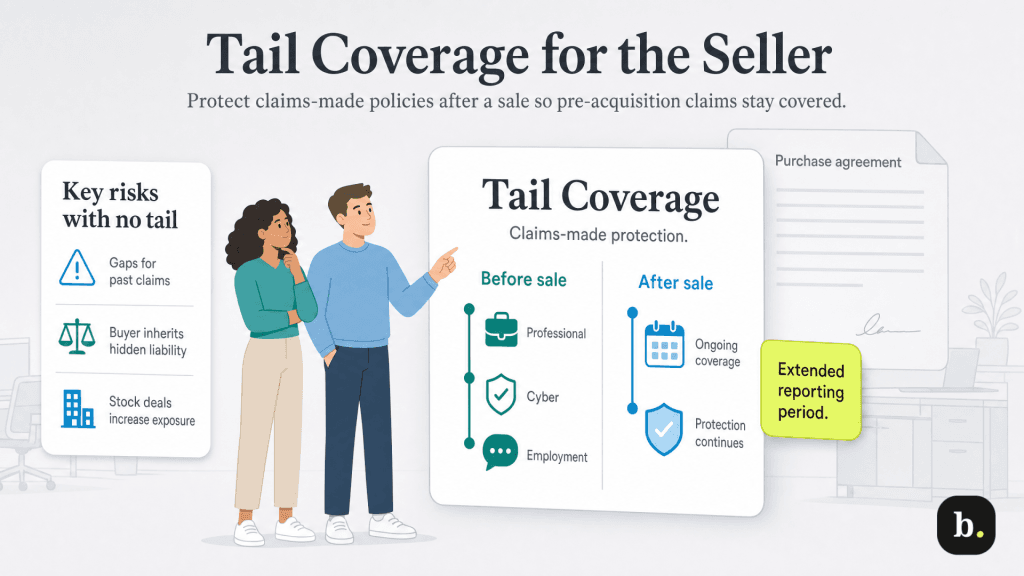

Tail coverage for the seller

Tail coverage, also called an extended reporting period, is one of the most important and most frequently overlooked insurance elements in a business acquisition. It applies specifically to claims-made insurance policies — policies that cover claims filed during the policy period, regardless of when the underlying event occurred.

Professional liability, cyber liability, employment practices liability, and directors and officers (D&O) liability are commonly written on a claims-made basis. When a claims-made policy ends — whether because it’s canceled, not renewed, or replaced — it stops covering new claims immediately, even if those claims relate to events that occurred while the policy was in force. Without tail coverage, a claim filed after a sale but based on pre-acquisition conduct falls into a gap: the seller’s expired policy won’t respond because it’s no longer in force, and your new policy won’t cover events that predate its inception.

This differs from occurrence-based policies (such as most general liability and commercial property policies), which cover events that occur during the policy period regardless of when the claim is filed. If a general liability policy was in force when a customer was injured, the policy responds to the claim even if the claim is filed years later.

Tail coverage extends the reporting window on a claims-made policy, allowing claims to be filed after the policy has ended as long as the underlying event occurred during the original policy period. Whether the seller or the buyer is responsible for purchasing tail coverage is a negotiation point in the purchase agreement. As the buyer, your priority is ensuring that tail coverage is addressed one way or another, because uninsured historical claims under claims-made policies can become your problem — particularly in a stock purchase where historical liabilities transfer with the entity.

Post-acquisition insurance integration

To ensure your insurance program runs smoothly after buying another business, follow these post-acquisition best practices.

Consolidate your insurance program.

After closing the deal, evaluate whether to maintain separate insurance programs for the acquired business and your existing operations or to consolidate them under a single program. Consolidation typically offers several advantages: cost savings through multi-location or multi-policy discounts, simplified administration with fewer policies to track and renew, and consistent coverage terms across your entire operation.

However, consolidation may not happen immediately. Some policies can’t be combined mid-term, and underwriting the combined operation may require new applications, updated loss runs and fresh risk assessments. Work with your insurance agent or broker to develop a realistic consolidation timeline, often targeting the next common renewal date as the point to bring everything under one program.

Reassess coverage limits.

The combined operation — your existing business plus the acquisition — is larger, more complex and has a different risk profile than either business had individually. Don’t assume that the sum of the two businesses’ individual coverage limits is adequate for the combined entity.

Reevaluate your general liability limits based on the combined revenue and employee count. Recalculate your commercial property coverage based on the total replacement value of all insured property across all locations. Update your business interruption limits to reflect the combined operation’s monthly fixed expenses. Review your umbrella or excess liability limits against the larger liability exposure of the combined business. The combined entity may warrant higher limits than either business carried independently, particularly for umbrella coverage, where the cost of additional limits is relatively modest.

Integrate employees and update workers’ compensation.

Ensure all acquired employees are properly classified and that their payroll is accurately reported under your workers’ compensation policy. If the acquired business operates in a different state than your existing business, you may need to add that state to your workers’ comp policy or obtain a separate policy for that state, since workers’ comp is state-regulated and policies must cover employees in the states where they work.

Review the acquired employees’ job functions against your existing classification codes. Don’t assume the seller’s classifications were accurate — misclassification is common and can result in premium audit adjustments. Update your EPLI, general liability and any other headcount-dependent coverages to reflect the combined employee count.

Review and update contractual obligations.

Notify all parties with insurance requirements — landlords, clients, lenders and partners — of the ownership change and provide updated certificates of insurance reflecting your post-acquisition coverage. Review every inherited contract for insurance provisions you need to meet and confirm that your current coverage satisfies all requirements.

Some contracts may contain change-of-ownership clauses that require the other party’s consent or impose additional insurance requirements upon a change of control. Identify these clauses during due diligence and address them during the closing process to avoid post-closing compliance issues.

Common insurance mistakes in acquisitions

Business acquisitions involve many moving parts, and insurance mistakes are common when the area doesn’t receive adequate attention during planning and execution. The following mistakes are all preventable.

Treating insurance as a post-closing task: Insurance due diligence should run in parallel with financial and legal due diligence, not after the deal has closed. By the time you discover a coverage gap or an inherited liability after closing, you’re already exposed, and your options are limited.

Failing to bind coverage effective at closing: Even a single day without coverage exposes you to the full range of liabilities the acquired business generates through its operations. Coverage must be in force the moment ownership transfers.

Not reviewing the seller’s claims history: The seller’s loss runs reveal critical information about operational risk, safety culture and the insurance costs you’ll inherit. Skipping this step means making a major financial commitment without understanding a significant component of your ongoing cost structure.

Overlooking tail coverage for claims-made policies: This is one of the most expensive mistakes in acquisition insurance. Without tail coverage, historical claims under professional liability, cyber liability, EPLI and D&O policies can fall into an uninsured gap that becomes your financial responsibility.

Assuming the seller’s policies automatically transfer or continue: Many policies contain change-of-ownership provisions that can void coverage, trigger cancellation, or require insurer notification and consent. Never assume coverage continues without verifying the policy terms and notifying the carrier.

Failing to reassess limits for the combined operation: After closing, your combined business is bigger and more complex. Operating with limits that were sized for your pre-acquisition business leaves the combined entity underinsured.

Not involving an insurance advisor early enough: An experienced commercial insurance broker can identify risks, evaluate the seller’s coverage, flag gaps and structure your post-acquisition program far more effectively when they’re involved from the letter of intent stage rather than brought in at the last minute.

Buying another business without insurance headaches

Insurance is a critical component of any business acquisition, and it deserves the same level of professional attention and rigor as the financial, legal and operational aspects of the deal. The acquisition structure — asset purchase versus stock purchase — fundamentally shapes your insurance exposure, and understanding the implications of each structure is essential to evaluating the true cost and risk of the deal.

Start insurance due diligence early. Review the seller’s policies, claims history, contractual obligations and uninsured exposures before you commit to the purchase. Ensure coverage is in place at closing with no gap. Address tail coverage for claims-made policies to prevent historical liabilities from falling into an uninsured void. And plan deliberately for post-acquisition integration — consolidating your insurance program, reassessing your limits, and updating all contractual and regulatory obligations to reflect the combined entity.

Work with a commercial insurance agent or broker experienced in acquisitions from the earliest stages of the deal through post-closing integration. The cost of professional insurance guidance during an acquisition is negligible compared to the cost of an inherited liability, a coverage gap or a compliance failure that could have been prevented with proper planning.

Adam Uzialko, the accomplished senior editor at Business News Daily, brings a wealth of experience that extends beyond traditional writing and editing roles. With a robust background as co-founder and managing editor of a digital marketing venture, his insights are steeped in the practicalities of small business management.

At business.com, Adam contributes to our digital marketing coverage, providing guidance on everything from measuring campaign ROI to conducting a marketing analysis to using retargeting to boost conversions.

Since 2015, Adam has also meticulously evaluated a myriad of small business solutions, including document management services and email and text message marketing software. His approach is hands-on; he not only tests the products firsthand but also engages in user interviews and direct dialogues with the companies behind them. Adam's expertise spans content strategy, editorial direction and adept team management, ensuring that his work resonates with entrepreneurs navigating the dynamic landscape of online commerce.