Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

What Is an Insurance Rider?

Adding a rider to business insurance helps you reduce costs and better protect against losses.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

An insurance rider adds or modifies an insurance company’s original coverage details. You can add riders to many policies, including business and life insurance to further mitigate risk and loss exposure.

Here’s everything you need to know about business insurance riders, including key benefits, choosing the right option for your company and making a claim on your rider.

What is an insurance rider?

Most insurance policies come with standard coverage detailed in the contract, but there may be times when you want to add or change coverage. An insurance rider can accomplish this. You’ll usually pay extra to add a rider when you need to fill a gap in the stand-alone policy and customize your business insurance.

An easy way to remember what a rider does is in its name: additional coverage “rides along” with the existing policy.

Did You Know?

Another name for a rider is an endorsement. However, to add confusion, insurance companies will use the term rider and endorsement interchangeably. For example, you can purchase a rider to modify a life insurance policy while from the same company buying an endorsement to add coverage to your homeowner’s insurance.

Riders can be added to many business insurance policies, including the following:

How the rider affects the policy’s coverage depends on what’s missing in the stand-alone policy and what the rider says it will cover. The carrier will standardize each policy as the monoline policy, which is insurance coverage focused on a single type of risk. Then, business owners can add a rider to modify these policies and better protect themselves from losses.

Tip

If you have commercial auto insurance, consider getting gap insurance, an optional policy that pays the difference between the depreciated value of the car and what you owe. Keep in mind, gap insurance is usually only available through the lending institution and not through an insurance company.

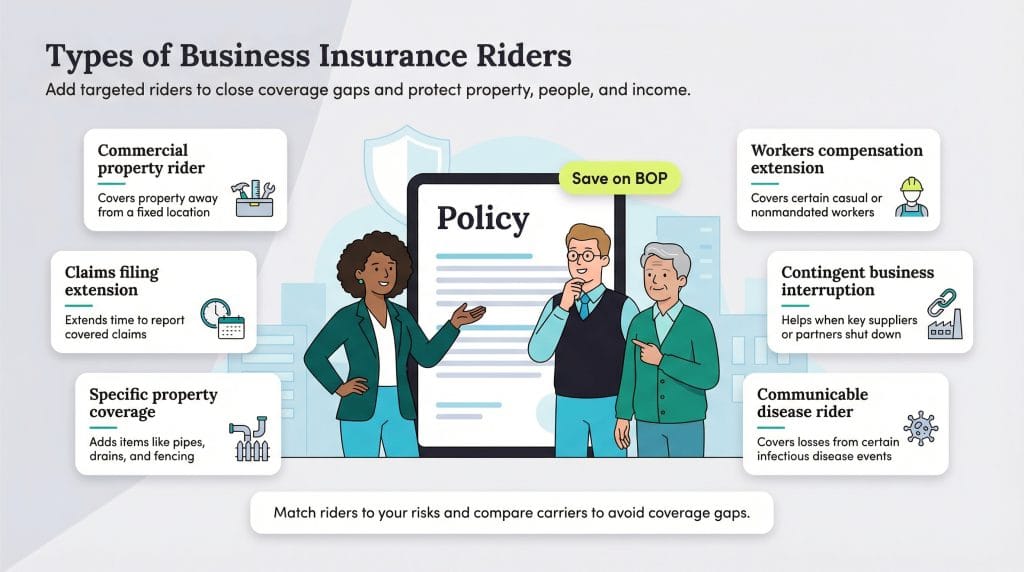

Types of business insurance riders

Ask your insurance carrier about the riders available for policies you’re purchasing. Not every carrier offers the same selection of riders, which may lead you to choose another insurance company.

Some examples of typical business insurance riders include the following:

Commercial property rider: A commercial property rider is a type of inland marine coverage that protects business property that isn’t stored at a fixed location.

Specific property coverage: This rider extends commercial property insurance coverage to include things like underground pipes, drains or fencing that may otherwise be excluded.

Workers’ compensation extension: This rider extends workers’ compensation benefits to casual employees you’re not mandated to cover.

Contingent business interruption: This rider kicks in when a primary supplier, partner or customer shuts down, preventing your standard business operations from proceeding.

Communicable disease rider: Many policies have exclusions for communicable diseases. This rider covers losses that occur due to infectious diseases. For example, this rider would have covered business shutdowns due to the COVID-19 pandemic.

Neokissha Penix, an underwriting auditor who focuses on commercial insurance has noticed the most common commercial business insurance riders are commercial property riders. They are purchased to help fill gaps in coverage to protect the insured’s property.

Penix said the most common riders she funds into are for “covering property not at a fixed location. Having worked with a lot of contractors they constantly have tools/equipment at different job sites. This [rider] helps if the tools are damaged or stolen while not at the primary property location.”

Did You Know?

A business owner's policy (BOP) is a combination of general liability insurance and business property insurance. Many BOPs come with riders for both liability and property and offer a great way to save money by having a lower premium than paying for both plans separately.

What are the benefits of riders?

Insurance riders offer many benefits to businesses, including the following.

Insurance riders provide customized coverage.

A primary business insurance contract provides standard coverage and is generally static. The insurance carrier won’t go line by line to individualize the terms. However, your business may need more or different coverage than the standard provisions.

This is where riders come in. Riders let customers make changes to provide more comprehensive coverage — whether they need specific benefits not otherwise available or their needs have changed since their original contract was instated.

Although you must pay extra for an insurance rider, the additional cost is worth it to make sure your business is properly covered. A little extra for the right insurance is better than finding out after a loss that you were underinsured or not covered at all.

Additionally, riders usually have lower deductibles than standard insurance policies. Thus, adding a rider could increase your overall insurance payout.

Insurance riders bring peace of mind.

Running a business can be unpredictable, even in the best of times. Modifying your insurance coverage to mitigate risk and meet your business’s present (and future) needs can bring much-needed peace of mind.

Even if you don’t purchase an insurance rider now, knowing your options can empower you to plan ahead if you need additional coverage down the line.

Buying an insurance rider is as straightforward as letting your insurance carrier know you want to add specific coverage. Riders usually cost pennies on the dollar compared to a whole new policy, making them an affordable and efficient way to add coverage.

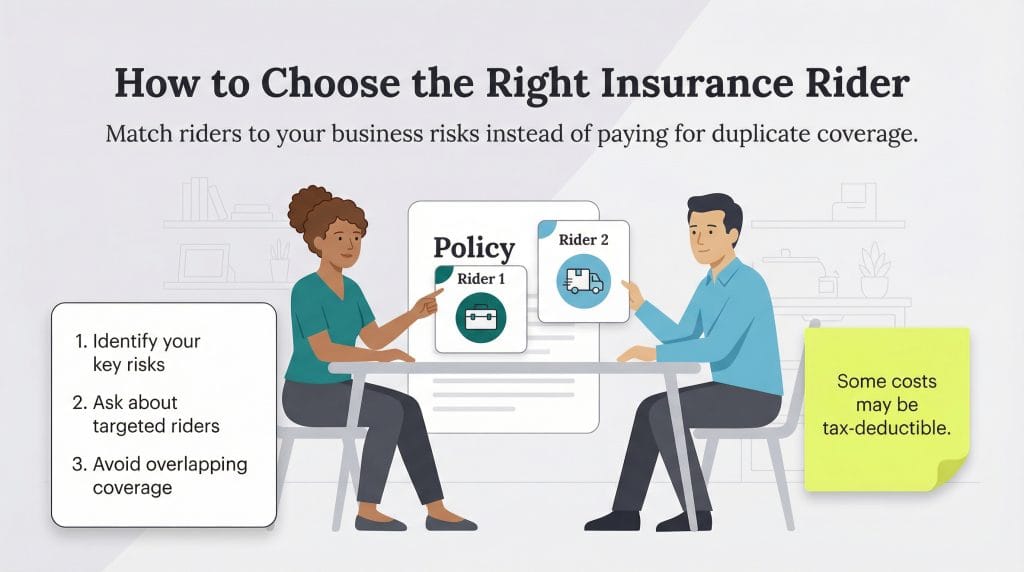

However, choosing a rider takes some consideration. When choosing business insurance, many business owners don’t think to ask about additional coverage, assuming the policy they’re purchasing covers everything they’ll need. This isn’t the case. Be sure to ask your carrier about its options to see if any riders fit your needs.

Depending on your business activities, some riders make more sense than others. Here are some examples:

Who needs commercial property riders? A contractor constantly moving tools from job site to job site must have coverage for commercial property not at a fixed location. They must be covered wherever their work takes them and while commuting. A commercial property rider will cover these situations.

Who needs contingent business interruption riders? A business that relies heavily on a specific supplier for necessary production materials would be shut down if there were a supply chain problem. This is where contingent business interruption riders come into play.

Often, a specific rider will make sense for you and your business, while others won’t seem as essential. Business owners should talk to their insurance agent about their company’s needs and ask if specific riders would better protect their interests.

While a rider is an important component in having proper coverage, both insurers and insureds need to make sure the rider is right for their business. This can only come about through honest conversations about business needs, risks and the goal of adding a rider to the policy.

“Custom endorsements allow … for a more accurate pricing model. But if not done carefully in conjunction with the standard policy it could provide an opportunity for businesses to overpay for overlapping coverage if the same coverage is afforded on the standard policy,” said Sheila Flores, a commercial adjuster with years in the industry. “Being specific on endorsement language will allow the flexibility to cover specific risks.”

Of course, wrapped up with choosing the right rider is finding the best business insurance provider. We’ve saved you the trouble and researched insurance companies to find the best business insurance providers for you.

One of the great things about a rider is there is no added work if you file a claim. As long as you pay your premium, the claims process is seamless and includes losses related to the rider.

Here’s how making a claim on a rider works:

Gather all the loss details and call the insurance carrier and file a claim.

A claims adjuster will conduct an initial investigation for the purposes of confirming your coverage, including the rider.

The adjuster will then work to determine the loss value and finalize the claim.

The business owner will receive payment.

Insurance rider FAQ

Riders are not just for business insurance. Standard riders are found in homeowners, personal auto and life insurance. For example, a typical homeowners insurance rider covers sewer and drain backups. A common personal auto insurance rider covers accidental death. Life insurance has many riders, including a waiver that pays your premium if you become disabled.

In most cases, riders aren't free though there are instances where an insurance carrier will add a rider for free to expand coverage or meet state minimum insurance requirements. The cost of a rider varies widely, but it's often just a few extra dollars per month. Riders are usually affordable because little to no underwriting is involved in the purchase.

A rider and an endorsement are the same. They both add coverage to a policy for specific need categories. A floater is similar in that it's added to a policy to increase coverage. The key difference is that a floater adds coverage for specific items. Floaters are most commonly found with homeowners insurance policies and often add coverage for items like jewelry or fine art.

Riders are worth their cost because they address specific use cases to limit your financial responsibility in common claims. Without a rider, a business owner may miss out on much-needed coverage.

Some companies may add a life insurance policy for key personnel whose loss may disrupt business operations. Should that individual leave the company, the policy owner can conduct a transfer of insured rider, which swaps one insured individual for another. Consider your business's individualized circumstances to determine whether a life insurance policy will benefit your business; you can also consult with your insurance provider or a financial professional for further insight.

Kimberlee Leonard is an insurance expert who guides business owners through the complicated world of business insurance. A former State Farm agency owner herself, Leonard started her decades-long career as a financial consultant advising on investment strategies before switching her focus to insurance and risk mitigation for businesses.

At business.com, Leonard covers topics related to business insurance, such as workers' compensation rates, professional negligence, insurance riders, hold harmless agreements and more.

Leonard has developed insurance primers on everything from small business insurance costs to specific policies, such as excess liability insurance. She has also reviewed business software tools, analyzed employee retirement plan providers and continues to share insights on financial topics as they relate to business. Leonard's work has been published in Forbes, U.S. News and World Report, Fortune, Newsweek and other respected outlets.