Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

How Business Debt Consolidation Works

If you have multiple business debts, consolidation may simplify your payments. Here's what you need to know before deciding if this option is right for your business.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

Consolidating business debt combines all your loans into one, potentially lowering your interest rate and decreasing your risk of accidentally missing a payment. However, debt consolidation isn’t for everyone. Before combining your loans, learn how to consolidate business debt and understand the benefits and risks of debt consolidation for business.

Searching for funding and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

How does business debt consolidation work?

With business debt consolidation, you’ll take out a single new loan to pay off multiple existing debts, including business credit cards and other small business loans. Instead of juggling numerous payments, you end up with just one monthly bill, which simplifies your finances and makes repayment much easier to manage. Depending on your loan repayment terms, you might also save money on interest by eliminating high-interest loans and credit card balances.

“Debt consolidation can simplify your situation if you have lots of individual payments, reducing it all to just one payment,” explained financial expert Eric Rosenberg. “If you get a lower interest rate, it can save you money and even help you pay off the debt faster.”

There are other ways to consolidate debt as well. For example, a debt management plan involves working with a third-party organization that handles your payments. You don’t receive a new loan — instead, the third party collects one monthly payment from you and distributes it to your creditors. You’ll typically pay a fee for this service.

However, while other options exist, we’ll focus on how to use a business debt consolidation loan to simplify repayment and reduce interest costs.

Who should consider business debt consolidation?

Business owners who feel overwhelmed by making payments to multiple creditors every month may want to consider business debt consolidation. It offers the simplicity of a single monthly payment, making it easier to create a realistic business budget. It also reduces the chance of missing a payment, which is important because missed payments can hurt your credit score.

Rosenberg also suggests considering business debt consolidation if your situation has improved recently.

“If your credit is higher now than when you first got your loans, getting a consolidation loan at a lower rate can save you a lot of money,” Rosenberg noted. “Those savings can be put back into your business.”

Tip

When applying for a business loan for consolidation purposes, carefully consider the amount you'll need to successfully cover existing debts. If you're approved for a $10,000 consolidation loan but have $25,000 in debt, consolidating won't be effective.

Does consolidating business debt hurt your credit?

While consolidating your debt can lower your monthly loan payments, you may see a temporary dip in your credit score. When you apply for a debt consolidation loan, the lender will conduct a hard inquiry on your credit, which can lower your credit score by a few points.

However, if you make timely payments on your consolidation loan, your score should rebound quickly. Ultimately, if you need to lower your annual percentage rate (APR) and monthly bills, a short-term dip in your score may be worth it for the long-term financial benefits.

Consolidating your debt into one loan may also help you get approved for future loans. When lenders look at your credit history, they don’t like to see a long list of outstanding balances. If you think you might need an additional loan soon to support growth or sustainability, business debt consolidation can help streamline your credit report.

FYI

Missing payments or defaulting on your loan can seriously impact your credit. Prioritize timely payments to maximize the benefits of your debt consolidation loan.

What is the difference between debt consolidation and a loan?

Since debt consolidation is one way to use a business loan, the two are often closely linked.

A debt consolidation loan is a type of business loan used to pay off other high-interest debts. By using it to eliminate existing business debt, including credit card balances, you simplify your finances and replace multiple payments with a single fixed monthly bill.

Still, there are small differences between business debt consolidation and a typical business loan. Here’s a quick breakdown:

Business debt consolidation

Business loan

A loan used to pay off other high-interest debts, such as loans and credit cards

A loan used for general business funding needs (hiring, expanding, etc.)

Combines multiple payments into one fixed monthly payment

Adds a separate payment for each new loan

May offer a lower overall interest rate

Interest adds up with each additional loan

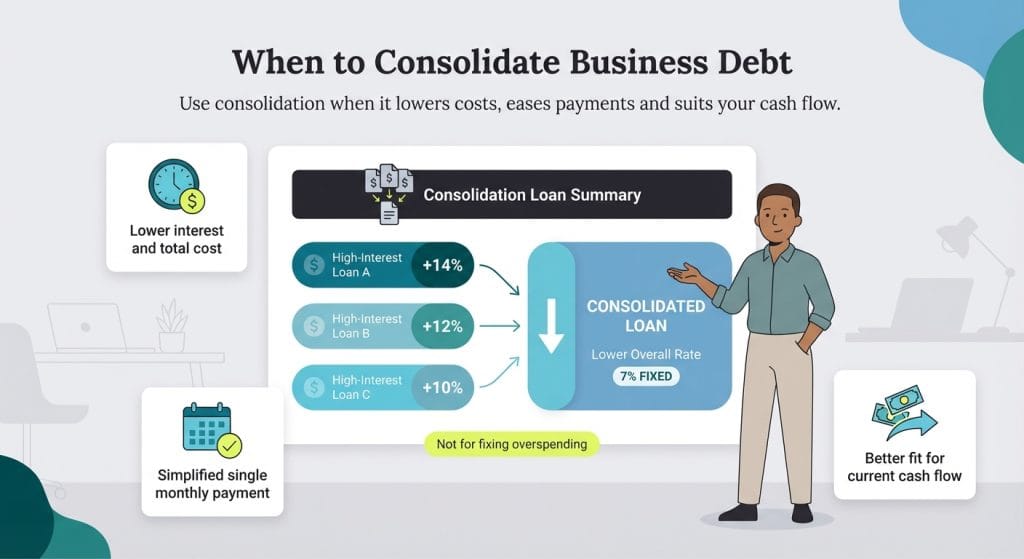

When should you consolidate business debt?

Consolidating your business debt is a strategic decision that can reduce interest costs and stress. However, it only makes sense under specific circumstances, including the following:

You have multiple high-interest debts: If your business is juggling several loans or business credit cards with high interest rates, consolidating your debt into a single loan with a lower interest rate can lead to significant savings over time.

Debt management is overwhelming: Managing multiple loan payments can be time-consuming and stressful. Consolidating into a single monthly payment can simplify your financial operations.

You have cash flow problems: Combining debts into one loan may improve your cash flow and free up funds for other business needs.

You want a lower interest rate: Say your debts have high APRs, like those on business credit cards, which can be 20 percent or more. If you qualify for a business loan with a low APR — such as one from a traditional bank — you could save significantly by consolidating.

You need shorter loan repayment terms: You may also benefit from business debt consolidation if you want to shorten your loan repayment term. The shorter the period during which you repay your loans, the less interest you pay. And the less interest you pay, the better your cash flow will be.

Here are some good and bad reasons to move forward with business debt consolidation:

Reason to consolidate

Good use

Bad use

Lower your interest rate

Yes

No

Shorten your loan repayment term

Yes

No

Spend more money

No

Yes

Before moving forward, take an honest look at your finances. Figure out what monthly debt payment fits comfortably within your current cash flow. Review your ongoing expenses to see where you can afford to reduce business costs.

Bottom Line

Business debt consolidation can be part of a successful financial plan, but it can't fix poor spending habits. Use it to strengthen your plan, not to avoid making one.

How many times can you consolidate business debt?

Technically, there’s no limit to how many times you can consolidate business debt. However, repeated consolidation isn’t a long-term solution if overspending is the root cause of your financial trouble.

The act of consolidating is simple. The hard part is recognizing and addressing the habits that caused the debt in the first place. Using consolidation as a quick fix to keep spending beyond your means won’t solve anything. If you don’t reflect on how you accumulated the debt, you risk falling back into the same patterns and digging yourself into a deeper financial hole.

The good news is that getting back on track is possible. With effective budget planning, tracking your spending and mentally preparing for any spending hiccups, you can foster sustainable financial habits.

Tip

Once you pay off your debt, consider depositing the money you were using for loan payments into a business savings account. That way, you'll have funds set aside for unexpected expenses, and there won't be a need to take out another loan or worry about extra fees.

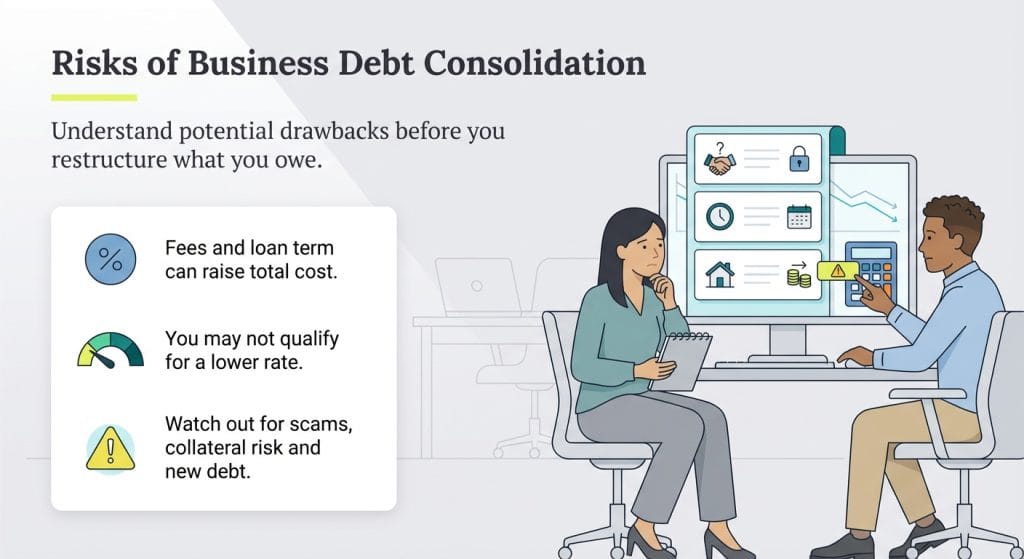

What are the risks of debt consolidation for business?

As with any loan, you must carefully consider the costs and risks of debt consolidation. Here are some crucial factors to consider.

New loan fees: When you apply for a business debt consolidation loan, the lender may charge fees for the application and approval process. These fees are often added to your original debt, increasing the monthly payment.

Extended loan term: Lowering your monthly payment tends to increase the number of months it will take to pay off the loan in full.

Interest rate qualifications: Finding a loan with a lower interest rate to consolidate your debt is possible only if you have good credit and minimal debt. Use a loan calculator to see if a slight reduction in your interest rate will make a difference in the total amount you pay over time. If you are already a few years in, or have bad credit or excessive debt, there’s a chance you won’t save any money by consolidating your business loans.

Prepayment penalty: If you plan to pay extra money each month on your loan’s principal to pay it off faster, check your loan agreement to verify that there’s no prepayment penalty. Lenders add this clause to ensure they make the maximum amount of money in interest on your loan.

Consolidation scams: Consumers and business owners are scammed by debt consolidation lenders every year. Stay away from these companies. Instead, research DIY solutions, such as balance-transfer credit cards with no annual fee and business loans. You can often find these through your financial institution or online vendors. Always go with a company you have researched and trust.

Collateral: Some banks require collateral, such as property or equipment, to approve a business debt consolidation loan. If you haven’t taken the time to analyze your spending and commit to a strict budget, you could easily fall back into excessive spending. Are you prepared to lose what you need to put up for collateral?

Credit score: If your credit score has already taken a hit from your debt, you may not qualify for a debt consolidation loan. Or, if you do, the interest rate might not be any better than what you’re paying now. A good credit score is crucial for securing the best business loans and financing options. Always aim to make your debt payments in full and on time.

More debt: Consolidating your debt may create the illusion of having more money, especially if you’re doing so to pay off business credit cards and thus have more credit available. Refrain from charging purchases on these cards to avoid the burden of repaying even more debt.

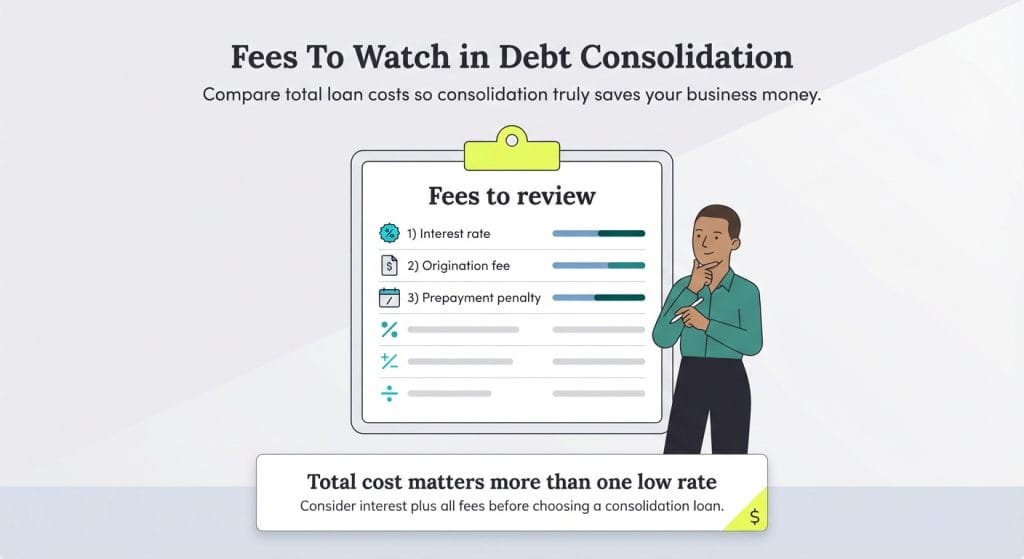

Which fees are associated with debt consolidation?

Debt consolidation can take many forms, including traditional business loans from banks, SBA loans, alternative lending and business credit cards. Some business owners even take out personal loans. No matter which option you choose, small business loan fees are common.

“Look at the costs to make sure that, in the long run, the loan will save you money,” Rosenberg advised. “Run the numbers to make sure that between interest, origination fees and other costs, you really will come out ahead.”

Be sure to consider all potential fees when deciding whether consolidation will help your business pay off its debts. Fee types and amounts vary by lender. Here are some fees to look for before accepting a loan:

Application fee

Origination fee

Guarantee fee

Appraisal fee (for collateral)

Annual fee

Late fee

Prepayment penalty

Closing costs

What qualifications do you need for business debt consolidation?

Lenders evaluate whether small business owners should be approved for business debt consolidation based on the following factors.

Credit history and score: Like all business loans, debt consolidation requires a good credit history and credit score. That said, it’s not the end of the road if your credit score or borrowing history is poor.

Collateral: In some cases, putting up collateral can persuade a hesitant lender to approve your debt consolidation loan. Just be sure you can repay your debts so your property isn’t seized.

Financial stability: If your financial statements show up-and-down revenue in recent times, lenders will not know whether you’ll earn enough to repay your loans, so approval is less likely.

Business income: For obvious reasons, high business income is a much more straightforward route to loan approval than low income. Before consolidating your loans, consider boosting your revenue.

What are some business debt consolidation options?

Here’s a quick summary of typical debt consolidation options:

Loan type

Description

Upsides

Top picks

Term loan

A fixed-amount loan repaid over several months to years

If you're deciding between a term loan vs. a line of credit for debt consolidation, a term loan is better for paying off a fixed amount of debt, while a line of credit is ideal for ongoing expenses, not lump-sum consolidation.

Is business debt consolidation right for your business?

Although business debt consolidation can be helpful, it isn’t a substitute for smarter spending decisions. You should only borrow money you’re confident you can repay, which means investing in loans that fit your financial reality. As such, debt consolidation isn’t a strategy — it’s a last resort.

If you’re juggling debt from multiple creditors, it can feel overwhelming. In some cases, consolidating that debt can simplify your payments and lower your interest rate. Just be sure to research your options carefully to determine whether a business debt consolidation loan is truly the right solution for your situation.

Miranda Marquit and Mike Berner contributed to this article.

With nearly two decades of experience under her belt, Julie Thompson is a seasoned B2B professional dedicated to enhancing business performance through strategic sales, marketing and operational initiatives. Her extensive portfolio boasts achievements in crafting brand standards, devising innovative marketing strategies, driving successful email campaigns and orchestrating impactful media outreach.

At business.com, Thompson covers branding, marketing, e-commerce and more.

Thompson's expertise extends to Salesforce administration, database management and lead generation, reflecting her versatile skill set and hands-on approach to business enhancement. Through easily digestible guides, she demystifies complex topics such as SaaS technology, finance trends, HR practices and effective marketing and branding strategies. Moreover, Thompson's commitment to fostering global entrepreneurship is evident through her contributions to Kiva, an organization dedicated to supporting small businesses in underserved communities worldwide.