Running a business is inherently risky. Business owners must protect themselves and their companies as much as possible against all potential threats. Purchasing business insurance is one way to mitigate risk and reduce losses caused by unforeseen events.

As a business owner, you’re likely familiar with how to file an insurance claim. However, many owners aren’t aware of how insurance companies view risk and how risk factors affect coverage and costs. We’ll examine the concept of risk in business insurance, explain how insurers assess risk and share ways to reduce your risk exposure.

Editor’s note: Looking for the right liability insurance for your business? Fill out the below questionnaire to have our vendor partners contact you about your needs.

What is an insurance risk?

Insurance risk is an assessment of the actuarial likelihood that an adverse event will occur and result in a loss. “Risk to the insurance industry is the potential for financial loss from an accidental situation occurring which would be contractually financed through an insurance contract,” said Harry Bound, vice president of the Arnold Insurance Agency.

Actuarial models use mathematical and statistical techniques to analyze historical insurance claim data to model how likely an adverse event is to occur for a specific business and what the cost might be. If the adverse event comes to pass, you’ll file a claim with your insurer. The insurer will pay out on the claim if it’s a qualifying event.

Business insurance costs are based on an insurer's assessment of how likely your business will become victim to the qualifying events you want protection against.

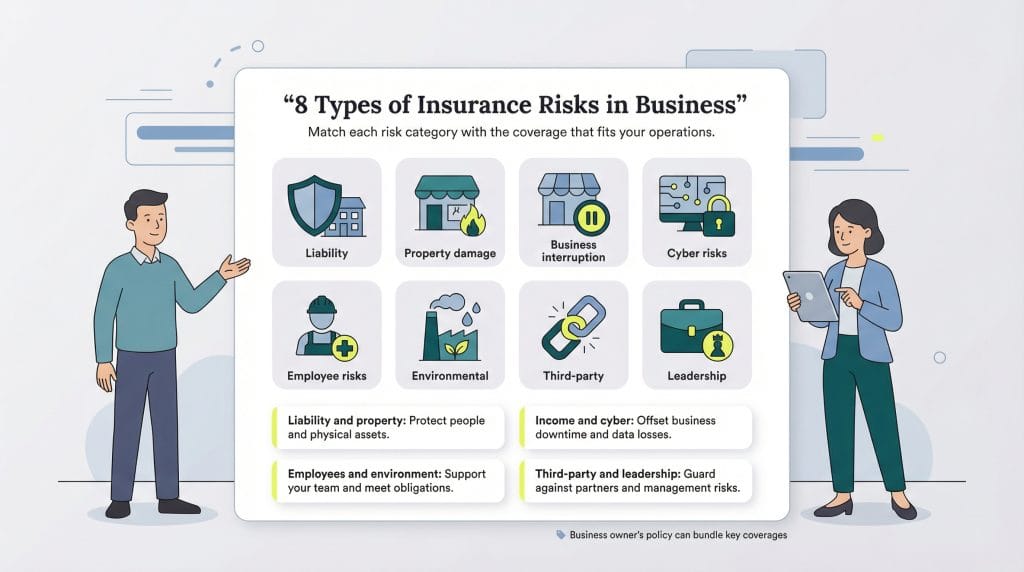

What are the types of insurance risks in business?

Here’s an overview of eight common insurance risk categories in business and the policies that can help cover them.

1. Liability risks

Liability insurance covers your business’s legal responsibility to prevent physical or financial harm or damage to others. Several types of policies are tailored to specific liability risks. Here are some examples:

- General liability insurance: The most common types of risks are covered by general liability insurance, which is often called slip and fall coverage because it can help cover incidents like a customer slipping and falling in your retail outlet. This insurance could help cover medical expenses and legal costs if the injured person decides to file a lawsuit.

- Product liability insurance: Product liability insurance is advisable if you manufacture products you sell to others. For example, say you manufacture and sell a skin cream that triggers a severe allergic reaction in a customer. Product liability insurance would cover this claim’s legal fees and compensation costs.

- Errors and omissions (E&O) insurance: E&O insurance covers businesses against mistakes or oversights they make when providing their services that result in financial loss or harm. For example, say an accountant makes a significant error on a client’s tax return that leads to IRS and state fines and penalties. E&O insurance would cover the costs if the client sued or demanded compensation.

- Professional indemnity insurance: Professional indemnity insurance is broader than E&O insurance and includes instances of negligence, breaches of professional duty and, in certain cases, breaches of copyright and defamation. For example, say a firm hired an architect to design a new warehouse. However, after erecting the building, they discovered its floor’s load-bearing capacity wasn’t sufficient for the warehouse’s stock. This flaw reduces the building’s utility drastically. If the architect knew the requirements but didn’t account for them, the client may have a strong case to bring against the architect’s professional indemnity insurance providers. They could then be compensated for the financial losses incurred by this oversight.

Builders' risk insurance is liability insurance for people and companies involved in a project where a new building is under construction. It can compensate stakeholders for losses related to delays, including additional loan interest and lost rental income.

2. Property damage risks

Commercial property insurance covers damage to your business’s physical assets, including real estate, inventory, supplies and materials, office furniture and electronics, signs and fixtures.

Common occurrences that commercial property insurance covers include a fire breaking out in your warehouse, causing damage to a significant proportion of your inventory or intruders stealing from and vandalizing your store.

3. Business interruption risks

Following an incident like a fire destroying a warehouse and its inventory, it may take a while for a company to recover enough to start doing business again.

In addition to commercial property insurance, business interruption insurance may be a sensible investment in these situations.

Depending on the coverage you negotiate with your insurer, you’ll receive funds to replace your lost revenue. You’ll also get help to continue paying fixed expenses like rent and salaries. This financial help may be the difference between closing permanently and reopening.

4. Cybersecurity and data risks

Several cyber risks can lead to devastating data breaches, including the following:

- Cyberattacks: Cyberattacks are a significant cause of business downtime.

- Ransomware: Ransomware, a form of cyber extortion, is a major cybersecurity risk. Unless you pay hackers to restore access, you’re locked out of your data, information technology system or both.

- Phishing: Business scams like phishing can harm an organization. With phishing, someone uses email or the phone to request information while pretending to be someone else, like a supplier or coworker.

Data breach costs can be overwhelming, making cyber insurance a must for many businesses. There are two primary types of cyber insurance for cyber risks ― cyber liability insurance and data breach insurance. If you hold and process sensitive data on computer systems and via paper records (like a medical practice, for example), you’ll need data breach insurance to cover the loss of non-digital records. That said, many cyber liability insurance policies will also cover this loss but check the small print before signing up.

5. Employee-related risks

Employee-related risks can take several forms. The following policies can help cover some of these risks:

- Injured employees: If an employee is injured while operating machinery, they might claim compensation for their injuries and lost wages. To cover your business against these situations, obtaining workers’ compensation insurance is crucial.

- Disgruntled employees: If there’s a risk that a disgruntled former employee could sue for wrongful termination, employment practices liability insurance (EPLI) can provide coverage for situations.

6. Environmental risks

Many businesses, particularly in manufacturing and extraction, are subject to more regulations because of the effects of their activities on the environment. For example, they may have a tank at a manufacturing plant leaking chemicals into a nearby river.

For companies in these sectors, environmental liability insurance can help cover the costs of failing to meet these obligations.

7. Third-party risks

Third-party risks vary by business and industry but can include the following:

- Supply chain disruptions: Your business is part of an interconnected web of companies that rely on each other to survive. Disruption in one company in the supply chain may affect your business even if you don’t deal with it directly. Alternatively, a natural disaster or political instability might delay products arriving to you. Supply chain insurance offers a degree of protection in these situations.

- Nonpayment: Other third-party risks include clients not paying your invoices for products and services you’ve already delivered. The risk is amplified further if you offer credit terms to clients and they go bankrupt after building a significant balance with you. Many firms take out trade credit insurance to protect against financial losses like these.

8. Leadership risks

Leadership risks can include the following:

- Mismanagement: A business’s leadership can dictate its success or failure. Leadership risks can occur when business owners or high-ranking stakeholders make poor decisions, mismanage finances or breach their fiduciary duties. In these cases, directors and officers insurance can provide some financial protection, depending on the circumstances.

- Loss of a leader: A key individual in a business may leave or become incapacitated. Many companies rely on the vision of a CEO to drive them forward or become heavily dependent on the revenues from a top salesperson. In these cases, key person insurance can provide financial compensation to help your business manage the impact and transition period.

The recommended policies listed above are examples of the coverage you might require. It’s critical to check with an insurance agent or insurance broker for policy details to address your specific business needs. [Learn more with business.com’s best picks for business insurance]

A

business owner's policy (BOP) is a great way to protect your business against multiple risks as it combines general liability, business income insurance and commercial property insurance into one policy.

How does insurance risk work?

A business owner buys an insurance policy to gain financial protection from specific risks or dangers. After purchasing the insurance policy, a risk transfer takes place. The insurance company assumes the risk in exchange for a regular payment, called a premium.

After the insurance company assumes the risk of financial loss, it places the business in a “risk pool,” a large group of businesses that share common risks of incurring losses. In other words, the insurance company spreads its financial risk over a large pool of premium-paying contributors.

How do insurance companies assess risk?

Actuarial models provide insurers with a statistics-based estimate of the following:

- How likely a qualifying event (like inventory theft) will occur at a particular business

- The potential losses from that qualifying event

Consider these actuarial models a “macro” assessment. After that, underwriters conduct a “micro” assessment to tailor the risk evaluation to a specific business.

To do this, underwriters gather information about their potential client to create an individualized assessment. For example, if the business has a burglar alarm and keypad entry to the inventory room, the risk is lessened. However, the shop may be in an area with higher crime rates, increasing the risk.

Underwriters will look at objective and subjective information:

- Objective information: A company’s claims history, measured via “loss runs,” provides underwriters with objective data on past claims to create a more focused risk profile. They’ll use your past behavior to assess how frequently you’ll likely make a claim and how much it will cost.

- Subjective information: Underwriters will also apply subjective judgment to estimate future claims by inquiring about what a business is doing to reduce risk. For example, it may be implementing measures to stop inventory from being stolen.

At the end of this process, the insurance company will offer you a premium that reflects its view of your individual risk profile.

Underwriting is not a one-size-fits-all approach. Each insurance company has its own determining factors when evaluating a risk pool.

How can I reduce risk?

The primary way to reduce risk is to institute a formal loss control program, which helps policyholders reduce claims using risk management and safety resources and training. Many insurance companies or agencies will help you develop a program to mitigate risk through risk control. Some examples of this, according to Bound, “are loss control inspections by a loss control expert, proper maintenance, personal manuals, buy/sell agreements, safety manuals, employee training and the like.”

Here are a few other ways to reduce risk.

1. Follow your insurer’s risk control guidance.

Some insurers offer risk management programs for their insurance policyholders. Other insurers also provide risk control representatives who can give suggestions and guidance.

For example, your risk control consultant can guide you through the contractual risk transfer as you enter into a contract with an outside entity, such as a subcontractor, tenant or service provider, which creates a new set of risks and liability issues.

2. Reduce your auto-related risks.

Insurance companies help policyholders mitigate risks associated with auto accidents. For example, a common risk is distracted driving.

In recent years, some of the best GPS fleet management services have introduced artificial intelligence-powered dash cams that can warn drivers when they’re distracted. They can tell whether a driver is eating, drinking, smoking, using a cell phone and more. They immediately alert the driver and send information to the company’s fleet manager.

Your business can also use risk management software with fleet tracking software to analyze data from previous accidents and claims to learn how the risk could have been mitigated.

3. Mitigate your cyber risks.

Conduct a cybersecurity risk assessment to determine your vulnerability to internal and external data breaches. Successful approaches include using a business virtual private network (VPN) instead of remote PC access software because a VPN allows for data encryption and protects sensitive or private information.

Healthcare companies that must comply with the Health Insurance Portability and Accountability Act face extra challenges. Any covered entity or business associate that collects, processes or stores protected health information is required to implement security and privacy controls to protect its confidentiality, integrity and availability (also known as the “CIA triad”).

Employees should also use only company-authorized devices for remote work and dispose of company documents properly.

Nathan Weller and Nicole Urbanowicz contributed to the reporting and writing in this article.