Business.com aims to help business owners make informed decisions to support and grow their companies. We research and recommend products and services suitable for various business types, investing thousands of hours each year in this process.

As a business, we need to generate revenue to sustain our content. We have financial relationships with some companies we cover, earning commissions when readers purchase from our partners or share information about their needs. These relationships do not dictate our advice and recommendations. Our editorial team independently evaluates and recommends products and services based on their research and expertise. Learn more about our process and partners here.

Types of Fast Business Loans

When your business needs a quick infusion of cash, what are your options? Learn about the different types of fast business loans and what you need to apply for them.

Business.com earns commissions from some listed providers. Editorial Guidelines.

Table of Contents

They say the only two things certain in life are death and taxes, but in business, there’s a third constant: the need for money. When you can’t immediately cover that need with your own cash or assets, fast business loans may help. These alternative lending options can get you the cash you need more quickly than many traditional lenders. Read on to learn whether a fast business loan is right for you, what you’ll need to get one, and what types of fast business loans are available.

Searching for a business loan and not sure where to start? Tell us a little more about your business and get customized quotes from qualified providers.

Types of fast business loans

Consider the following options if time is short and your financial need is immediate.

Business credit cards

Business credit cards can provide a convenient funding source for your company. They often come with low or no fees, and you can avoid interest charges if you repay your balance on time. Approval can take anywhere from just moments to as long as two weeks.

When you apply, you may need to provide details such as your company’s size, industry and tax classification. Most of the companies and banks that offer personal credit cards also offer business credit cards.

Tip

It's crucial to use business credit cards wisely; otherwise, you could end up in a worse financial situation than you were trying to fix.

Invoice financing

With invoice financing — sometimes called invoice factoring — you can turn unpaid customer invoices into quick working capital. If a client hasn’t paid and you need their cash now, a financing company can advance a portion of the invoice’s value. You may receive funds in as little as 24 hours after submitting financial documents. Depending on the arrangement, either you or the financing company will collect the customer’s payment, which is used to repay the advance along with fees and interest.

Short-term loans

Short-term loans are a broad category that includes any loan you can get within a few hours or days. These loans usually come with a quick repayment timeline — typically one to two years — and include interest and fees. Lender requirements vary, but many ask for proof of income, a credit check, and documentation showing how long you’ve been in business. You’ll usually find these loans through online alternative lenders.

Merchant cash advances

A merchant cash advance is provided by your credit card processing company. You’ll get a cash infusion from your payment processor, and in return, the processor will take a percentage of your future credit card sales until the advance is repaid. Alternatively, your card processor may regularly withdraw fixed amounts from your account. You can usually get cash within a day, but your loan fees may be exceptionally high.

Equipment financing

If you’ve ever paid for an expensive item in monthly installments instead of all at once, then you’re familiar with equipment financing. With this type of fast business loan, you can get equipment immediately and pay for it over time.

You can often be approved in as little as two days, and paperwork requirements are usually minimal. That’s because equipment financing is a low-risk option for the provider: The equipment itself serves as collateral. If you fall behind on your payments, your provider may take back the equipment, leaving you without the tools you need — and with less money than you started with. This type of financing is typically available from equipment sellers, although many banks also offer it.

U.S. Small Business Administration (SBA) loans

You may not think about SBA loans when considering fast business loan options, in part because they’re known for their lengthy approval periods. However, for SBA loans under $150,000, you may be eligible to receive funding in as little as one week instead of several weeks. Additionally, loans under $50,000 fall under the SBA Microloan Program, which is designed for startups and small businesses and typically offers faster funding through nonprofit intermediaries.

Your requirements would be the same as those with other lenders. However, your interest rate would be lower, and your repayment term would be longer. Although SBA loans may not be as fast as other options, the better interest rates and terms may be worth the wait.

Did You Know?

If you can't repay your SBA loan, the lender can seize any collateral you put up, and the SBA will seek repayment from you personally if it guaranteed the loan. Defaulting may also harm your credit and make it more difficult to obtain financing in the future.

6 fast business loans

While many lenders tout speedy funding, it pays to be cautious and choose a reputable option. In our reviews of the best business loan and financing options, the following lenders stood out for their established reputations and reliable service.

Alternative lender

Time to deposit

Loan size

Collateral

Rapid Finance

Same day

Up to $10 million

No

SBG Funding

Same day

Up to $10 million

No

Balboa Capital

Same day

Up to $5 million

No

Crest Capital

Same day

Up to $500,000

Yes

Fundbox

Next business day

Up to $250,000

No

Accion

Varies

Up to $250,000

Varies

Rapid Finance

This online lender provides business owners with funding the same day as approval. Rapid Finance will lend business borrowers anywhere from $5,000 to $10 million. The lender offers a simple online interface and mobile application, along with fast approvals. The online portal allows you to track the status of your loan and manage it. Rapid Finance offers a variety of loan types, including term loans, merchant cash advances and lines of credit. Learn more in our complete Rapid Finance review.

SBG Funding

SBG Funding can also fund a loan the same day it’s approved. This lender offers multiple financing options, including term loans, lines of credit, equipment financing, bridge loans and invoice factoring. With many of these loan types, you’ll get a decision on your application in 24 hours. We also like that you can make payments monthly or weekly, and that you can borrow up to $10 million.

Balboa Capital

Balboa Capital, another lender that can fund loans on the same day as approval, is also willing to work with borrowers who have less-than-perfect credit scores. We appreciate that this lender uses automated decision-making technology to streamline the approval process and enable same-day funding.

Crest Capital

Small business owners seeking fast equipment financing should consider Crest Capital. We found it to be one of the fastest lenders in the marketplace. Additionally, it offers flexible terms, allowing you to finance equipment for 24 to 84 months and borrow between $5,000 and $500,000. The equipment being financed serves as the collateral for the loan. Learn more in our Crest Capital review.

Fundbox

When it comes to a line of credit, Fundbox stands out for its innovation. This lender utilizes digital technology that allows you to connect your accounting software or business bank account directly to the application. It can also help you determine how to repay your loan while maximizing your cash flow. This online lender offers loans of up to $250,000, with terms ranging from 12 to 24 weeks.

Accion

We found Accion to be an excellent option for small business owners who need a microloan fast. Through the Accion Opportunity Fund, this nonprofit lender provides affordable loans, educational resources, coaching and networking opportunities to small businesses. Accion keeps it simple with an online application that takes about 15 minutes to complete. This nonprofit works with lenders in local communities, so the time it takes to receive your cash can vary. Our research found that some microloans can be funded the same day as approval or the next business day. Learn more in our Accion review.

FYI

Balboa Capital, Rapid Finance and SBG Funding are among our top options for business loans for bad credit. These lenders are willing to look beyond your credit score and consider factors like your time in business and annual revenue.

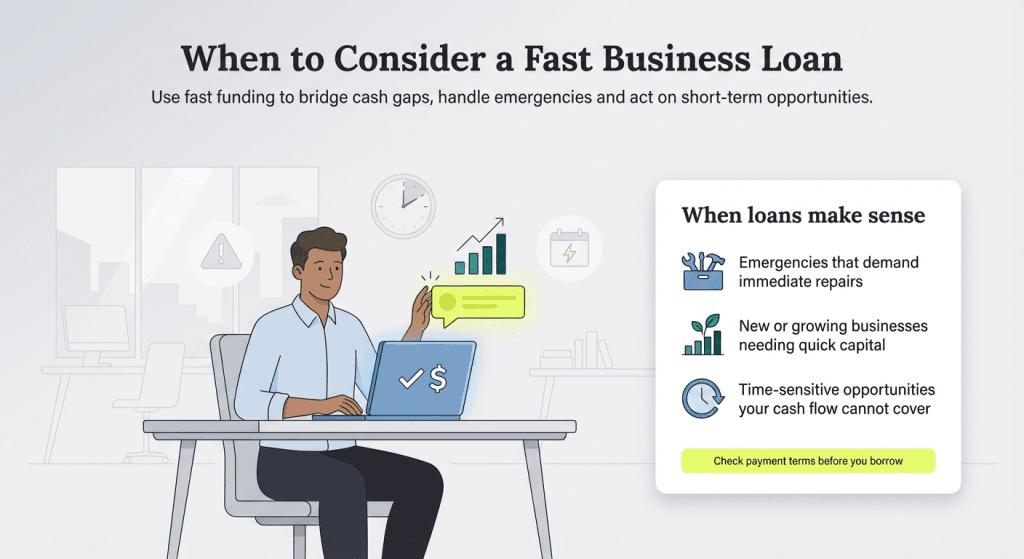

Who should consider a fast business loan?

Any business concerned about waiting for approval from a traditional lender may want to consider a fast business loan. “Traditional banks tend to have a longer approval period and may have stricter standards,” explained Eric Rosenberg, a business and personal finance expert. “Other funding sources, including credit cards and online lenders, are often faster if you need funds right away.”

If your company is facing any of the following situations, a fast business loan might be a good option to get some breathing room and continue operations:

Emergencies: Even if you have great business insurance, emergencies can create urgent needs that require fast but often expensive solutions. That’s where fast business loans come in. With these loans, you can repair the damage or solve the issue immediately and repay the funds when things get back to normal.

New company expenses: Starting and growing a business is expensive and often requires more money than you can generate from sales alone. A fast business loan can provide startup or growth funding much more quickly than you could through your standard revenue-generating routes.

Time-sensitive business opportunities: Let’s say you’re faced with an obvious business opportunity that requires fast action — a third-party agency that can take you on immediately, a limited-time bulk sale on key items in your inventory, or the chance to purchase a smaller company that will go with another buyer if you don’t act quickly. These loans can put the cash you need in your hands quickly.

Marketing campaign rescue: If your company has embarked on a mid-level sales or marketing campaign that isn’t getting the results you want, you can turn things around with more funding. Fast cash that arrives mid-campaign can help you upgrade to a higher-level strategy, which may boost your marketing ROI.

General quick-cash needs: No matter how new or established your business is, there will be times when cash runs short — for example, making payroll while you’re waiting on multiple invoices. Fast business loans can help bridge that gap.

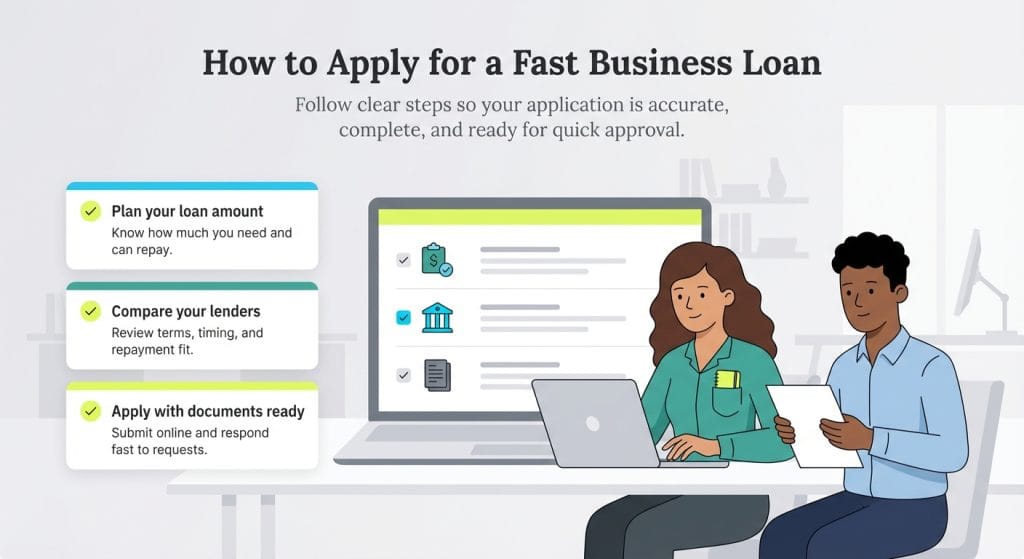

Once you decide it’s time to apply for a fast business loan, take the following steps to increase your chances of quick approval.

Decide how much you need to borrow: Determine how much funding will help you meet your business goals without borrowing more than you need.

Compare lenders: Research and compare three to five business loan providers. Look closely at the terms to make sure the lender offers the type of loan you want with loan repayment terms you can manage.

Gather your documentation: Find out what documentation is required and gather all necessary materials before starting your application.

Start the application on the lender’s website: Complete the online application using the information you’ve gathered. Be ready to upload scanned documents if requested.

Ask questions if needed: Reach out to the lender for help or clarification. For instance, you should know upfront whether a personal guarantee is required. “Find out if you need to provide a personal guarantee,” Rosenberg advised. “Many lenders want to look at your personal credit and guarantee you’ll use personal assets if necessary to pay the loan. This is especially true if you’re a new business and a new borrower.”

Submit the application: Once you’ve completed the application, submit it and monitor for follow-up requests. Be prepared to respond quickly if the lender asks for more information.

What documents are needed to apply for a fast business loan?

No two providers have exactly the same requirements. However, it’s generally safe to gather the following documents before you apply for a fast business loan:

Basic business information: Most fast business loan providers will require you to give your business’s name, address, contact information and taxpayer identification number or employer identification number. You may also need to provide the Social Security numbers of all business owners.

Credit history: You may need to provide proof of your credit score or submit a more detailed credit history. Lenders may have different thresholds for an acceptable credit score. However, keep in mind that even a single personal or business bankruptcy is often enough to disqualify you from access to fast business loans.

Business launch paperwork: You’ll need these documents to prove how long your company has existed. Many types of fast business loans are available only to companies that have existed for a certain number of years.

Business licenses: Occasionally, loan providers will ask for proof that your business is properly licensed. In this case, you can include just your original business license. Leave out other licenses, such as fire permits and DBAs (doing business as names).

Company tax returns: Most fast business loan providers have a minimum annual business income that applicants must meet to qualify for funding. Use your company tax returns to prove that your income is above this threshold.

Bank statements: Often, you’ll need to pair your company’s tax returns with bank statements for thorough income verification. It’s customary to provide your most recent three months of bank statements when you’re asked for any banking information.

Profit and loss statements: Lenders may want to see profit and loss statements to support your other financial information.

Online software information: Some fast business loan providers require you to detail any online systems your company uses for e-commerce, sales transactions, payroll and other key operations.

Loan history: Be prepared to show your entire history of loan applications and approvals or denials.

Other basic business documents: You also may encounter lenders that require you to provide other basic business paperwork, such as your office lease, a brief company history and your mission statement.

FYI

Some lenders may require a personal guarantee or business lien. A personal guarantee makes you personally responsible for repaying the loan if your business can't. A lien puts a personal or business asset at risk if you default.

What else to know before pursuing fast business loans

Here are a few additional best practices to consider before agreeing to a fast business loan.

Know the offered APR: Some lenders quote a monthly interest rate instead of the annual percentage rate (APR), which can make the loan seem cheaper than it really is. Be sure you’re comparing APRs to understand the true cost. Credit cards tend to have the highest APRs.

Figure out the ideal term: Have an idea of how quickly your business can repay the loan so you know what kind of loan to get. Short-term loans and credit card financing are best for repayment within a year or two, while term loans and equipment financing typically have three- to five-year terms.

Determine asset value (if applicable): If you pursue equipment financing or inventory financing, you should know the value of the asset you’re using as collateral.

Check for fees: Be aware of any fees, such as origination, administration, application and credit check fees.

Compare costs: Compare the total cost of each loan, including the total interest paid over the life of the loan and any associated fees.

Learn about the interest: Find out if the interest rate is fixed or variable, and get a sense of whether interest rates are likely to increase or decrease.

Negotiate: You can negotiate certain fees and may also be able to negotiate your interest rate.

Select your loan: Choose the one that makes the most sense for your business in terms of the amount, term, cost, required collateral and credit requirements.

Read the fine print: Read the loan agreement carefully before you sign, watching out for hidden clauses or fees. Don’t overlook sneaky long-term costs, even if you need an immediate solution.

Miranda Marquit and Jennifer Dublino contributed to this article.

For almost a decade, Max Freedman has been a trusted advisor for entrepreneurs and business owners, providing practical insights to kickstart and elevate their ventures. With hands-on experience in small business management, he offers authentic perspectives on crucial business areas that run the gamut from marketing strategies to employee health insurance.

At business.com, Freedman primarily covers financial topics, including debt financing, equity compensation, stock purchase agreements, SIMPLE IRAs, differential pay, workers' compensation payments and business loans.

Freedman's guidance is grounded in the real world and based on his years working in and leading operations for small business workplaces. Whether advising on financial statements, retirement plans or e-commerce tactics, his expertise and genuine passion for empowering business owners make him an invaluable resource in the entrepreneurial landscape.